Week Ahead – Long overdue US Q4 GDP, other data backlog to dominate

The fourth quarter GDP estimates for the United States will finally be published next week following the disruption to the American release calendar from the government shutdown. Canadian GDP will also be in focus, along with core PCE inflation numbers out of the US. Other notable releases include Japanese and Australian capital expenditure figures for Q4, as well as Eurozone flash inflation and Chinese manufacturing PMIs. Trade talks between the US and China will also be on investors’ radar as they look set to last beyond the March 1 deadline.

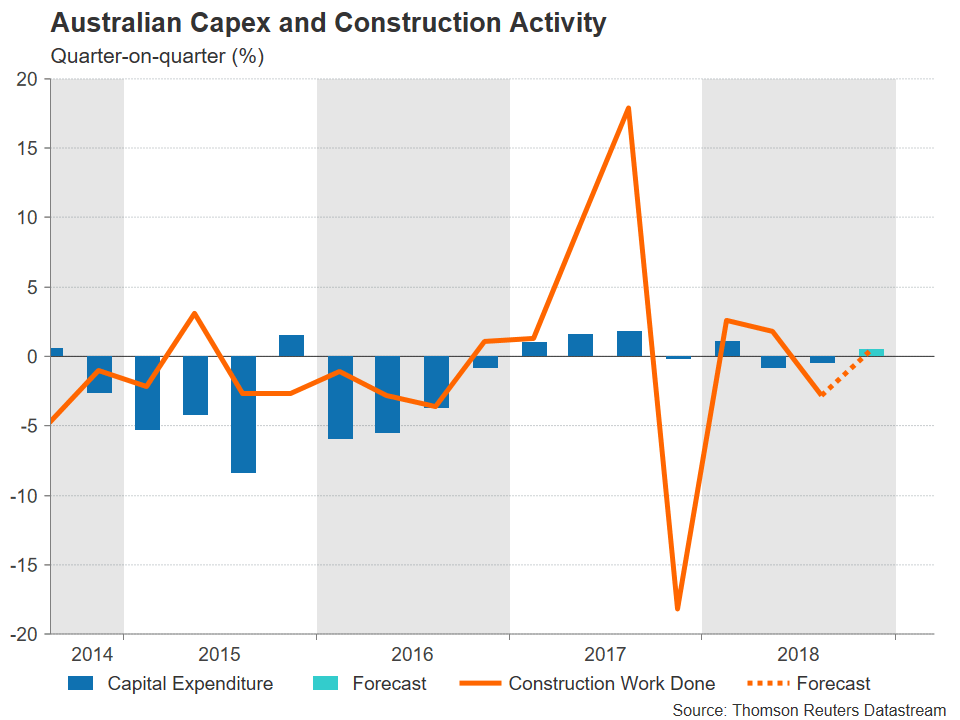

Australian economy under the spotlight

After hitting a bump this week, the Australian dollar could be sailing through more choppy waters in the coming days as some important data releases will be looked at for signs the Australian economy could be entering troubled times. First on the watch list is construction work done for the fourth quarter on Wednesday. Construction constitutes a sizeable portion of Australian GDP so the data will be a guide for Q4 growth figures due in the following week. Another clue will come from Thursday’s Q4 capital expenditure figures. Also out on Thursday are private sector credit numbers for January and rounding up the week on Friday will be the AIG manufacturing index for February.

The aussie erased almost two weeks of gains on unexpectedly weak PMIs by IHS Markit as well as reports that China has banned some imports of Australian coal. Hence, any worrying aspects to next week’s data could further pressure the aussie.

In addition to the domestic data, aussie traders will also be watching the latest manufacturing PMIs out of China. The official manufacturing PMI, due on Thursday, is expected to hold steady at 49.5 in February, while a day later, the Caixin/Markit PMI could provide some relief to the markets as it’s forecast to edge up by 0.2 points to 48.5.

Could be a tough week for the kiwi too

The New Zealand dollar hasn’t fared any better than its aussie cousin over the past week despite the absence of any local data. However, New Zealand indicators will move to the forefront next week with a number of big releases. Kicking off the week are the fourth quarter retail sales numbers on Monday. This will be followed by trade figures on Wednesday and the closely-watched ANZ business outlook survey on Thursday, both for January. On Friday, kiwi traders will be hoping to get an insight to Q4 GDP performance from New Zealand’s terms of trade gauge.

A weak set of figures would likely strengthen expectations of a rate cut by the Reserve Bank of New Zealand later this year, weighing on the kiwi.

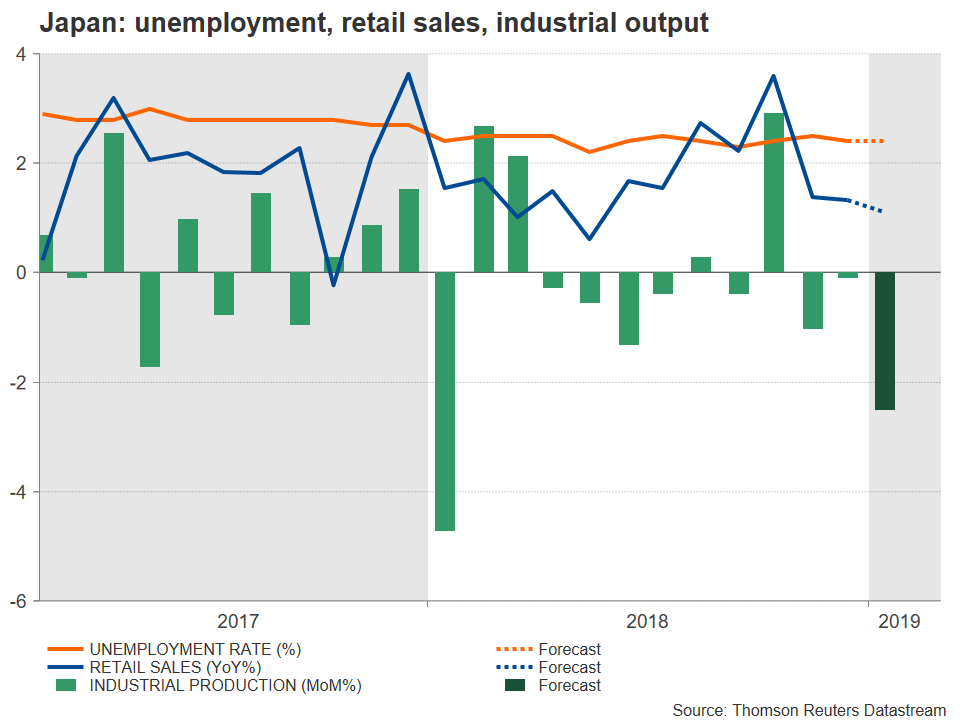

Japanese industrial output eyed

While much of the focus in the global slowdown narrative has been on China and now increasingly, on the Eurozone, Japan’s economy is also at risk of a major downturn. Fears about the world’s third biggest economy were heightened this week after data showed Japan’s exports plunged by 8.4% on an annual basis in January.

There will be more Japanese indicators for January coming up over the next seven days, with the most significant being Thursday’s preliminary reading of industrial output. Retail sales are also due on Thursday, while on Friday, unemployment numbers will be viewed along with capital expenditure for the fourth quarter. The capex data is seen as a reliable guide to the second GDP estimate, which tends to be revised sharply in Japan.

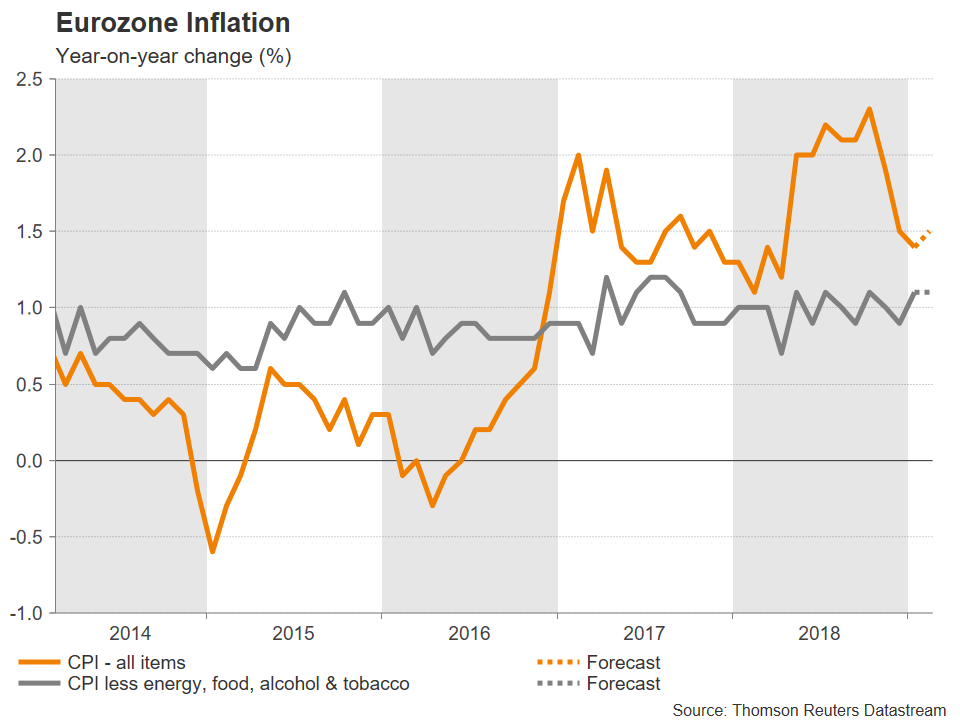

Eurozone flash CPI to be European highlight

The flash reading of the Eurozone PMIs for February provided some glimmer of hope that the severe slowdown could be coming to an end. There could be more evidence of the downtrend bottoming out in Wednesday’s economic sentiment indicator for the euro area.

The single currency could receive some support if the survey points to a steadying picture in February, but otherwise, with the only other major release being the preliminary inflation print for February, the euro could struggle for direction next week.

The flash headline inflation figure, out on Friday, is expected to inch higher by 0.1 percentage points to 1.5% in February. However, core CPI, which excludes food, energy, tobacco and alcohol, is forecast to stay unchanged at 1.1% year-on-year. Also out on Friday is the Eurozone unemployment rate for January and the final manufacturing PMI for February.

Yet another Brexit vote looms in UK Parliament

It’s going to be a muted week in the UK as well for economic data, with only Friday’s manufacturing PMI filling up the calendar. The Markit/CIPS manufacturing PMI is forecast to decelerate further in February, from 52.8 to 52.0.

However, Brexit will once again be keeping pound traders active as another crucial vote on the Brexit deal is scheduled next week for February 27. It’s not quite clear what MPs will be voting on at this point. If the prime minister, Theresa May, manages to secure legal assurances from the EU on the Irish backstop, there will likely be a meaningful vote on the revised deal. But if UK-EU negotiations have not been completed by then, MPs could simply vote on an amendable motion on how to proceed next with Brexit. The latter carries the risk of Parliament voting to take control of the Brexit process, possibly forcing the government to extend Article 50, if Mrs. May has nothing to show from the latest round of talks with Brussels. Either way, the pound appears to be headed for more volatility.

Canadian inflation and GDP to provide rate clues

Inflation and GDP growth numbers out of Canada next week could be significant for the loonie as any surprises in the numbers will probably impact rate hike expectations. The inflation figures are released first on Wednesday and investors will be watching for another possible strong reading in the headline number in January following December’s unexpected overshoot of 2.0% year-on-year.

Producer prices for January will be up next on Thursday but the main focus will be on Friday’s GDP estimates for Q4. Canada’s economy expanded by 0.5% quarter-on-quarter in the October quarter and a softer reading is likely for the final three months of 2018. A very disappointing figure would further dash expectations of a rate hike in 2019 following this week’s cautious remarks by Bank of Canada Governor Stephen Poloz.

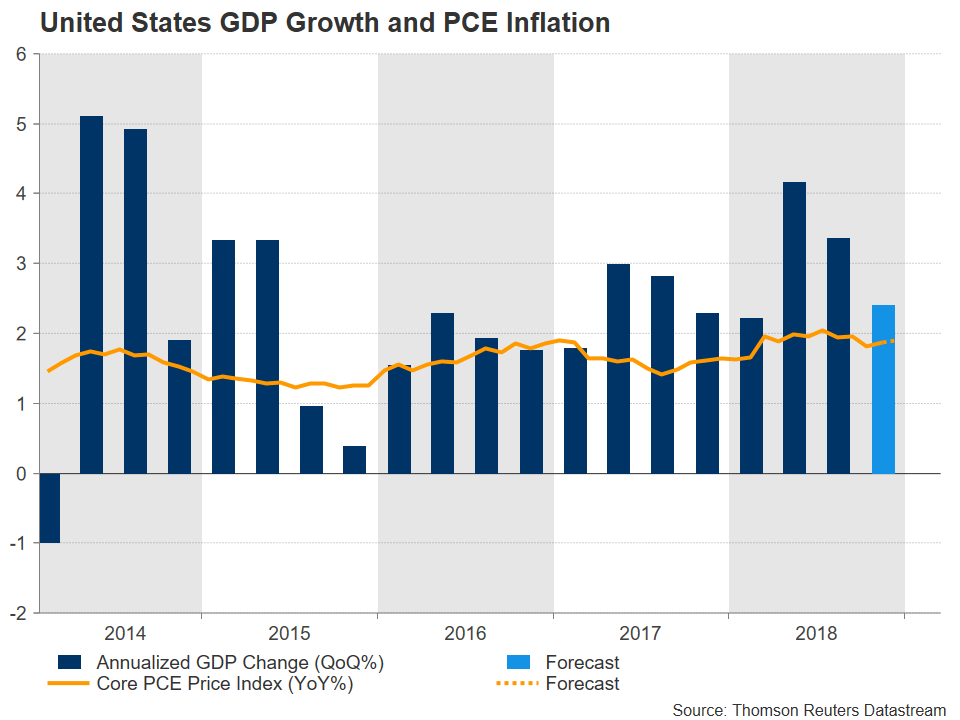

US data to play catchup

There will be an overload of data out of the US in the coming week as many of the delayed releases are finally published. The housing market will fall under the limelight on Tuesday as December building permits and housing starts are released together with the S&P CoreLogic Case-Shiller 20-city home price index. Also due on Tuesday is the Conference Board’s barometer of consumer confidence. The index is forecast to increase in February from 120.2 to 125.0. If confirmed, it would end a steep three-month decline.

On Wednesday, factory orders and the trade balance for December will be monitored, as well as January pending home sales before attention moves to Thursday’s all-important GDP report. Growth in the world’s largest economy is projected to have slowed from an annualized rate of 3.4% in Q3 to 2.4% in the December quarter.

More top tier data will follow on Friday with all eyes turning to the Fed’s favourite inflation measure – the core PCE (personal consumption expenditures) price index. The price gauge is expected to have held steady at 1.9% y/y in December, just below the Fed’s 2% target. A surprise dip in the figure would probably reinforce expectations that the Fed will remain on pause until there’s a convincing build-up of inflationary pressures. In addition to the inflation data, the PCE report will contain the latest numbers on personal income and spending.

Equally important on Friday will be the ISM manufacturing PMI for February. The PMI is anticipated to record a 0.6 point drop to 56.0, in line with the other manufacturing indices released in recent days.

Tariff deadline nears; poses danger to risk rally

The US dollar could come under some selling pressure if the above data adds to the global growth worries than reassure investors that US fundamentals remain solid. The greenback is also likely to be driven by safe-haven flows as the March 1 deadline approaches when US tariffs on $200 billion worth of Chinese imports will automatically rise from 10% to 25% unless a trade agreement is struck, or President Trump decides to push back the deadline.

Given the extent of the rally in risk assets on expectations of a deal, any setback in the US-China trade negotiations could trigger a sharp correction, particularly in equities, but would lift safe havens such as the dollar and the yen.

Investors will also be watching the second summit between President Trump and North Korean leader Kim Jong-un in Vietnam on February 27-28. However, any developments in US-North Korean relations are more likely to influence gold than the currency markets.

Author

Mr Boyadjian graduated from the London School of Economics in 1999 with a BSc in Business Mathematics and Statistics. Following graduation, he joined PricewaterhouseCoopers in the Business Recoveries team, where he was responsibl