US Michigan Consumer Sentiment Preview: The Beijing express arrives in the station

- Sentiment to rise modestly in November continuing recovery.

- Labor market strength in job and wages underpinning outlook.

- China trade deal unlikely to have any positive effect as yet.

The University of Michigan will release its preliminary Survey of Consumers for November on Friday November 8th at 15:00 GMT 10:00 EST

The survey consists of three indexes--the Index of Consumer Sentiment, the Index of Current Economic Conditions and the Index of Consumer Expectations. Each is revised once. The survey began in 1978.

Forecast

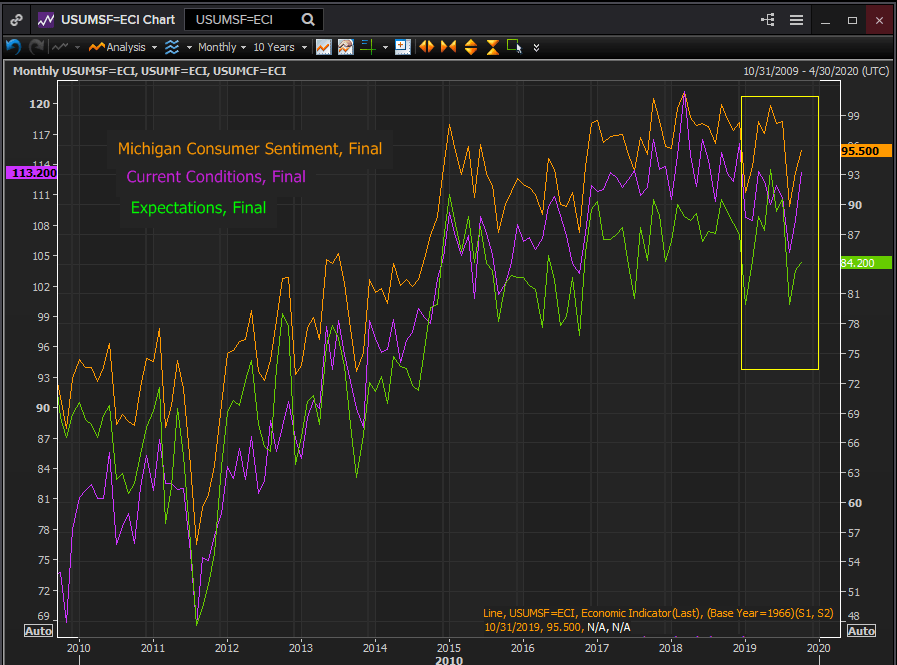

The Consumer Sentiment Index is expected to edge up to 95.9 in November from 95.5 in October. The Current Conditions Index is estimated to slip to 112.5 from 113.2 in October. The expectations Index will climb to 84.9 in November from 84.2 in October.

Consumer sentiment and the US economy

The American consumer has been caught this year between two forces. The labor economy, jobs, wages, participation and unemployment have all been good, excellent or stellar. Yet growing concerns from the trade war with China and slowing global growth, which have hit the manufacturing sector and its employment hard, and even at a remove Brexit have taken a noticeable toll on sentiment.

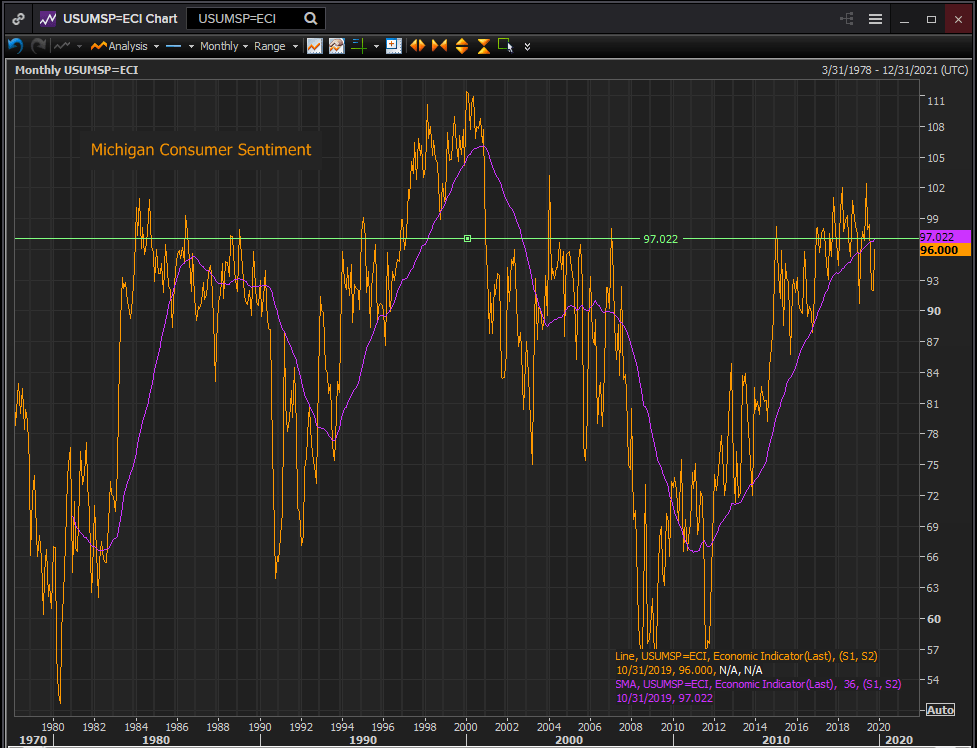

From the election in November 2016 to July of this year sentiment in the Michigan Survey sustained levels not seen in over two decades. Optimism at such levels is a rarity, even in the best of times.

In the 41 year history of this survey there has only been one other period that scored as highly, that of from March 1998 to August 2002.

Reuters

The rebound from July’s three year low of 89.9 to 95.5 in October has been driven largely by a recovery in the current conditions index. It has climbed 7.9 points from 105.3 in July to 113.2 while the expectations index has gone up by just over half as much, 4.3 points, and 79.9 to 84.2. This differential is what one might anticipate with a buoyant labor market competing with genuine but non-specific fears about the future.

Reuters

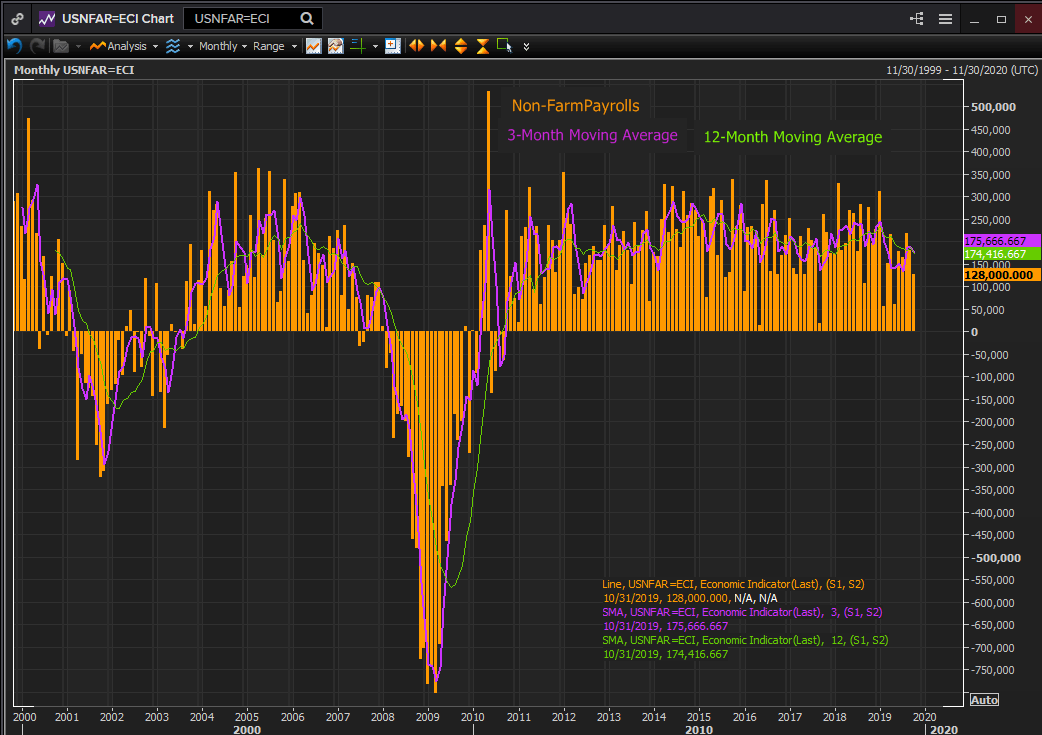

October’s non-farm payrolls reinforced the idea of the present against the somewhat uncertain future.

New employment of 128,000 was far ahead of forecast and the addition of 95,000 to the August and September totals brought the 3-month and 12-month moving averge to 176,000 and 174,000 respectively. Both are more than sufficient to provide work for the 125,000 to 150,000 new entrants to the labor force each month. The surplus of jobs will add to the backlog of unfilled positions accumulated over the past three years, keeping upward pressure on wages.

Reuters

Retail Sales

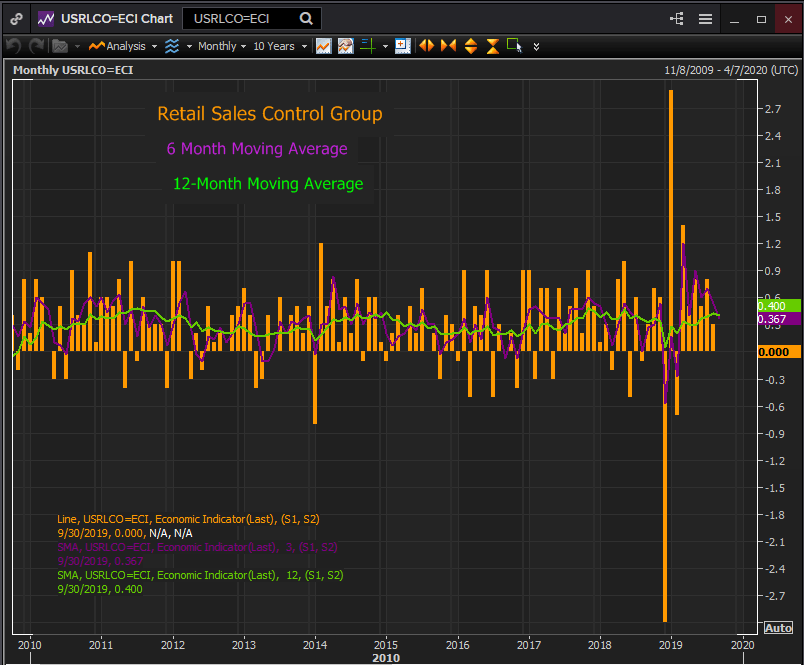

Consumer spending has been the main engine of economic expansion for the past year. Business investment has been moribund as executives wait on the outcome of the US China trade dispute.

The advance reading for the retail sales control group, the government’s GDP consumption component, came in flat in September. But even so the average at six months of 0.367% and 12 months of 0.4% is evidence of a healthy consumer economy.

Reuters

Conclusion

Consumer sentiment remains positive and likely to range higher in the months ahead as the US China trade deal removes a major concern and enables a burst of business investment.

It may be too soon to expect a substantial improvement in the November figures but the direction should be clear.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.