US Service Sector October PMI Preview: That turned corner must be around here somewhere

- Services PMI forecast to rise after September’s three year low.

- Manufacturing PMI recovered in October from decade trough but still weaker than expected.

- Payrolls maintained strength in October, revisions to August and September were robust.

The Institute for Supply Management (ISM) will release its Non-Manufacturing Purchasing Managers Index (PMI) for October at 15:00 GMT, 10:00 EST, November 5th.

Forecast

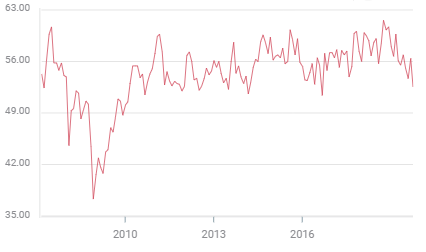

Services PMI is estimated to rise to 53.4 in October from 52.6 in September. The business activity index is expected to slip to 55.0 from 55.2. Employment was 50.4 in and 53.1 in August. New orders were 53.7 in September and 60.3 in August.

ISM business outlook

Business Sentiment has taken a long battering this year as the twin threats of the US China trade war and the British exit from the EU appeared set to drive the global economy into the slow lane or off the highway altogether.

The purchasing managers’ index for services fell from 60.8 last September, a 14 year high, to 59.7 in February and 52.6 seven months later.

Non-Manufacturing PMI

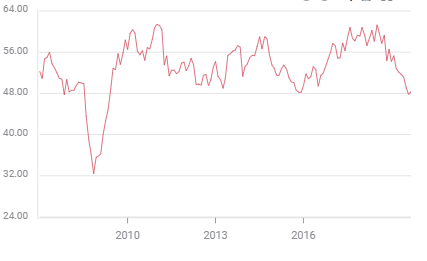

Manufacturing was even more stricken. It went from 60.8 in August 2018, to this year’s high at 56.6 in January and then plunged into three months of contraction at 49.1 in August, 47.8 in September and 48.3 in October.

Manufacturing PMI

Yet despite the pessimism the worst has not happened.

China and the US seem ready to sign a preliminary, or phase one deal sometime this month. If this is not the comprehensive trade arrangement once hoped for it does reverse the tariff escalation of the last two years and offer modest promise for the future.

In Britain the approved but not implemented exit agreement may get its final assent from the electorate at the December 12th general election.

Manufacturing PMI

Manufacturing PMI executed a small turn in October rising to 48.3 from 47.8 through remaining under the 50 demarcation and in contraction.

Several of the component indexes deepened their decline last month. Production fell to 46.2 from 47.3, order backlogs dropped to 44.1 from 45.1 and inventories rose to 48.9 from 46.9.

But as with the overall index, three of the most forward looking components reversed direction though only one moved into expansion. Employment rose to 47.7 in October from 46.3, new orders climbed to 49.1 from 47.3 and most startling new export orders soared 9.4 points to 50.4 from September’s 41.0

Consumer and business spending in the US economy

The US economy has not wholly participated in the business sector pessimism of the past year, slowing but keeping an even keel and in most of the labor and consumer indicators maintaining a healthy expansion.

Gross domestic product dropped from its 3.1% pace in the first quarter to 2.0% in the subsequent six months. Job creation has fallen from the very strong 245,000 in the three-month moving average in January to 177,000 in October. But if the Labor Department estimate of 46,000 striking GM workers subtracted from October’s total is correct the average is last month was 191,000.

Annual wage increases have been at 3.0% or better for 15 months and unemployment has been within fractions of a percentage point of a half-century record for 18 months.

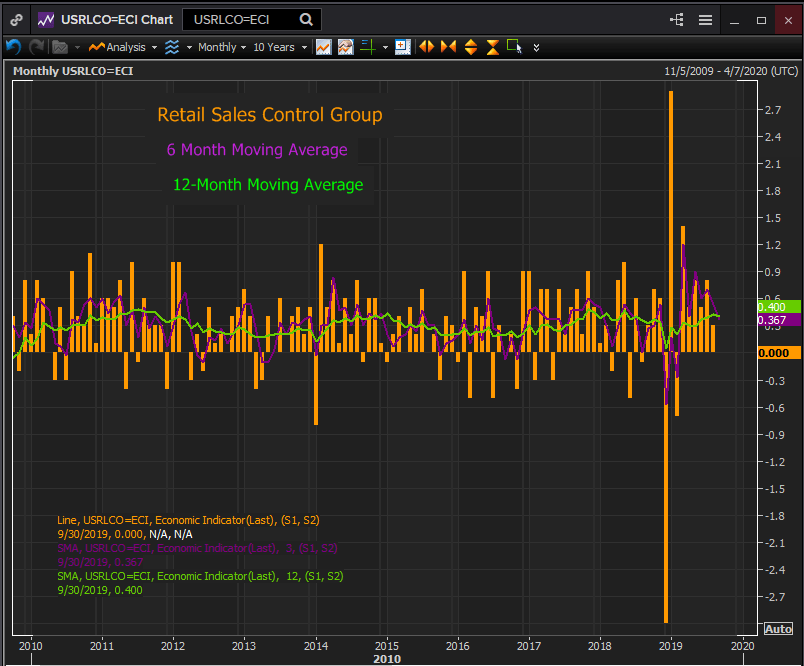

Retail sales have held up well through August with the six-month moving average of the control group at 0.533%. September’s flat reading brought that down to 0.367%. Consumer confidence has also rebounded to the mid-levels of the last two years which are the best in two decades.

Reuters

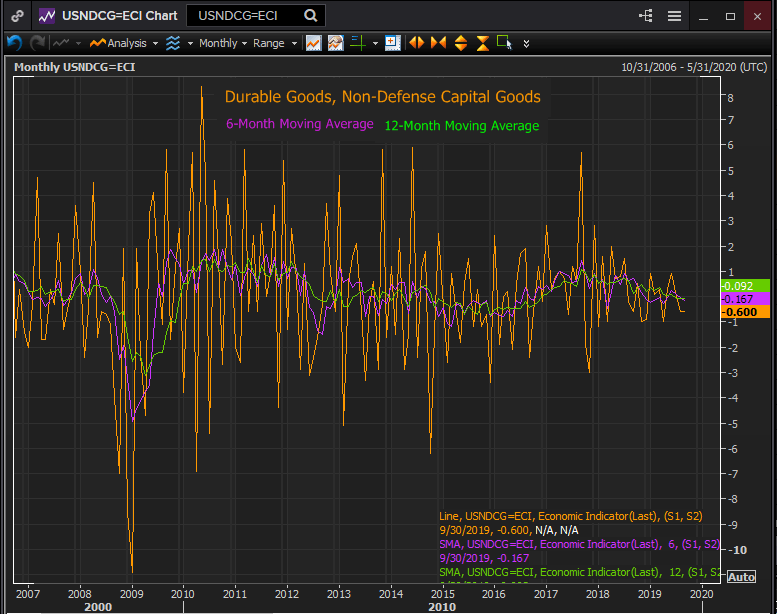

The problem for almost a year has been business investment. The durable good category of non-defense capital goods ex-aircraft was negative in both the six-month and 12-month moving averages at -0.167% and -0.092% respectively in September.

Reuters

Conclusion

The split between an active, happy and generous consumer and a depressed and straitened business executive is unusual. Normally business takes its cues from the dominant American consumer sector. When households are spending companies will strive to meet demand and err on the side of optimism and investment.

The China trade dispute, cited by the Federal Reserve in three rate cuts, and the largest reason for the yearlong pullback in business spending may be ending its run as the great economic instigator.

Equities, with records in the S&P 500 last week and the Dow on Monday, are predicting growth ahead as are rising Treasury rates after August’s recession scare.

If China and the US have reached an operational agreement business executives may turn their attention and resources to the neglected investment needs of the last twelve months.

It should not take much to spur optimism in the US business community after its unaccustomed internationalist pique of this year. The small turn in manufacturing may predict a more substantial move in services.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.