US Nonfarm Payroll October Preview: Inflation to the rescue?

- National payrolls projected to add 425,000 after 194,000 in September.

- Services and manufacturing employment indexes remain positive.

- ADP employment at 571,000 was much stronger than anticipated.

- Improving NFP will support the taper, US Treasury rates and the dollar.

With the Federal Reserve’s taper announcement out of the way, markets can return to reading the economic tea leaves for the direction of the US labor market.

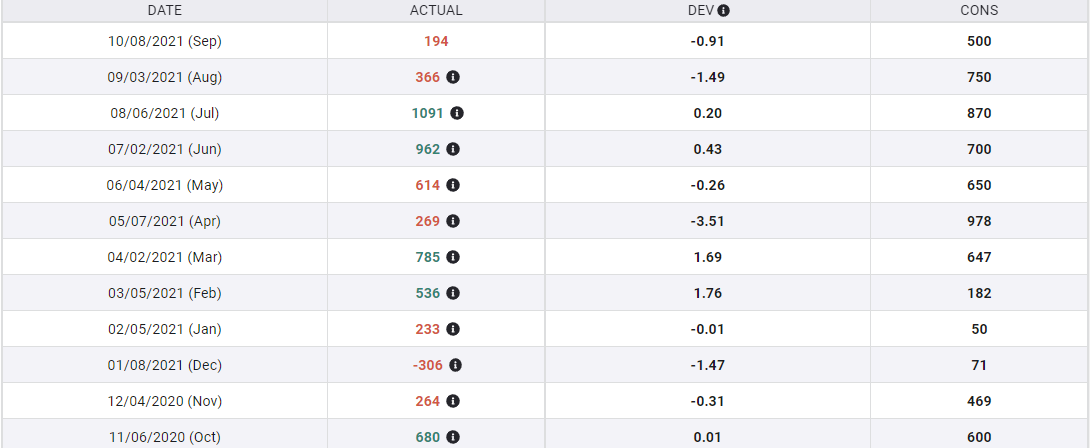

Nonfarm payrolls are forecast to rise by 425,000 in October. September’s major disappointment of 194,00 hires was the lowest monthly figure since last Decembers’ loss of 306,000. The unemployment rate should have edged down to 4.7% last month from 4.8%, both pandemic lows. Average Hourly Earnings are forecast to rise 0.4% on the month and 4.8% on the year from 0.6% and 4.6% in September. The Labor Force Participation Rate is predicted to be unchanged at 61.6%.

Nonfarm Payrolls

Nonfarm Payrolls dropped 22.32 million workers in the March and April lockdown last year. Since then the fitful labor recovery has rehired 15.7 million employees, 70%.

Forward looking indicators are generally favorable to a continuing expansion of the US labor force. The declining nationwide Covid cases may help to encourage workers to seek employment.

Purchasing Managers' Indexes

Purchasing Managers’ Indexes (PMI) for the service and manufacturing sectors have maintained their expansionary outlook despite the difficulties in finding and securing workers.

The Manufacturing Employment Index from the Institute for Supply Management rose to 52 in October from 50.2 a month earlier. The forecast had been for 49.6, just below the 50 division between expansion and contraction. Over the past six months the index has bounced around the dividing line dropping below in June and August and averaging 50.8 for the period.

Manufacturing Employment Index

FXStreet

The Employment Index from the much larger services sector registered 51.6 in October down from 53 prior and missing the 53.3 estimate. This gauge has been more positive over the last six months, falling below 50 just once in June and averaging 52.8 for the half-year.

Business executives polled for this survey stressed that their difficulties in the labor market were not weak consumer demand but inability to find workers.

ADP

The Employment Change Report from Automatic Data Processing, the largest private payroll company in the US, listed 571,000 new hires in October, nearly half again as many as the 400,000 forecast. The 609,000 average for the last six months is the best of the recovery excepting the initial burst of rehiring in May and June last year.

Although the ADP data has been a poor predictor for individual NFP results over the past six months, the steady positive trend is an indication that the overall job market has not seriously deteriorated.

ADP

FXStreet

JOLTS

The Job Openings and Labor Turnover Survey (JOLTS) from the Bureau of Labor Statistics lists the number of jobs available in the US. For five straight months, from March to July the survey set a new record. In July the 11.098 million total was 47% higher than the top score from before the pandemic of 7.574 million in January 2019.

The weak payrolls reports in August and September were not caused by lack of opportunity. Though the September JOLTS report will not be issued until November 12, it will show the same massive overhang of unfilled positions.

JOLTS

FXStreet

Initial Jobless Claims

Initial Jobless claims have been declining almost continually since February. The four-week moving average has fallen from 836,750 in the first week of February to 284,750 in the final report for October. In comparison, the second week of March 2020, the last before the pandemic explosion, the average was 232,500.

Claims over the past month are running at levels that in the recent past would have been considered indicative of full employment. Employers are doing all they can to retain workers.

Initial Jobless Claims, 4-week moving average

FXStreet

Conclusion

The problems in the US labor market are manifestly not from employers. There are millions of unfilled positions, companies are desperate for workers. Initial claims, Employment PMIs, job openings and ADP all indicate a healthy outlook for hiring.

Individuals are choosing not to return to the workplace. Lingering pandemic diffidence, onerous vaccine mandates, extended unemployment benefits, lack of child care and the economic dislocations inflicted by the lockdowns have led to an unprecedented disparity between employment and work.

One likely cause which has not received much attention is the geographic distribution of work and employment. The highest unemployment rates are in the states which enforced the strictest lockdown. These closures destroyed many small businesses. Those jobs have not returned and will not until new businesses are created.

From a market perspective, strong payrolls are a guarantor for the Fed’s taper program which over time will lead to higher US interest rates and, until other central banks catch up, a higher dollar.

In an odd way the rampant consumer inflation inflation that was the barely stated motive behind the Fed’s bond taper may provide the incentive for many workers to return to their jobs.

When gasoline is almost 50% higher in a year and food costs are rising monthly, a steady job is likely to be seen as far more dependable than government largesse.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.