USD/CAD Weekly Forecast: The pandemic analysis

- USD/CAD gains 1.5% on the week as risk-aversion returns.

- Technical support at 1.3130 proves to be resilient.

- Rising COVID-19 brings back the specter of closed economies.

- WTI falls 10% as France and Germany begin limited restrictions.

- FXStreet Forecast Poll predicts a false breakout.

The USD/CAD rose smartly last week gaining 1.5% as the second wave of the pandemic in Europe and the United States revived the general dollar safety-trade though the fear and the greenback remained far from the March panic high.

After opening at the support line of 1.3130 on Monday the day's close at 1.3185 displayed a clear bias, but it was the successful breach of the resistance band at 1.3220-1.3250 in the hourly chart on Wednesday that sealed market intentions. After that break, it was a straight run to 1.3300 and consolidation for the balance of the Thursday and Friday sessions.

The USD/CAD had departed its six-month pandemic descending channel on September 21. The secondary October trend line which had begun on September 30 was intersected at 1.3125 by the Friday close on October 23. The Monday (10/26) double break was given added emphasis as it exited that month-long pattern and rebounded from the 1.3130 support line.

Canadian data was mildly disappointing with the Raw Material Price Index, which measures the cost of key raw materials paid by manufacturers, falling 2.2% in September. The Industrial Product Price gauge which tracks the prices received by producers for major commodities, dropped 0.1% in September on a 0.1% forecast and a 0.3% gain in August.

Canada is one of the few industrial countries that track its Gross Domestic Product (GDP) monthly and though August's 1.2% result was stronger than the 0.9% forecast but less than half the 3.1% expansion in July.

The Bank of Canada left its base rate unchanged at 0.25% as expected in its Wednesday decision and said that “growth is expected to slow markedly, due in part to rising COVID-19 case numbers.” It also noted that “oil prices remained about 30% below pre-pandemic levels.”

The US Durable Goods Orders for September came in at 1.9% on a 0.5% estimate. Business spending was 1%, double the identical 0.5% forecast, and when combined with the 0.3% positive revision for August to 2.1% they confirmed that consumer and business spending were the main support for third-quarter GDP.

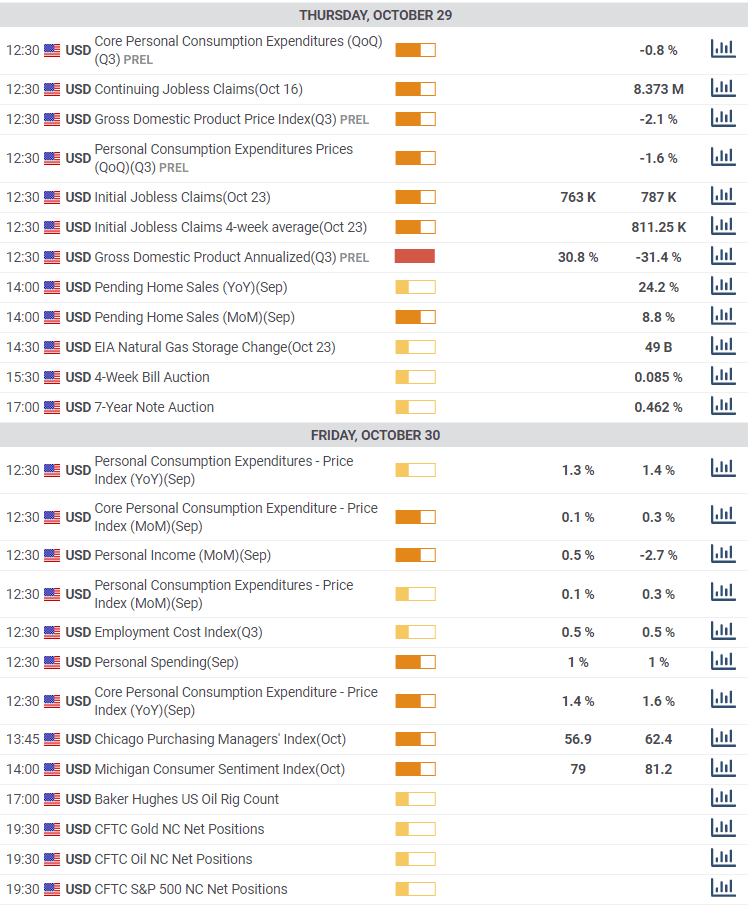

Initial Jobless Claims and Continuing Claims at 751,000 and 7.756 million in their latest weeks were both the best since March.

Third-quarter annualized GDP was 33.1%, more than replacing the 31.4% decline in the previous three months and better than the 31% consensus forecast.

Personal Income at 0.9% in September more than doubled the 0.4% estimate and Personal Spending rose 1.4% on a 1% prediction. Core PCE prices were 1.5% higher on the year, a bit under the 1.7% projection and the downward revision in August to 1.4% from 1.6% were signs that rising consumption has not restored pricing power to retailers.

WTI

West Texas Intermediate (WTI), the North American crude standard, fell 9.89% on the week as global growth expectations faltered under COVID-19 lockdown threats with Germany, France and the UK beginning limited closures. The commodity is at the bottom of its five-month range with initial support at $34.50 and the wide price range below a product of the March and April market panic.

USD/CAD outlook

Markets have taken up their pandemic worry beads again.

American and Canadian equities had their worst week since the initial panic in March. In the US the S&P 500 lost 4.99% closing at late September levels and the Toronto composite lost 3.87%.

The inconclusive break on September 21 of the six-month down channel has gotten a second boost from the action this week. The technical nature of the September move and the lack of a fundamental change in the USD/CAD became clear after the pair plateaued below the 1.3400 resistance line and then resumed its decline.

Despite the sharp ascent on Wednesday, the pair remains below the 1.3400 resistance which was briefly approached on Thursday at 1.3389.

It is unclear whether this round of the pandemic will prompt governments to the same stringent and economy-destroying measures that transpired in March and April. At the moment it appears not and the decision point is probably a few days or weeks ahead and will depend on the success of the various health systems in dealing with the new cases.

The bias in the USD/CAD has shifted to the upside but is not the panic rush of the spring as the full closure of economies do not appear to be contemplated.

Technically, the resistance at 1.3400 remains paramount as that is where the September attempt to move higher failed. If that can be crossed then the break should acquire the momentum to reach 1.3500 and higher.

Canada and US statistics November 2-November 6

Markit's Manufacturing PMI is forecast to slip to 55.6 in October from 56 in September.

The Canadian Unemployment Rate is forecast to rise to 9.7% in October from 9.0% in September. It would be the first increase since May. The Net Change in Employment added 378,200 jobs in September. The Ivey Purchasing Managers' Index was 61.1 in October.

Canada's employment statistics on Friday have the best chance of eliciting market attention. If the pessimistic forecast for unemployment is incorrect it will support the loonie.

In the US the main event is the Presidential election on Tuesday. Former Vice-President Joe Biden leads President Donald Trump in the polls but the vote in the decisive swing states of the upper Mid-West is much closer.

Manufacturing PMI from the Institute for Supply Management for October is expected to rise to 55.6 from 55.4. The New Orders Index is forecast to drop into contraction at 45.9 from 60.2. The Employment Index is projected to fall to 40.9 from 49.6.

The Services PMI is forecast to be unchanged at 57.8 in October. Employment is expected to drop to 49.8 from 51.8, New Orders will fall to 49.4 from 61.5. The ADP Employment Change payroll is expected to add 526,000 workers in October after rising 749,000 in September.

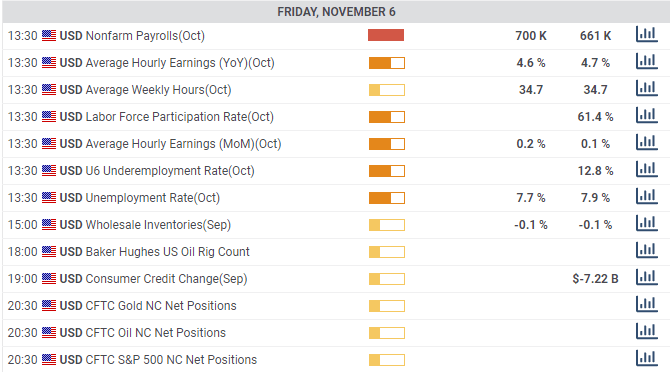

Initial Jobless Claims are predicted to rise to 770,000 in the last week in October from 751,000. Continuing Claims are forecast to increase to 8.103 million from 7.756 million.

The Federal Reserve will leave its base rate unchanged at its Thursday meeting and no change is expected in its other economic support programs.

Nonfarm Payrolls for October will add 700,000 new jobs following September's 661,000 addition. The unemployment rate should fall to 7.7% from 7.9%.

The US electorate is unusually volatile this year and the election and its aftermath will dominate news and markets. The reaction to the election may be the most important development. The polls have been tightening and the late run looks much like the 2016 vote. If Trump wins the potential for violent protest in many cities seems high.

For markets the question is will US civil unrest, if it happens, play to the dollar's safety status as the COVID-19 cases have or will traders flee to the euro, yen and farther shores? The surpassing rarity of political violence in the United States makes the prognosis an unknown of the highest order.

USD/CAD technical outlook

The USD/CAD increase has brought he Relative Strength Index (RSI) to 59.34, about half-way to over-bought status but it is not a sell signal. The 21-day moving average at 1.3207 supports the line at 1.3230. The average at 1.3330 is just above the Friday close of 1.3319 and offers moderate resistance. The 200-day line at 1.3545 is out of the current picture.

The break of the descending channel on September 21 and the Wednesday break at 1.3130 await confirmation above 1.3400.

Support: 1.3300; 1.3250; 1.3220; 1.3130; 1.3050

USD/CAD Forecast Poll

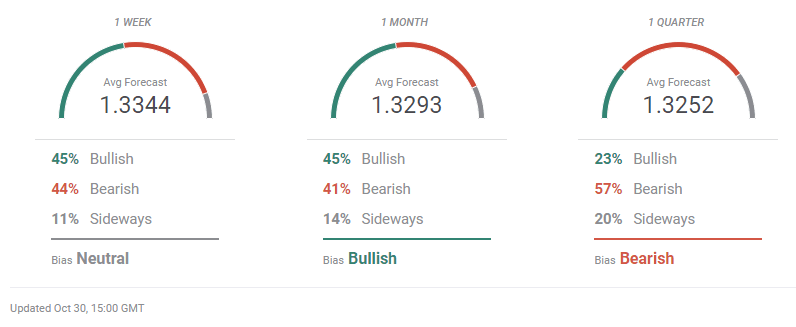

The gain in USD/CAD has not convinced our FXStreet Forecast Poll experts that a new uptrend has started. The one-month and one-quarter views are less than 50 points above the forecasts last week. Much will depend on the response of the markets to the advancing pandemic cases and the various government measures to combat the spread.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.