US October Retail Sales Preview: Consumers keep faith with the economy

- Retail sales projected to rise after the first drop in six months.

- Control group GDP component to recover following a flat September.

- Labor market remains a strong backing for consumption.

The US Census Bureau will issue its advance report on Monthly Sales for Retail and Food Services for October on Friday November 15th at 13:30 GMT, 8:30 EST.

Forecast

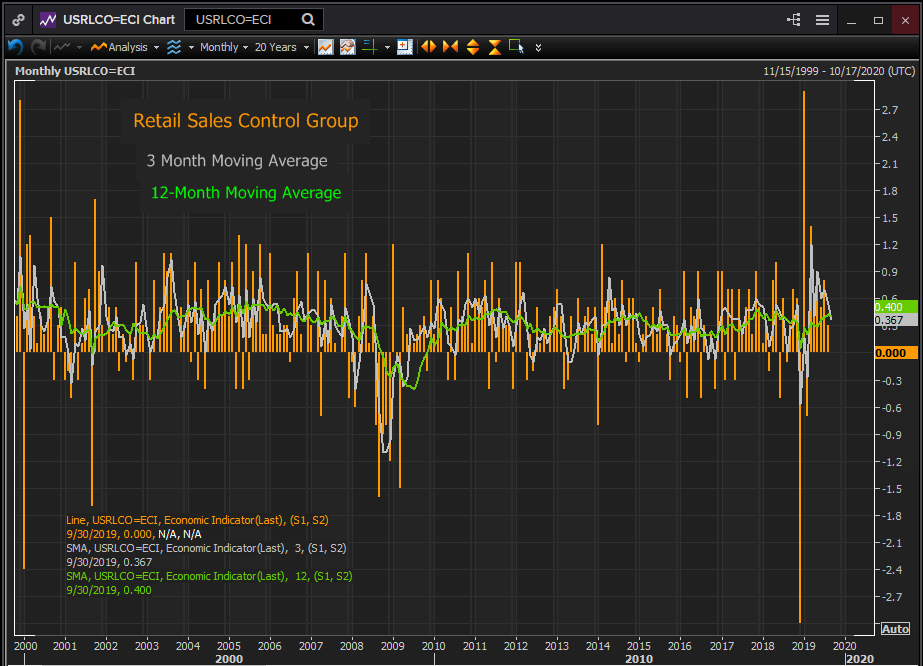

Retail sales are projected to 0.2% in October after falling 0.3% in September. The retail sales control group, the Bureau of Economic Analysis’ GDP component is expected to climb 0.3% after an unchanged reading in September.

Retail sales and economic growth

While annualized GDP has subsided 37% this year from 3.1% in the first quarter to 2.0% in the second and 1.9% in the third, the control group category of retail sales, used by the BEA to calculate consumption, has improved modestly.

The monthly average for the nine reported months of this year through September is 0.722%. This is overstated because of the huge variation around the government shutdown in January. Control group sales were down 3% in December and up 2.9% in January due to Census admitted reporting problems.

Any monthly average that included January and not December, as September’s year-to-date average does, gives a false impression of strength. The 8-month average from February to September is 0.45%. The 3-month moving average was 0.1.67% in January and 0.367% in September.

Reuters

The decline in GDP was largely caused by the China trade dispute related drop in business investment. The non-defense capital goods category of durable goods orders, a common analog for business spending, sank from 0.358% in the 12-month moving average in January to 0.067% in June, 0.058% in July and -0.092% in August and September. These are the first negative annual averages since November 2016.

Gross domestic product as calculated by the BEA consists of four general categories: consumer spending or consumption, business spending, government expenditures and net exports.

Retail sales and the labor market

The excellent performance of the US labor market over the past two years has been the foundation on which the retail sales numbers and GDP have been built.

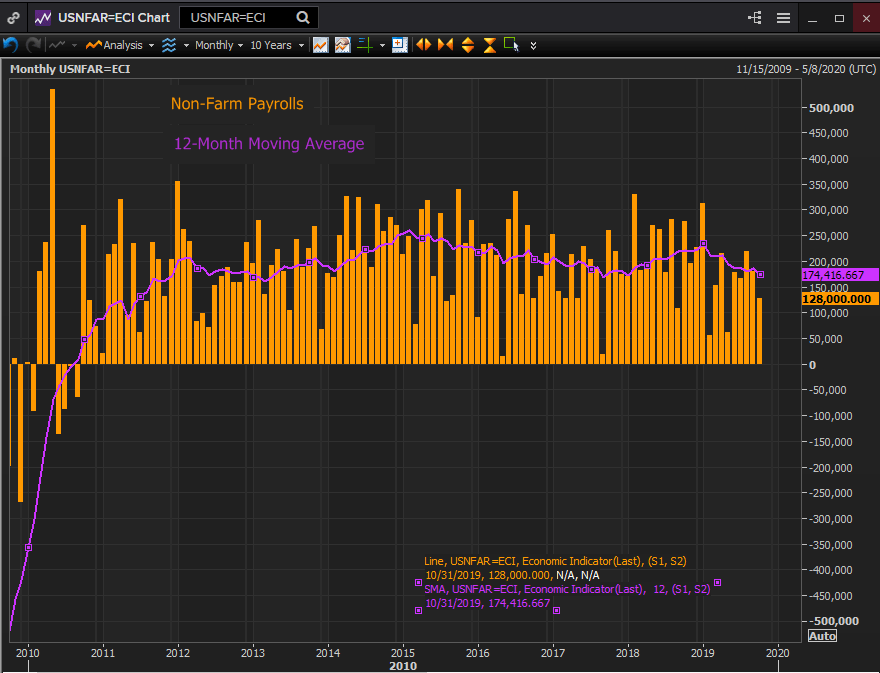

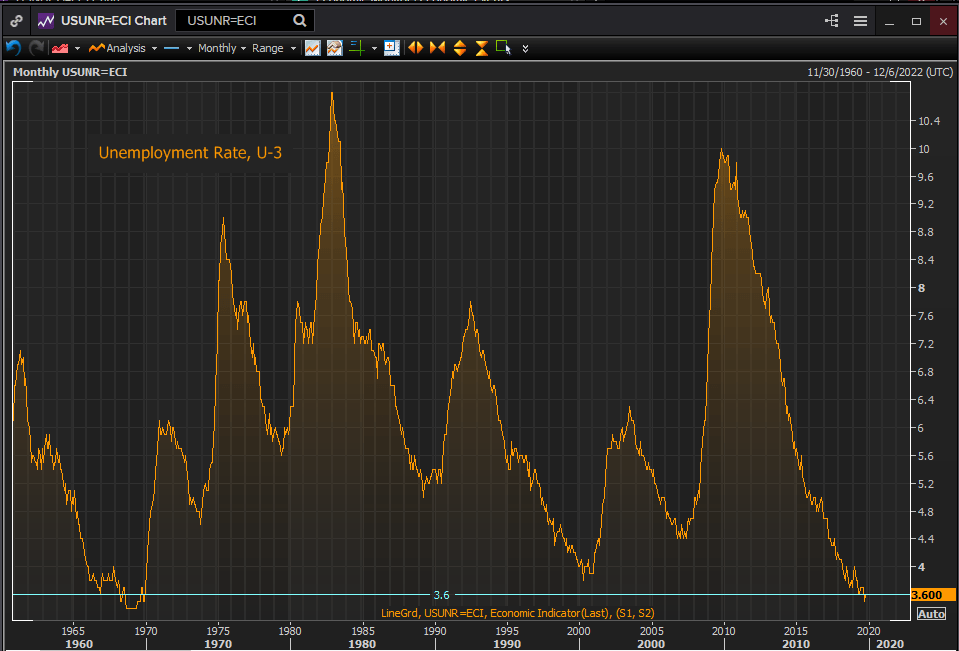

Non-farm payrolls have averaged 167,000 a month through October and 174,000 over the past year, well above the 125,000-150,000 needed to provide work for first time workers. Annual wages have gained 3% or more for 15 consecutive months and the 3.6% unemployment is nearly a 50 year low. The jobless rate has been at or below 4% for 20 months the longest run since the last half of the 1960s and the majority of that time, 17 months out of 20, the rate has been below 4%.

Reuters

These figures would be remarkable in almost any period of economic growth, but in the 11th year of the longest post –war expansion they are extraordinary.

Reuters

Retail sales and consumer sentiment

Consumer sentient reflects the success of the economy in creating employment and boosting wages.

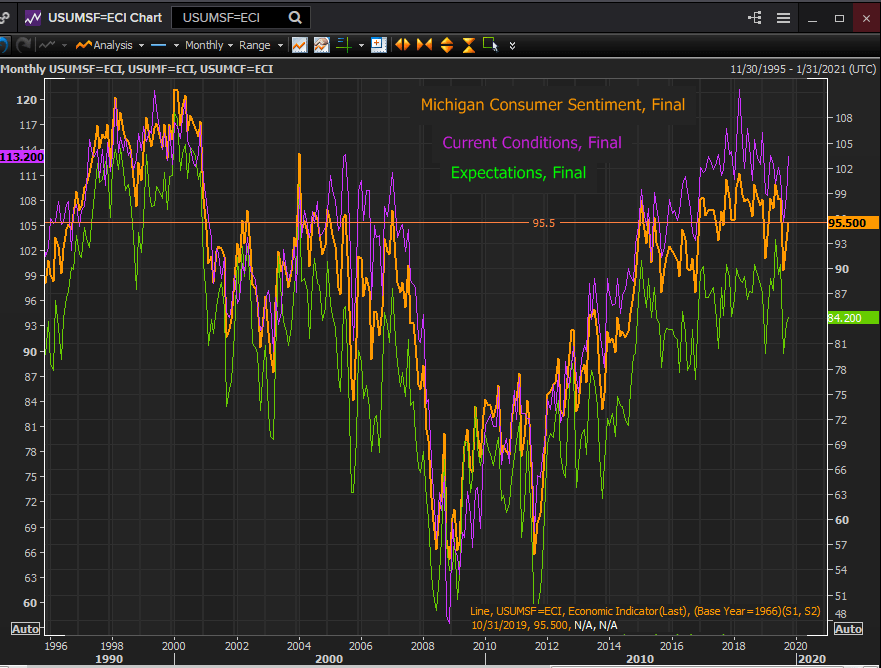

The Michigan Survey of Consuemr scored 95.5 in October near the mid-point of its three year range and among the best scores since the boom of the second Clinton administration from 1997-2000.

Reuters

Tellingly it is the current conditions index that has registered the highest sustained readings over the past three years. American have not been so satisfied with their economic conditions in over two decades.

Federal Reserve and the dollar

The end of the Fed temporary rate campaign with the October 0.25% cut, the third in a row this year, is an acknowledgement, tempered with hope, that the US China trade dispute and the British exit from the EU are on their way to be solved, or at least, much diminished as a threat to US and global growth.

The fed funds futures place the odds for a rate cut at the December 11th meeting at a vanishingly small 3%. For the January 29th FOMC they are 19.1%, March 20th 28.9%, April 3oth 36.4% and June 10th 42.8%. The do not reach 50% until the July 20th meeting at 51.3%. For the last FOMC of next year on December 16th the odds for one cut or none throughout the year are 75.4%

The Fed’s 0.75% in reduction this year was not based on the performance of the US economy but on the perceived dangers from trade, Brexit and their impact on the already weakening global economic growth.

The contrast in rate policy to the European Central Bank’s newly re-minted quantitative easing bond purchases is instructive for the path of the dollar in the remaining months of 2019 and into 2020. It will be hard for the euro and other currencies to gain traction against the US dollar while a restrained Fed presides over a growing American economy and an effervescent consumer.

Conclusion

The labor market has kept faith with the American consumer and US households have kept faith with the US economy. Consumption has kept the economy afloat over the past year even as political and economic wrangles threatened to undermine consumer sentiment.

If the China trade war is truly defused business spending will return to keep pace with consumption and fill in the gaps left by a year of denial and the US economy will further extend this record expansion.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.