USD/CAD Weekly Forecast: Change is brewing

- USD/CAD nearly level on the week after two-year low on Thursday.

- WTI in a holding pattern for the last two weeks.

- BoC keeps rates and quantitative easing unchanged as anticipated.

- FXStreet Forecast Poll sees continued gains in USD/CAD.

The Bank of Canada left policy unchanged at its Wednesday meeting surprising no one.

There had been little market expectation for variation in either the 0.25% overnight lending rate or the C$4 million a week of quantitative easing purchases. Media exposition had suggested that in light of the weak December employment report the bank might opt for a reduction less than the standard 0.25%.

What was unforeseen, given that much of the Canadian economy is locked down, was the bank's relative optimism about the vaccine and its impact on second half growth which drove the USD/CAD down almost a figure to close at 1.2643 on Wednesday.

The headline on the Bank of Canada website said the bank “will hold current level of policy rate until inflation objective is achieved.” The text of the policy statement was rather more positive, noting that “as the governing council gains confidence in the strength of the recovery, the pace of net purchases of Government of Canada bonds will be adjusted as required.”

As markets anticipate an economic recovery long before an inflation revival, the statement implies that a reduction in quantitative easing could happen with a rise in growth in the third or even second quarters.

That possibility may have been responsible for the loonie's continued strength on Thursday where the USD/CAD dropped to 1.2590, the strongest for the Canadian dollar since April 19, 2018. That brief plunge had reversed by the end of the day with the finish at 1.2632.

The rebound in USD/CAD continued on Friday with profit-taking assisted by a fall in WTI from $53. Governor Tiff Macklem is highly unlikely to send the Canadian dollar soaring in the midst of a recovery by curbing QE purchases before the Federal Reserve even if the economy begins to purr by June.

Canadian Retail Sales in November at 1.3% were much better than the 0.1% forecast and October's 0.4%, but as the economy went back into partial lockdown in December there was no market impact.

The US inaugurated its 46th President Joe Biden on Wednesday to minimal market reaction in a capital empty of crowds and patrolled by 25,000 National Guard troops.

An anticipated $1.9 trillion stimulus package has helped support equity markets and boosted Treasury returns though neither has assisted the dollar much.

Initial Jobless Claims fell to 900,000, the prior week was revised down by 39,000 and continuing claims fell to their lowest level of the pandemic but labor market concerns continue unabated. Housing construction and sales remained exceptionally strong, even in their quietest winter month. Perhaps that is a sign of an impending boom in the spring.

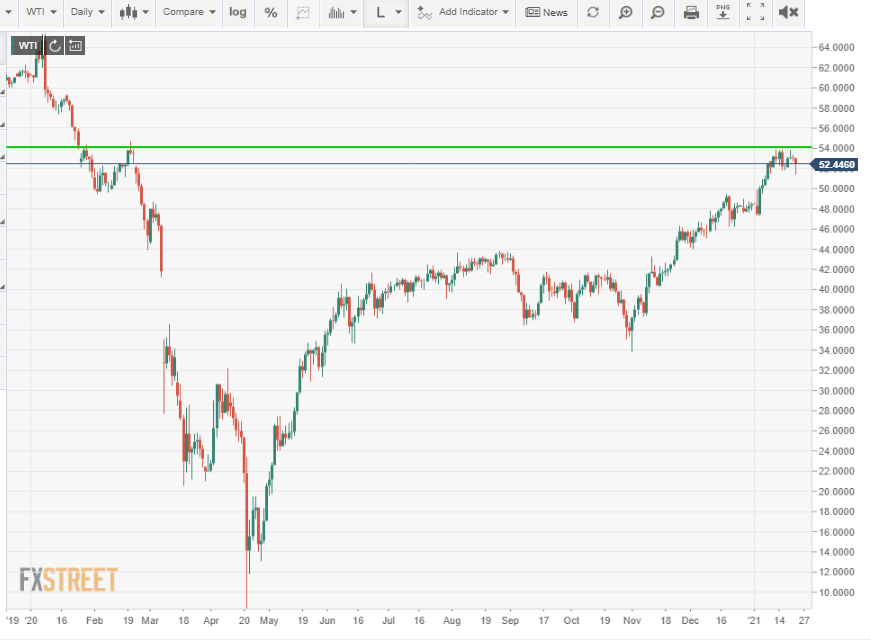

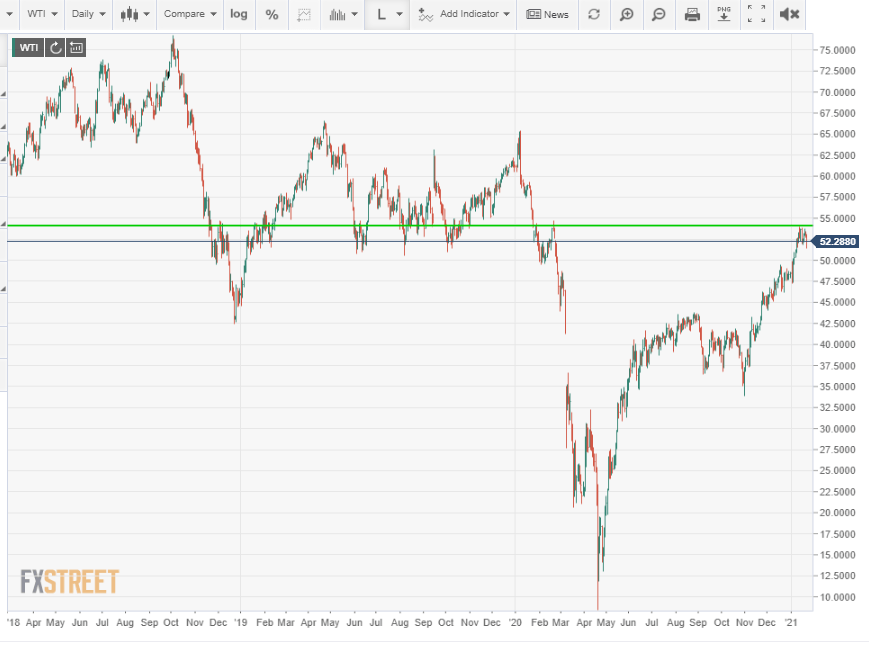

West Texas Intermediate was again unable to break $54 resistance with a high of $53.80 on Wednesday. Prices marked time on Thursday, opening at $53.12 and finishing at $52.98. The week's long positions were cut on Friday with the dip to $51.43 but the recovery to $52.44 is evidence that WTI is still expected to move higher in the immediate future.

USD/CAD outlook

The USD/CAD is in the somewhat unusual position (for the current market) of trading on both sides of the pair. Movement is not limited to input from the US dollar side, as is largely true, at least for the moment, in the USD/JPY and EUR/USD.

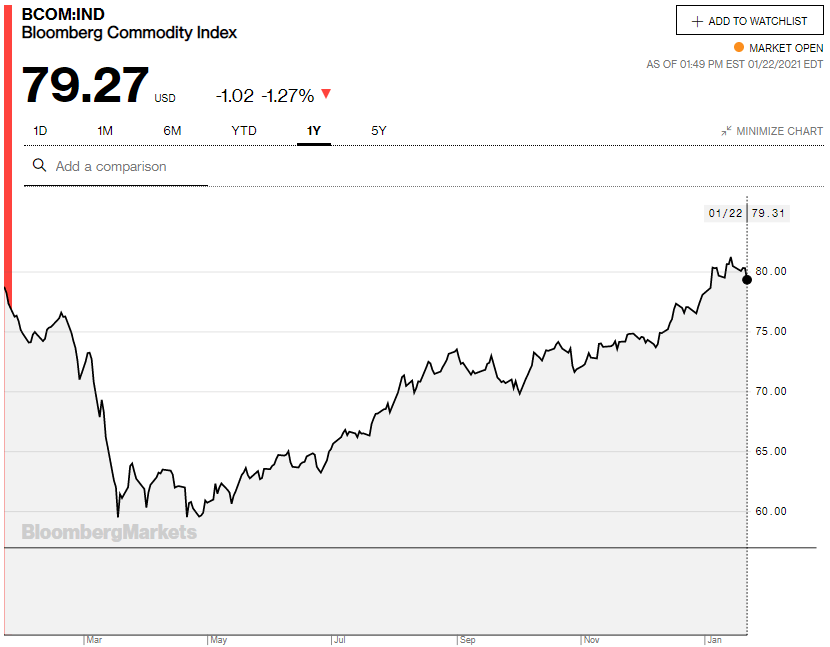

Commodity prices have been a major factor in the recent loonie strength but they have completed the return to the level before the pandemic and have largely priced in the anticipated global economic recovery.

Further increases in commodity prices will depend on global growth exceeding that of 2019. While that is possible there is no evidence of it yet. For the immediate future any accession to loonie strength from this quarter is apt to be limited.

The one exception to this picture is WTI which, once the global recovery picture comes into focus, is likely to return to its $55 to $75 range of 2018 and 2019.

The overall trend in the USD/CAD remains weakly lower, mostly from the lack of a competing scenario.

Not until the US and Canadian economies are divested of their lockdowns and can compete on economic recovery will we be able to gauge the impact on the USD/CAD.

Historically, the US has had the best recovery record among the developed economies but as the two North American economies are closely tied the differential is much smaller than that between the US and Europe. The $1.9 trillion stimulus will improve the perception of US growth even if its actual economic impact will be largely limited to consumer spending.

The impending economic recovery is likely to favor the greenback. But because Canada participates in US growth and because the loonie has sources of its own strength in commodities and oil, it should be resilient in the US dollar recovery in the second and third quarters.

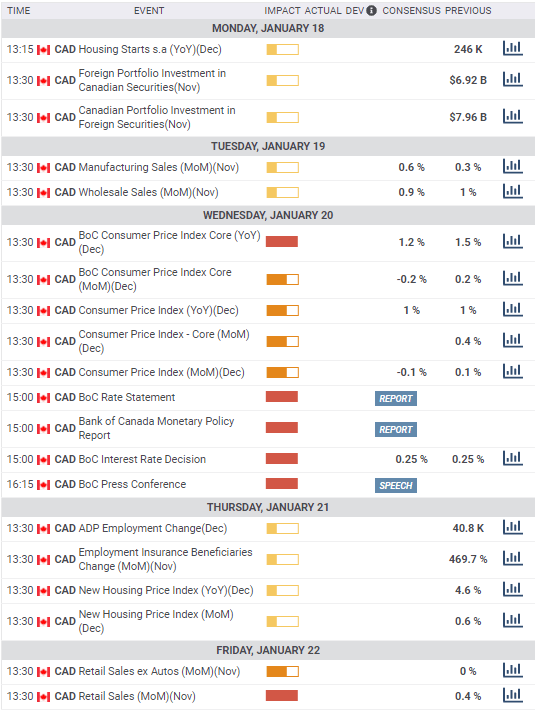

Canada statistics January 18-January 22

Monday

Housing Starts fell slightly on an annualized basis to 228,3000 in December from 259,900. The forecast was 225,000.

Tuesday

Manufacturing Sales fell 0.6% in November on a -0.1% estimate and a 0.2% increase in October. Wholesale Sales rose 0.7% in November on a 1% forecast and November result.

Wednesday

The Bank of Canada held policy steady, overnight cash at 0.25% and bond purchases at C$4 million a week. The Consumer Price Index fell 0.2% on the month in December on a 0.0% forecast and November's 0.1% gain. The annual rate rose 0.7% on a forecast and November rate of 1%. Core CPI from the Bank of Canada fell 0.4% on the month in December on a -0.2% forecast and a 0.2% gain in November. The annual rate was unchanged at 1.5% on a 1.2% prediction.

Thursday

ADP Employment Change shed 28,800 jobs in December after losing 219,8000 in November.

Friday

Retail Sales rose 1.3% in November, far more than the 0.1% forecast after a 0.4% gain prior. Sales ex-Autos climbed 2.1%, seven times the 0.3% estimate and following a flat October.

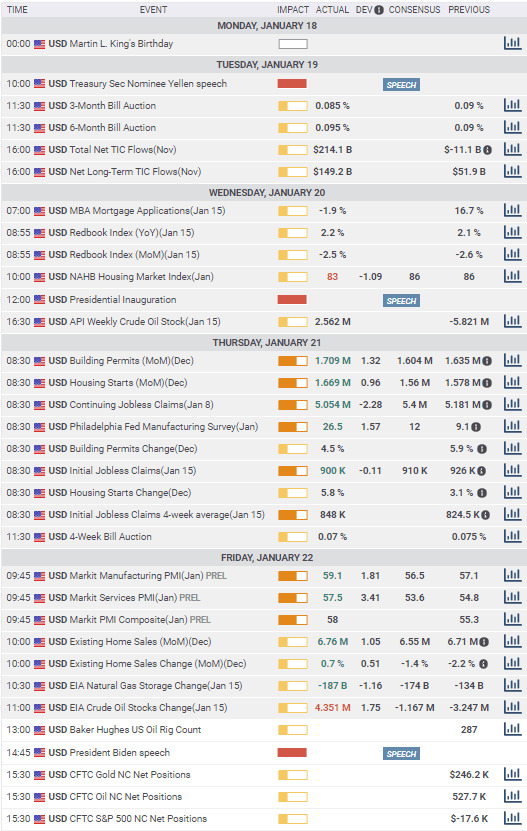

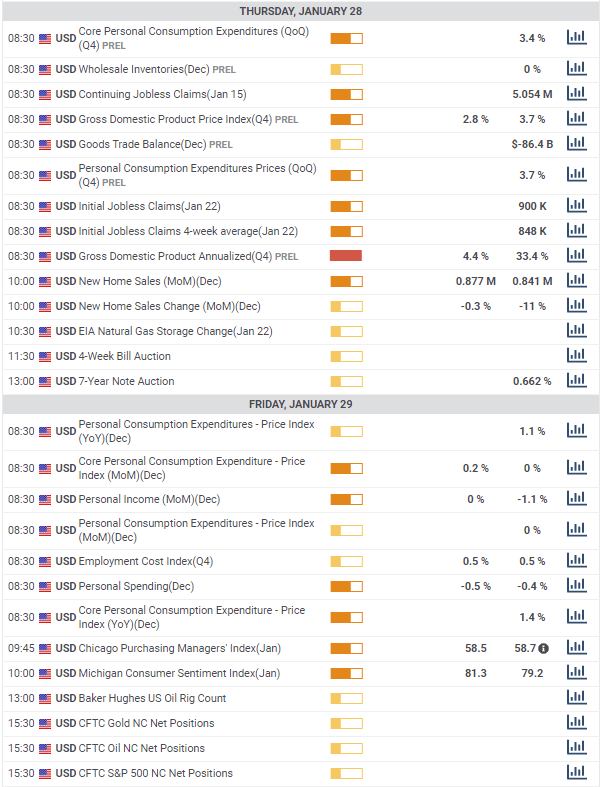

US statistics January 18-January 22

Existing Home Sales, Housing Starts, Building Permits and Markit's PMIs in Manufacturing and Services point to an economy lined up for the end of the pandemic.

Thursday

Initial Jobless Claims dropped to 900,000 in the January 15 week from 926,000 prior, revised from 965,000. The forecast was 910,000. Continuing claims fell to 5.054 million in the January 8 week, well under the 5.4 million estimate, from 5.181 million previous, revised from 5.271 million. The four-week moving average rose to 848,000 in the January 15 week from 824,500. It was the highest average since the week of October 2. Housing Starts in December rose 5.8% to 1.669 million (annualized) their best level since the housing bubble of the last decade. Building Permits climbed 4.5% to 1.709 million per year, also the best rate since 2008.

Friday

Markit Manufacturing PMI in January rose unexpectedly to 59.1 from 57.1, 56.6 had been forecast. Services PMI climbed to 57.5 from 54.8 on a 53.6 prediction and the Composite Index came in at 58 after 55.3 in December. Existing Home Sales in December rose 0.7% to 6.76 million per annum, from 6.71 million in November. It was highest pace since 2006. Sales had been forecast to drop to 6.55 million. The jump was doubly unexpected as December is normally one of the slowest month of the year for home sales.

FXStreet

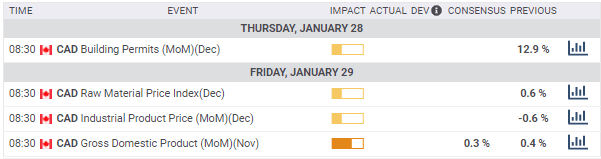

Canada statistics January 25-January 29

A sparse week. Only November monthly GDP has a potential market impact.

Thursday

Building Permits for December is on the schedule, they rose 12.9% in November.

Friday

Raw Material Price Index and Industrial Product Price for December are due, they were 0.6% and -0.6% in November. November GDP is forecast to rise 0.3% following a 0.4% gain in October.

FXStreet

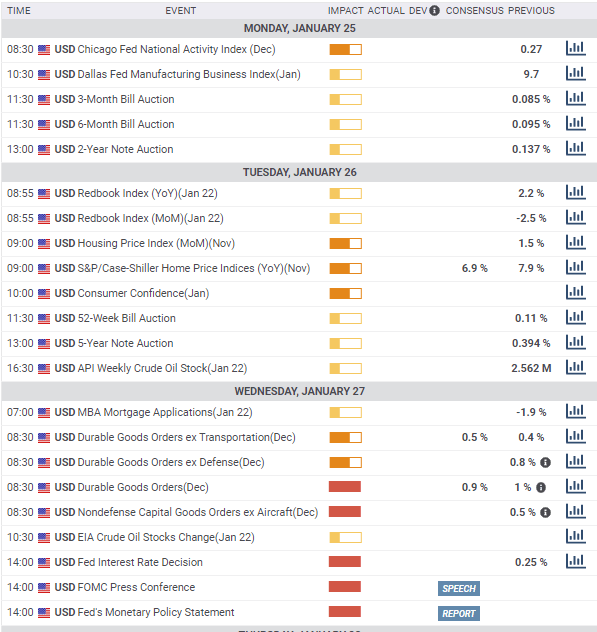

US statistics January 25-January 29

The Federal Reserve two-day meeting which finishes on Wednesday is the main interest. With no change expected in either the fed funds or the bond purchase program the chief curiosity will be Chairman Jerome Powell's discussion of the US economy in his prepared statement and news conference. Fourth quarter preliminary GDP on Thursday will run a close second to the Fed and has more potential for an unexpected result.

Tuesday

Conference Board Consumer Confidence for January is expected to drift lower to 78.3 from 79.2 in December.

Wednesday

Durable Goods Orders for December are forecast it rise 1% as in November. Orders ex-Transportation are expected to gain 0.5% after 0.4% in November. Nondefense Capital Goods ex-Aircraft, the proxy for business investment spending, was revised to 0.5% from 0.4% in November .

The Federal Reserve will leave the fed funds target range unchanged at 0.0% to 0.25% and bond purchases at $120 billion a month.

Thursday

Fourth quarter annualized GDP is forecast to be 3.9% but the range of estimates is unusually wide. The Atlanta Fed GDPNow model posits 7.5%. Initial Jobless claims for the January 22 week are expected to be 875,000 after 900,000 prior. Continuing Claims are forecast to be 4.9 million in the January 15 week following 5.054 million. New Home Sales are predicted to increase 2.7% in December to 855,000 annualized from -11% and 841,000 in November.

Friday

Personal Income in December is expected to rise 0.1% after falling 1.1% prior. Personal Spending is projected to be down 0.4% in December as in November. Michigan Consumer Sentiment is forecast to be unchanged at 79.2 on revision. The Core Personal Consumption Expenditures Price Index (PCE) is expected to gain 0.1% in December after flat in November and the annual rate is forecast to be 1.3% after 1.4% in November.

FXStreet

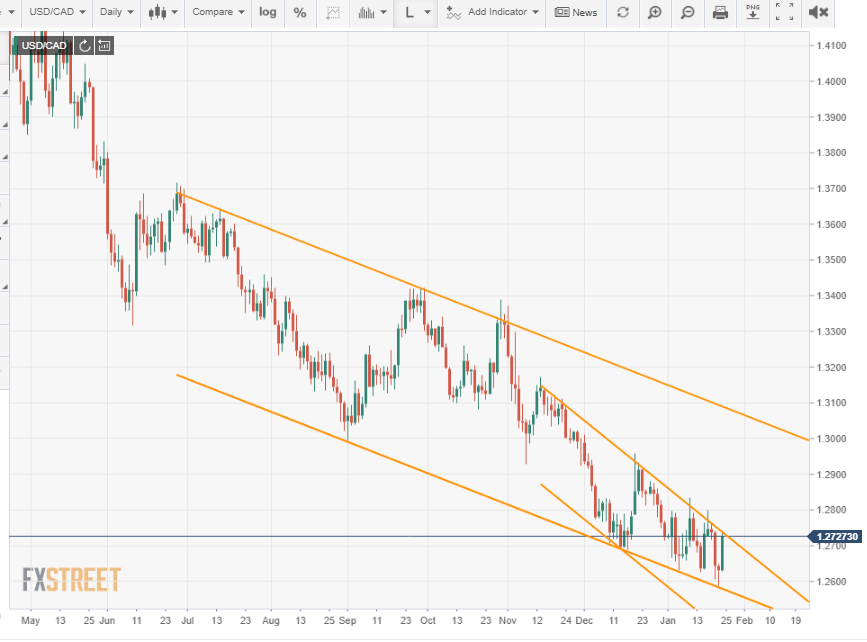

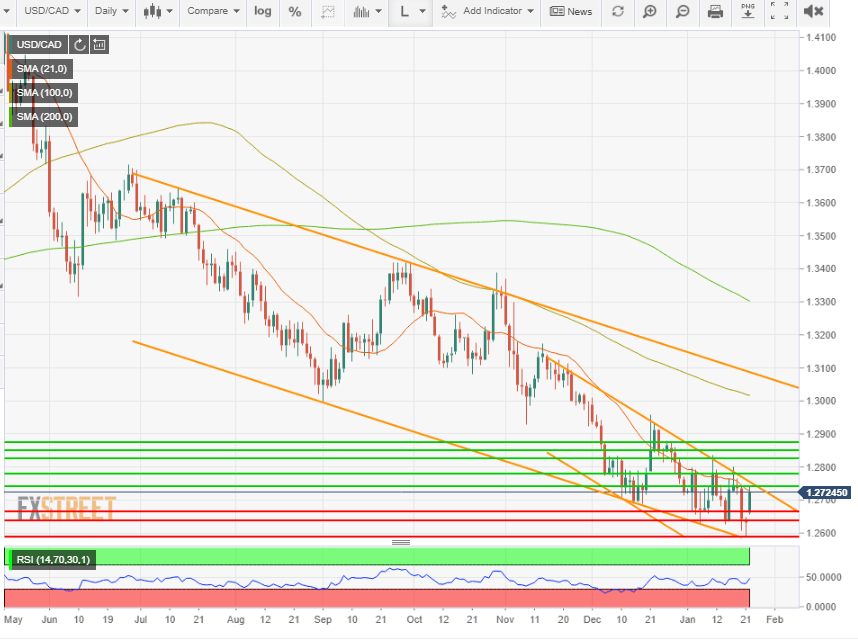

USD/CAD technical outlook

The double descending channels are the chief graphical formations. The USD/CAD movement down over the past five weeks has been contained by the lower border of the long term channel (origin late June) and the upper border of the steeper and more recent channel (origin mid-November). The combination forms a downward flag or pennant in traditional technical analysis and predicts further losses.

Resistance lines are more plentiful, closely spaced and recently traded. Near support at 1.2665 and 1.2640 have moderate substance from action this year while the deeper lines reference levels from 2018.

The Relative Strength Index at 47.86, given the sharp rebound from Thursday's low, is a buy signal. The 21-day average at 1.2727, the close on Friday, is likely to be crossed at Monday's open in Auckland and is not meaningful resistance. The 100-day average at 1.3016 and the 200-day at 1.3302 are external to the current technical scene.

Resistance; 1.2740; 1.2780; 1.2825; 1.2850; 1.2876

Support: 1.2665; 1.2640; 1.2590; 1.2550

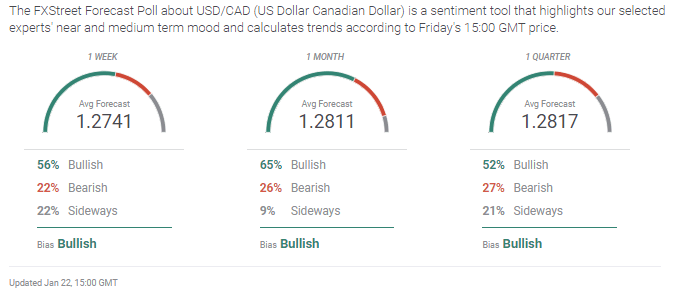

USD/CAD Forecast Poll

Change is brewing in the FXStreet Forecast Poll with a bullish view out to the quarter. Initial gains in the USD/CAD are modest but a move above 1.2800, envisioned in the one-month forecast, would place the pair above all trading in 2012 and provide a firm base for further increases.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.