US Retail Sales March Preview: Waiting for the inflation hammer to drop

- US economic growth and Fed policy depend on consumer spending.

- Inflation has poleaxed consumer sentiment and threatens consumption.

- American wages are failing to keep pace with 8.5% inflation.

- Producer prices soar 1.4% and 11.2% in March, both records.

In normal times the consumer can be counted on to keep the US economy humming. Over the last year household spending has come under increasing threat from rampaging prices. It is an open and crucial question how long the inflation-battered US consumer can continue to fund the current economic expansion.

Retail Sales are forecast to rise 0.6% in March, doubling the February gain. Sales ex-Autos are expected to climb 1% after a 0.2% increase in February. The Control Group category, which mimics the consumption component of GDP, is projected to rise 0.2% after falling 1.2% in February.

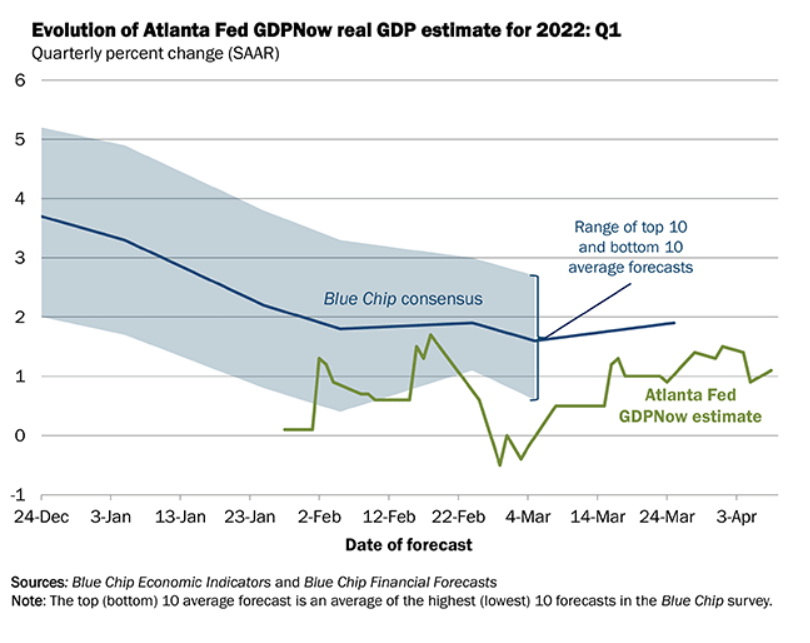

The Federal Reserve has embarked on a rate tightening regime that could, by year end, bring the fed funds rate to 2.5% or higher from its current 0.5%. That program is wholly contingent on an expanding US economy. The Atlanta Fed’s GDPNow program estimates first quarter growth at 1.1%, with a new calculation due after Thursday’s sales figures. There is very little leeway in US growth. If the economy contracts in the quarter just ended, it is difficult to see how the Fed hikes 0.5% on May 4 as widely predicted.

Sales have averaged 2.6% in the two months of the first quarter reported. That excellent gain is due to the 4.9% increase in January that followed a 0.5% overall decline in the last quarter of 2021. Given the huge jump in January sales, the quarter is likely to remain positive for consumption and GDP even if the March figures take an unexpected plunge.

Let's take a look at the sales indications for March.

Retail Sales: Positive indicators

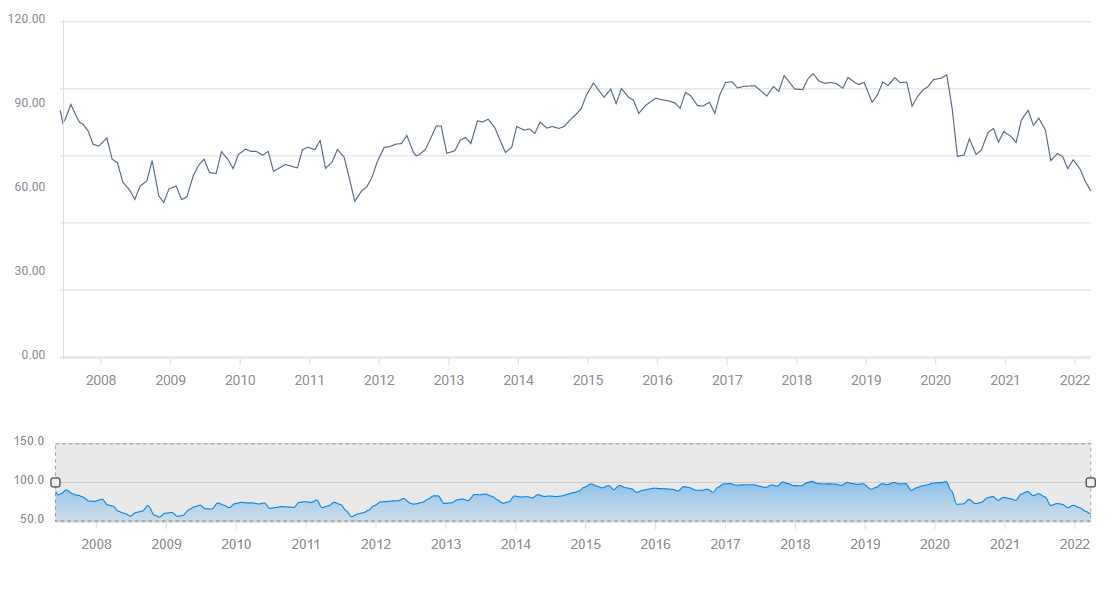

The best hope for strong consumption is Americans' tendency to spend regardless of external circumstances. Consumers say they are very unhappy. The Michigan Survey has been near recessionary lows for eight, soon to be nine months, and it has not had a noticeable impact on spending.

Michigan Consumer Sentiment

Behind the resilience is the robust job market. Payrolls have averaged 596,000 for six months and 482,000 for 12. The unemployment rate was 3.6% in March, a level in former times considered beyond full employment. Initial Jobless Claims were 166,000 in the latest week, the second lowest total in the 55-year series. Available positions in the Job Openings and Labor Turnover Survey (JOLTS) have averaged almost 11 million for nine months, an all-time record. Anyone in the US who wants to work can find a job.

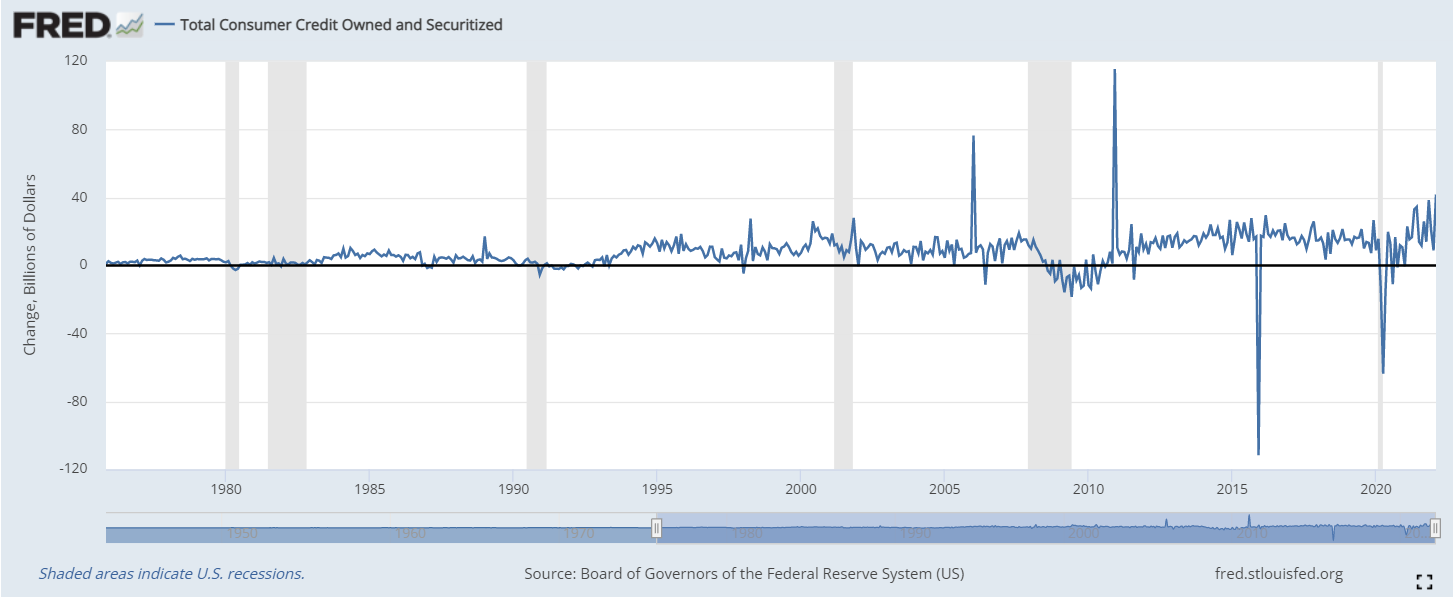

Consumer credit expanded $41.8 billion in February, far more than the $6.8 billion expected and the third highest monthly total in a statistic that goes back to 1943. The extravagance can be interpreted in two ways. The willingness to assume more debt might be due to the confidence generated by the job market, or it might be an expedient necessary to shore up the inflation erosion of purchasing power.

Consumer Credit

Retail Sales: Negative indications

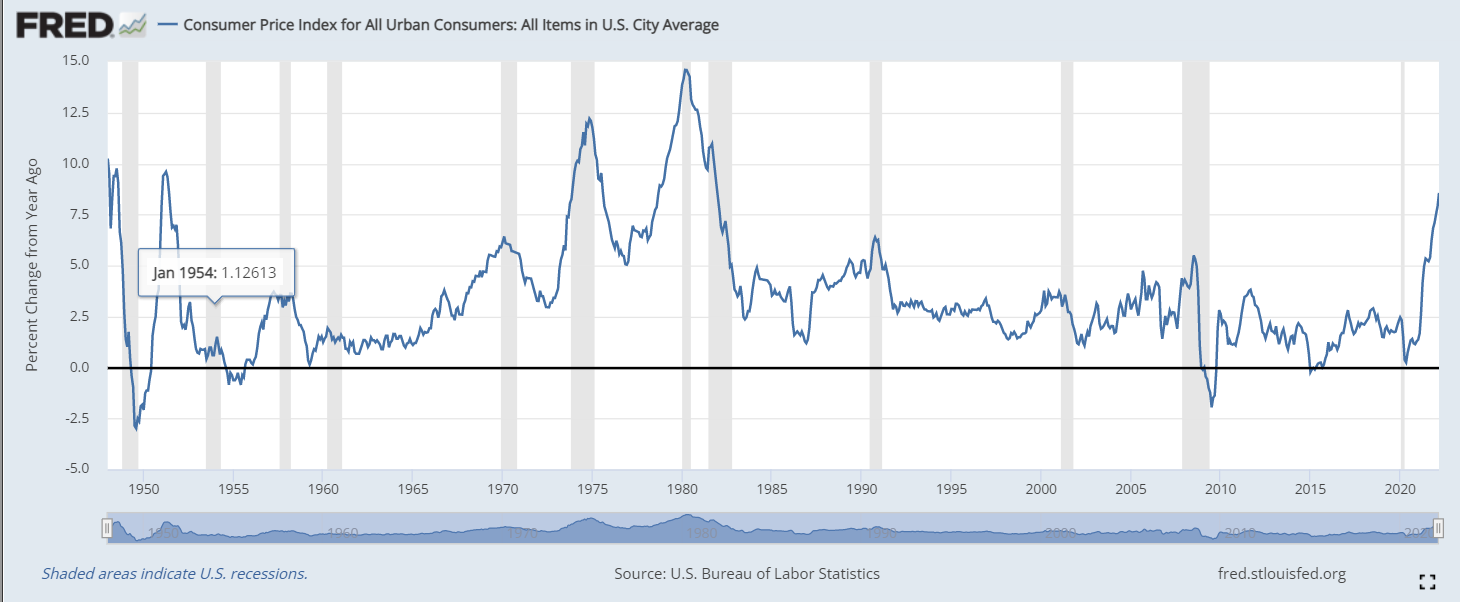

Inflation is the main culprit. It is responsible for the dismal consumer sentiment reading, but more importantly, it has long-since overtaken wage increases and is draining consumer finances every month. In March annual real inflation-adjusted income dropped 2.7%, despite a 5.6% increase in Average Hourly Earnings. It was the 12th straight month of decline. That is a financial impact consumers will find impossible to ignore.

Although headline CPI rose 8.5% annually in March, many necessities saw much greater increases. Overall food expenses jumped 8.8% but home grocery costs climbed 10%, another record. Meat, poultry, fish and eggs were up 13.7%, beef 16%, dairy and related products 10.3%. Cereal and bakery products are up 9.4%, fruits and vegetables 8.5%.

CPI

Gasoline was 18.1% higher in March and up 48% for the year. Fuel oil vaulted an astonishing 70.1% in 12 months, natural gas was up 21.6% and domestic electric charges jumped 11.1%.

When the basic cost of living rises so much and so quickly, CPI was 1.4% last January, adjustments to household budgets are inevitable. At first, families will maintain spending by dipping into saving and extending credit, hoping that inflation subsides. Eventually, adjustments will begin in discretionary purchases and that will continue until expenses are in line with income. Has that process begun?

Consumer inflation has been 5% or higher for 11 months and there is no end in sight to the elevation.

The annual Producer Price Index (PPI) soared 11.2% in March, up 1.4% in the month, from 10.3% in February. The core rate jumped 9.2% from 8.7%. These are the highest PPI readings in the 12 year series. Increases of this magnitude, especially in the current environment, are sure to be passed on to consumers. Inflation may not be peaking, it may not even be finished accelerating.

PPI

Market conclusion

Retail Sales and consumption in general are the economic keys to the next two quarters. If consumers defy both their own outlook and their shrinking wallets and maintain a modest if not expansionary attitude, the US economy should be able to avoid recession and the Federal Reserve will continue its rate increases.

If consumer spending stagnates or falls, business expansion will follow and US economic growth will be in serious question. As noted above, at 1.1% in the Atlanta Fed estimate, there is no room for weak Retail Sales.

Markets will react in a straight line with the strength of the sales figures. Better than expected results support Treasury rates and the dollar. Equities should be able to ignore the prospect of higher interest rates as strong sales mean an expanding economy.

Weak or negative sales raise a host of problems about the second quarter but the immediate reaction will be lower Treasury yields, a lower dollar and fading equities. For the stock market, the prospect of a recession is more daunting than higher interest rates.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.