USD/CAD Weekly Forecast: COVID strikes again

- New COVID variant, Omicron, first-discovered in South Africa, roils global markets.

- WTI falls 10% from Monday’s open, 12.8% on Friday, commodities plunge.

- USD/CAD adds 1%, closes at two-month high despite US Treasury yield decline.

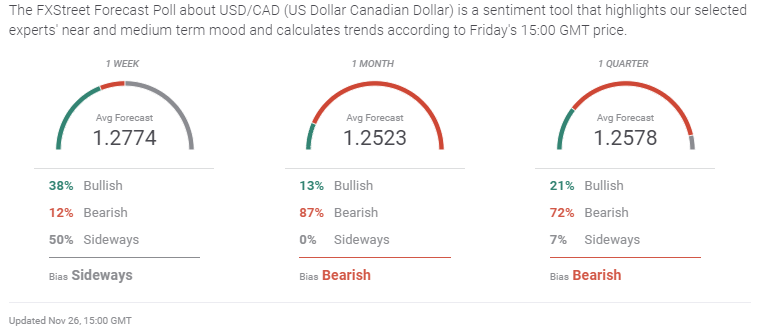

- FXStreet Forecast Poll predicts near-term neutrality.

The discovery of a new COVID variant in South Africa amplified fears about the economic impact of the already spreading viral cases in Europe and completely upended global markets on Friday. Travel restrictions on South Africa and neighbor countries by the US, UK and others underlined the perceived danger.

The ensuing equity and commodity sell-off and safe-haven demand punished the Canadian dollar which dropped to its lowest level against its US counterpart in two months.

Dollar-Canada* opened the week at 1.2641 and by the end of trading in Thursday’s US holiday market had barely stirred to 1.2648. Friday’s global equity and commodity sell-off on fears that the new COVID variant and the ensuing restrictive mandates will crush the economic recovery, drove crude oil prices to their largest single day fall since April 2020.

Dollar-Canada moved higher at the beginning of Friday's market, encountered some resistance above 1.2750, touched 1.2800, its highest trade since September 22 and settled at 1.2768, a two-month high, up 1.1% on the day.

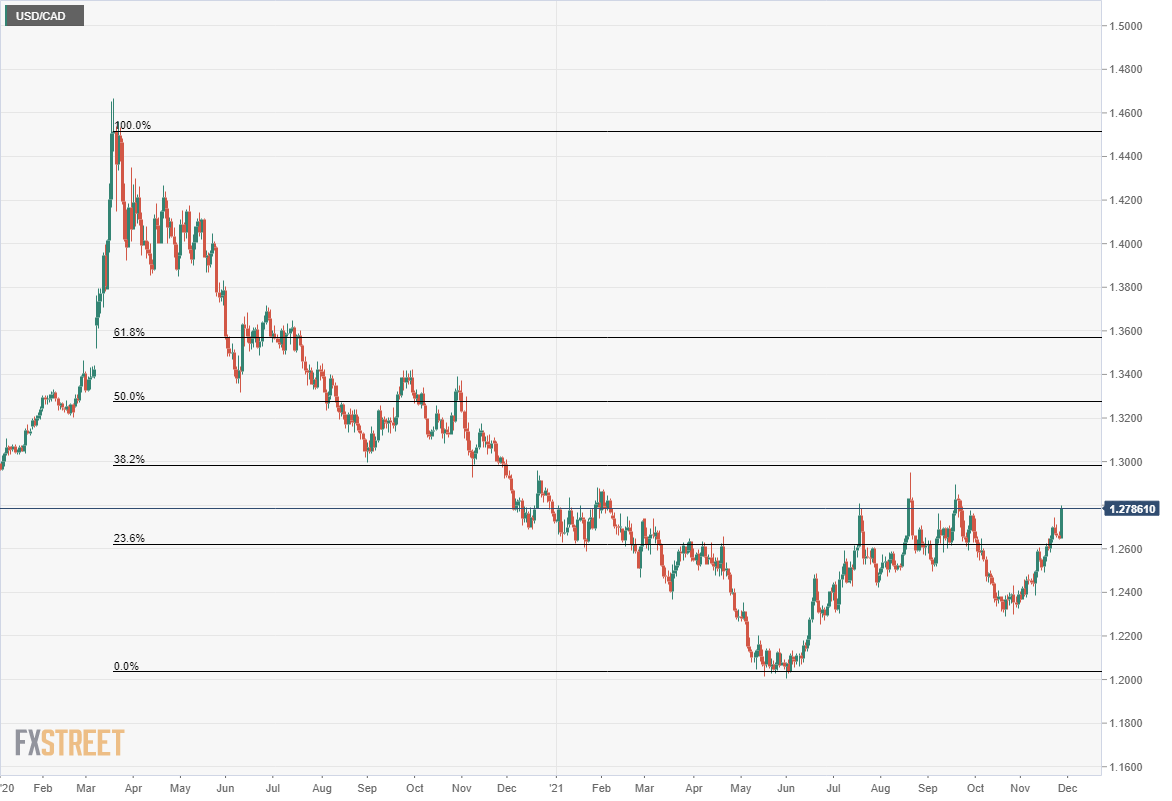

The USD/CAD has gained 3.8% from its open at 1.2320 on October 22 and 6.2% from its low of 1.2035 onJune 2.

West Texas Intermediate (WTI), the North American crude pricing standard, lost 12.8% on the day ($78.10-468.09) and 10% on the week ($75.58-$68.09).

The Bloomberg Commodity Index (BCOM) fell 3.36% on Friday and closed at 100.10, down 5.42% from the seven-year high of 105.84 on October 25.

Bloomberg/MarketWatch

American equities took a huge beating with the Dow losing 2.53%, 905.04 points to 34,899.34. The S&P 500 tumbled 106.84 points, 2.27%, finishing at 4.594.62.

Sovereign interest rates tumbled on Friday as investors anticipated future central bank accommodation should the new variant prove dangerous.

The Canadian 10-year bond yield lost 16 basis points to 1.605% and the yield on the US 10-year Treasury also shed 16 basis points to 1.482%.

There were no Canadian economic statistics this week.

In the United States, the Core Personal Consumption Expenditure Price Index – core PCE for short – the Fed’s preferred inflation measure, came in at 4.1% (YoY) in October, well above the 3.7% prediction and the highest annual rate since January 1991. The headline PCE rate soared 5%, the fastest gain since November 1990.

Personal Spending, a broader gauge of consumption than Retail Sales, rose 1.3% from 0.6% in September. Excluding the stimulus fueled months of January and March this year, it was the best score since July 2020.

The Fed initiated the withdrawal from its monthly $120 billion bond purchases at its November 3 meeting. A reduction of $15 billion is scheduled for November and December, with continuing subtractions expected until the program is eliminated in June.

Accelerating inflation makes the need for higher US interest rates plain. Core PCE has nearly tripled this year from 1.5% in January, and the overall rate has soared 3.5 times from 1.4%.

Manufacturing costs are also rocketing, guaranteeing that yet higher prices will be passed onto consumers. The Producer Price index jumped 8.6% in October, its highest level in 13 years.

Economic growth fell sharply in the third quarter to 2.1% from 6.5% in the first half of the year. If expansion continued at that pace in the fourth quarter, the Fed governors might be hard pressed to justify higher interest rates despite the inflationary surge.

The Federal Open Market Committee (FOMC) does not want to be forced to choose between curbing inflation and growth.

Fortunately for the bankers, the American consumer is ignoring inflation and spending at levels that should keep the economy humming through to the end of the year.

The latest Atlanta Fed GDPNow estimate for the final three months of the year is 8.6%. If accurate, that would provide 5.9% growth for the year.

In addition to the Personal Spending and PCE data discussed above, several other US statistics intimated a healthy economy. Initial Jobless Claims dropped to 199,000 in the week of November 19, far below the 260,000 forecast and the lowest number since November 1969. Even in the heady expansion of late 2019 and early 2020, the lowest reading was 201,000 in the week of January 31. Personal Income, a more encompassing gauge of family finances than Average Hourly Earnings, that includes transfer payments, interest income and other non-salary items, rose 0.5% in October, more than twice its 0.2% forecast and a reversal of the 1% September decrease. Wholesale Inventories rose 2.2% in October, up from 1.4% in September and one reason for the rising GDP estimates for the fourth quarter.

*Currency market terminology for USD/CAD

USD/CAD outlook

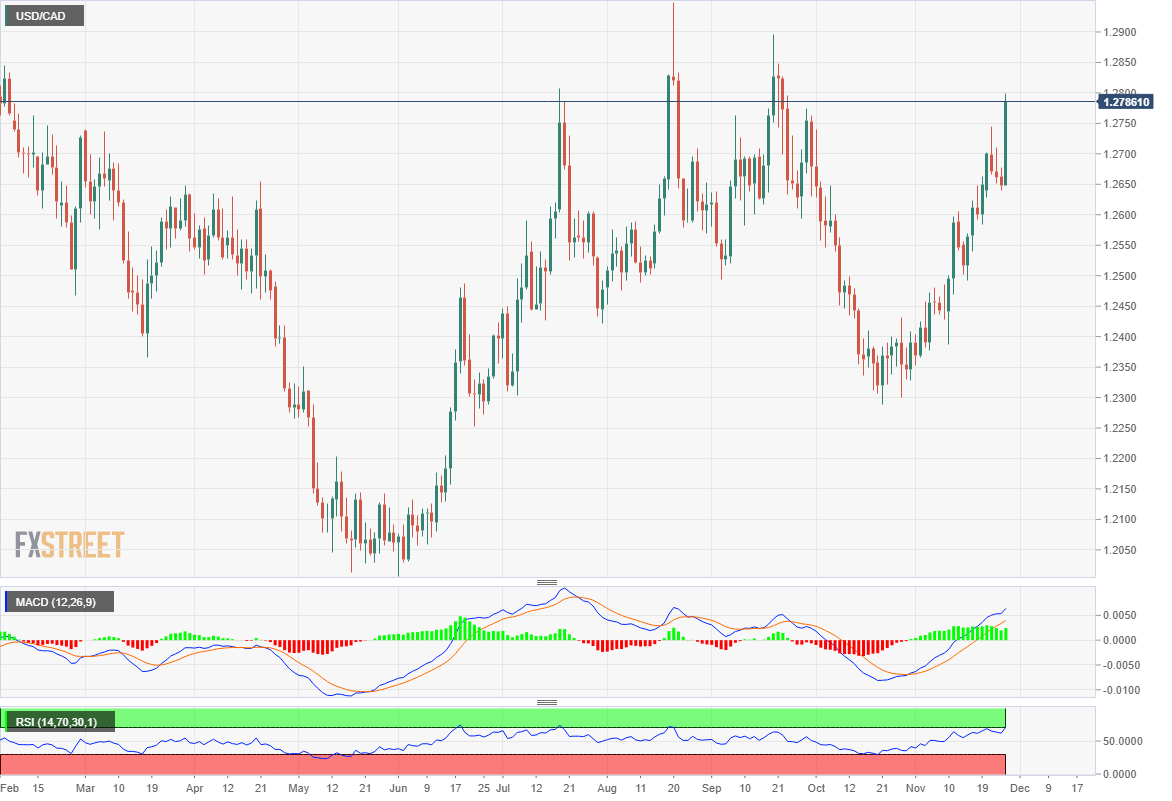

The USD/CAD has not overcome crucial resistance at 1.2825 centered on the high finishing trades in August and September. Thursday’s close at 1.2648 was 27 points above the 23.6% Fibonacci retracement level (1.2621) of the March 2020 (1.4514) to June 2021 (1.2035) USD/CAD decline. The September to November drop was partially due to the inability to approach the 38.2% Fibonacci retracement line at 1.2983.

Fundamentally, the drop in oil prices is a large impediment to robust growth in the Canadian economy. The Bank of Canada (BOC) has an aggressive rate normalization policy, having already ended its bond purchases. If the global recovery recedes because of a new series of government lockdowns, whether from the Delta-wave or some other variant, Canada’s resource based economy will not prosper. The BOC will be unable to continue its push for higher rates until growth resumes.

Canadian Gross Domestic Product (GDP) for September and annualized for the third quarter on Thursday will not move trading. The Employment Change Report on Friday will, as usual, be subsumed in the US payroll release at the same time.

The speculation that US rate policy is about to shift was given backing in the minutes of the November 3 FOMC meeting released on Wednesday. The summary noted that bank officials were concerned about inflation and would be willing to raise interest rates “sooner than participants currently anticipated”, with some advocating a more aggressive tapering program.

The appointment of Jerome Powell as Federal Reserve Chair is another plus for the dollar. His competitor for the post, now Vice-Chair, Lael Brainard, was viewed by markets as a bit more accommodating, though there is probably little reason to doubt that in practice, her policies would have been nearly identical.

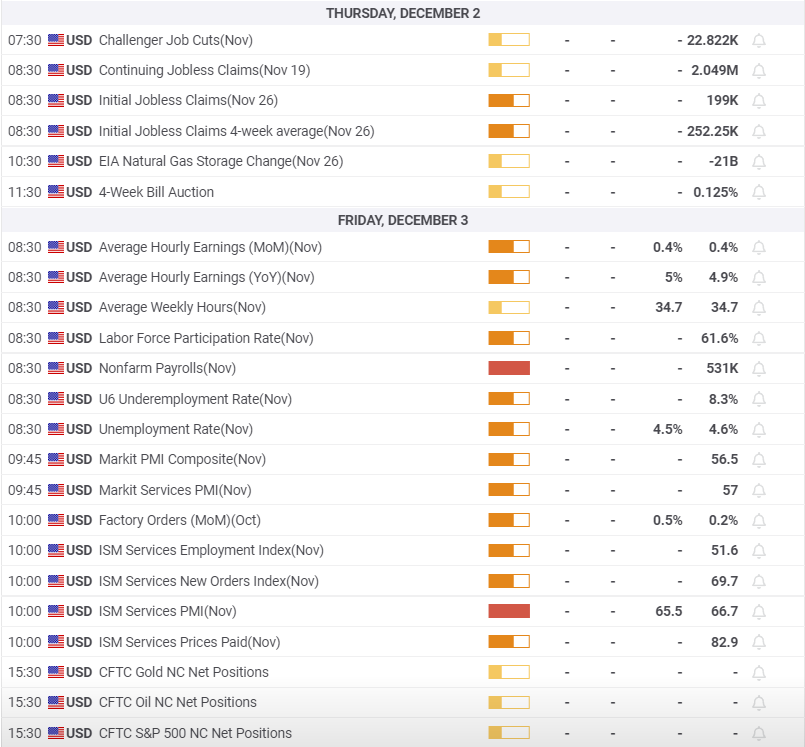

In the US, Nonfarm Payrolls have the potential to send the dollar and interest rates higher. The relationship is linear, better payrolls, higher Treasury yields and the dollar. Purchasing Managers’ Indexes for the manufacturing and services sectors will also provide the greenback with support if they show an accelerating US economy.

The USD/CAD bias is higher with the large caveat that if the newest South African variant proves to be little different in consequence than previous versions, Friday’s rampant moves will reverse. That will not negate the basic USD/CAD trend higher, but it will weaken momentum and could result in a period of relative neutrality.

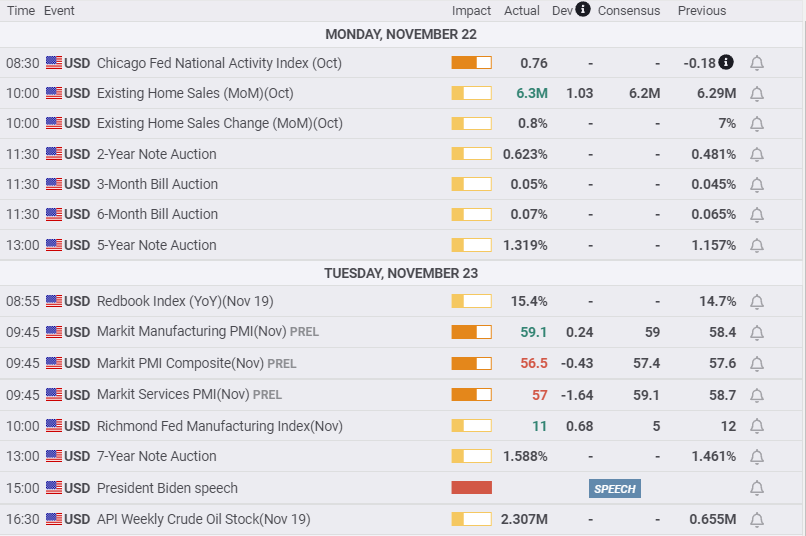

Canada statistics November 22–November 26

US statistics November 22–November 26

FXStreet

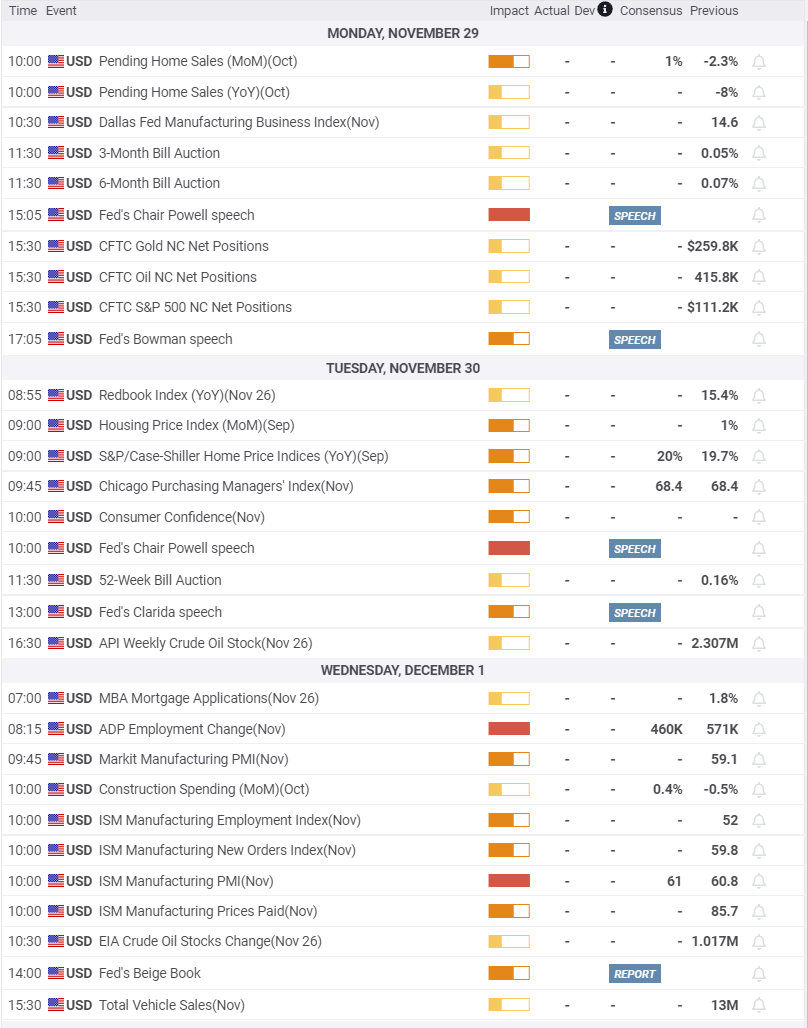

Canada statistics November 29–November 26

FXStreet

US statistics November 29–December 3

USD/CAD technical outlook

The MACD (Moving Average Convergence Divergence) has favored the USD/CAD since the main line crossed the signal line on October 28. The divergence dipped on Thursday but widened again on Friday. It remains a purchase. The Relative Strength Index (RSI) borders on overbought status, and so stays a buy, if a wary one.

Three moving averages clustered within 32 points midway between 1.2500 and 1.2600 are a source of major support. The 21-day moving average (MA) at 1.2543, the 50-day MA at 1.2534 and the 100-day MA at 1.2566 indicate a base for upward movement. The 200-day MA at 1.2472 is a strong backup.

Resistance: 1.2825, 1.2860, 1.2915, 1.2940

Support: 1.2755, 1.2700, 1.2650, 1.2600

FXStreet Forecast Poll

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.