US Retail Sales: Consumers ignore the critics so does the credit market

American households continued one of their strongest sales runs in years buying new cars and keeping their keyboards busy shopping online as the tight labor market provided the highest wage gains in a decade.

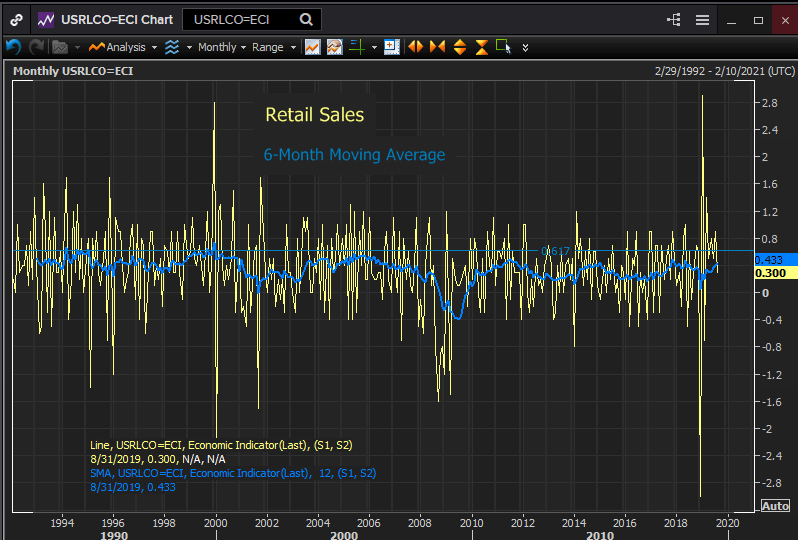

The value of retail sales rose 0.4% in August reported the Census Bureau on Friday and the July total was revised 0.1% higher to 0.8%. The consensus estimate from the Reuters survey of economists was for a 0.2% gain.

Reuters

Sales excluding automobiles were flat for the month, missing the 0.1% forecast and down from July’s robust 1.0% increase.

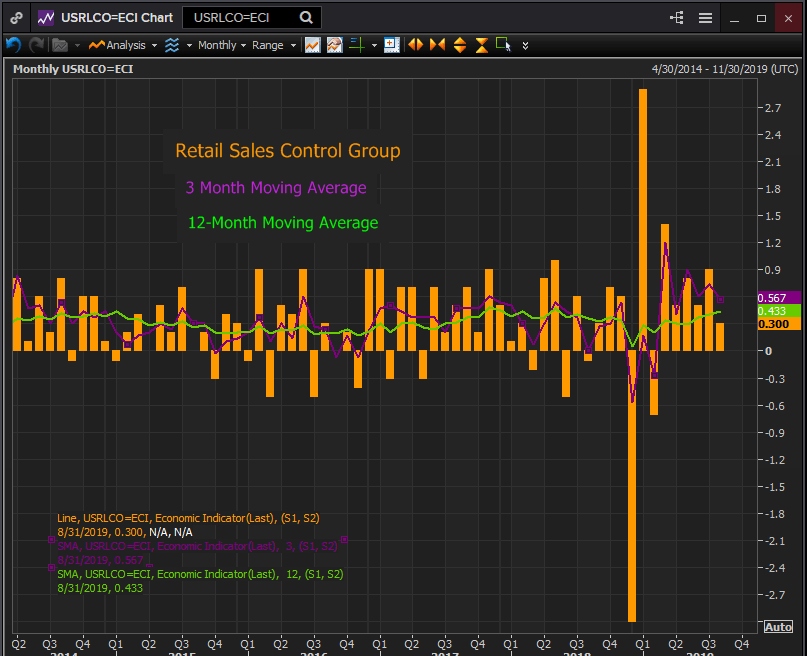

The government named control group which excludes food services, car sales and gasoline sales and building materials and is used to calculate the personal consumption expenditure component of GDP rose 0.3% as expected, and the July result was revised to 0.9% from 1.0%. Control group sales increased at an 8.1% annual rate in the three months to August, down from the 9.4% pace in July.

Reuters

Consumers have been spending steadily this year spurred by the availability of work and rising compensation. Retail sales have increased for six straight months with the 12-month moving average at 0.433% its best level since May 2018.

Treasury Yields

Treasury yields added to their recent gains with the generic 10-year rising 10 basis points to 1.88%. The return on this benchmark government security has turned sharply higher this month rising 44 points in 10 days after an intraday low of 1.43% on September 3rd. The 2-year yield climbed 6 points to 1.78% (12:15 EDT). It has increased 35 points since its low on September 4th.

The spread between the two key economic interest rates began to narrow at the end of July and inverted for several days at the end of August reaching a 4 point reversal on August 28th.

Reuters

The inversion of the 2-10 spread, where the yield on the long bond is less than the shorter has been considered a reliable indicator of a recession six months or more in the future. The logic is that a declining economy will require the support of lower rates as the recession approaches. In anticipation the credit markets buy the longer dated notes driving rates lower.

This inversion has been short-lived. By August 30th rates were equal at 1.51% and they have moved rapidly in the opposite direction since. As of this writing the spread is 10 points. It was 13 points on July 31st.

China Trade

Trade tensions with China and Brexit and the slowing global economy have mattered less to consumers than the positive impact on household budgets of employment and compensation.

The almost two year old dispute with Beijing showed some signs of progress this week as China said it is encouraging companies to buy US agricultural products. The US had previously delayed imposition of some of the tariffs that had been scheduled to start on September 1st. Talks between the world’s two largest economies are slated to resume in October.

The Federal Reserve has made preserving this expansion its priority policy goal and is expected to reduce the fed funds rate by a second quarter point to a 2.0% upper target when it meets on the 17th and 18th of this month.

Retail Sales Components

Retail sales were healthy overall though seven of 13 major classifications saw declines including restaurants receipts which fell the most in a year. General merchandise vendors and clothing stores also declined. Spending at automobile dealers rose 1.8% the most since March

Non-store sales, the category that covers internet shopping climbed 1.6% following July’s 1.7% gain.

Michigan Consumer Sentiment

In another release the preliminary Michigan Consumer Sentiment Index for September came in at 92.0, slightly better than the 90.9 forecast. The August score of 89.8 represented a sharp drop from July’s 98.4 level. The Current Conditions Index rose to 106.9 from 105.3 and the Expectations Index increased to 82.4 from 79.9.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.