US Initial Jobless Claims Preview: Employment is up, why are claims not down?

- Claims forecast to slip to 1.375 million from 1.427 million.

- Four week moving average has not be below 1 million since March 20.

- Continuing claims expected to be at 18.95 million, down 24% from peak.

- Dollar modestly lower on good US economic data, ebbing virus fears despite the rise in cases.

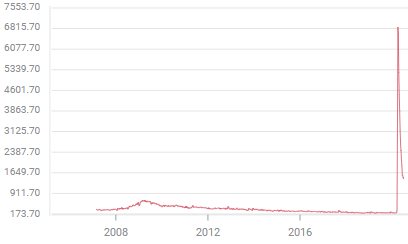

The unexpected recovery in May and June payrolls has not dented the new unemployment claims flowing into the Labor Department where the four-week average has yes to drop below 1.5 million.

Initial claims are predicted to fall to 1.375 million in the week of July 3 from 1.427 million prior. Continuing claims re projected to drop to 18.95 million from 19.29 million. The four-week moving average for initial claim was 1.503 million in the June 26 week.

Initial jobless claims, 4-week moving average

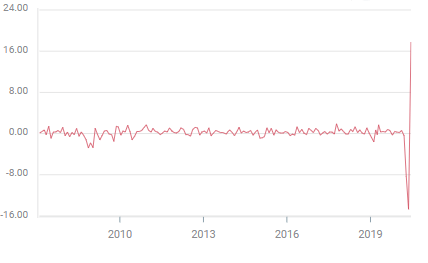

Payroll statistics

Job creation and rehiring has been productive in the last two months with many more people returning to work than had been anticipated. The NFP consensus forecast figure for May was for a loss of 8 million jobs and the June number for a gain of 3 million for a total loss for 5 million jobs over the two months.

The actual figures for May and June were 7.499 million new jobs a swing of 12.499 million, certainly the largest beat in the history of economic forecasts.

Non-farm payrolls rose 4.8 million in June and the May original total of 2.509 million was revised higher by 190,000 to 2.699 million.

The June unemployment rate fell to 11.1% from 13.3% in May, 12.3% had been predicted. Average hourly earnings dropped 1.2% on the month as lower-paid workers were rehired and rose 5% on the year. The labor force participation rate climbed to 61.5% from 60.8% in May. The underemployment rate dropped to 18% from 21.2%.

Consumer confidence

The improving jobs picture has helped to boost consumer attitudes.

The Michigan Survey of Consumer Sentiment has rebounded from its April low. The two month drop from February to April in each of the three indexes, sentiment, current conditions and expectations was the steepest in the 68 year series.

The current conditions index recovered the most--April 74.3 to June 87.1, followed by overall sentiment--April 71.8 to June 78.1--and then expectations--April 70.1 to June 72.3.

Conference Board figures showed a sharper recovery. The consumer confidence index jumped to 98.1 in June from 85.9 in May, easily passing the 91.6 forecast. The present situation index climbed to 86.2 from 68.4 and the expectations index rose to 106.0 from 97.6.

Retail sales and consumption

The gain in consumer attitudes is enabling consumption. Retail sales, durable goods and personal spending numbers for May confirmed the reversal of April’s near paralysis in consumption.

Retail sales plunged 14.7% in April, the largest one month drop on record and then soared 17.7% in May, more than double its 8% forecast. The June retail numbers will be reported by the Census Bureau on July 16.

Retail sales

Durable goods, a set of sales for long-lasting items, fell 18.1% in April and rebounded 15.8% in May, beating the 10.9% prediction. Non-defense capital goods, the business investment proxy, dropped 6.5% in April, then rose 2.5% in May, much more than the 1% estimate.

Personal spending climbed 8.2% in May following the 12.6% April tumble and was the only consumption gauge to miss its forecast at 9%.

Conclusion and the dollar

The disparity between the payroll and claims numbers suggest that that the US economy is moving in two directions at one.

Millions of workers are being rehired at a much faster pace than anticipated as most of the economy liberalizes pandemic restrictions. At the same time businesses continue to fail from the prolonged closures. In many urban areas, especially on the coasts, the commercial traffic needed to sustain restaurants, bars and small shops, remains far below normal levels.

This development indicates that the recovery, however fast, will not easily provide jobs for the unknown number of workers whose employers are permanently closed.

The dollar is also being pulled in two directions. On one side the improving economic data in the US has greatly subdued the pandemic risk-premium. At the same time the rising tide of coronavirus cases, even if not accompanied by increasing fatalities, has stoked fears of the long-bruited second wave of the pandemic.

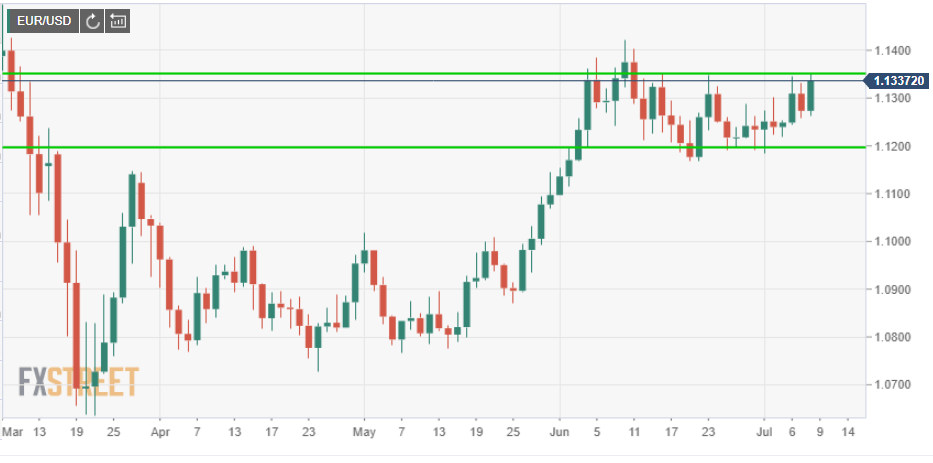

For the past three weeks the major pairs have been trapped in tight ranges as the contest works itself out. The USD/JPY has moved between 106.50 and 108.00 since June 10. The EUR/USD has traded from 1.1200 to 1.1350, the sterling from 1.2350 to 1.2600 and the AUD/USD between 0.6800 and 0.7000.

Unless most of the US resumes lockdowns of the scale and duration of March and April the current flirtation with the risk dollar will eventually disappear.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.