US Consumer Price Index December Preview: The Fed’s die is cast

- Accelerating inflation continues to plague the US economy.

- December CPI expected at 7%, a fresh 40-year high.

- Core CPI forecast at 5.4% up from 4.9%.

- Federal Reserve policy for 2022 has been set by 2021 inflation.

American expectations for inflation have doubled this year and still they cannot catch up with reality.

The US economy is set to deliver another year of soaring prices in 2022 as it closes out a 40-year record in December. Manufacturing production is bedeviled by component and raw material shortages, the global supply chain is creaking under labor and pandemic restrictions and workers are demanding higher wages as firms compete for scarce employees.

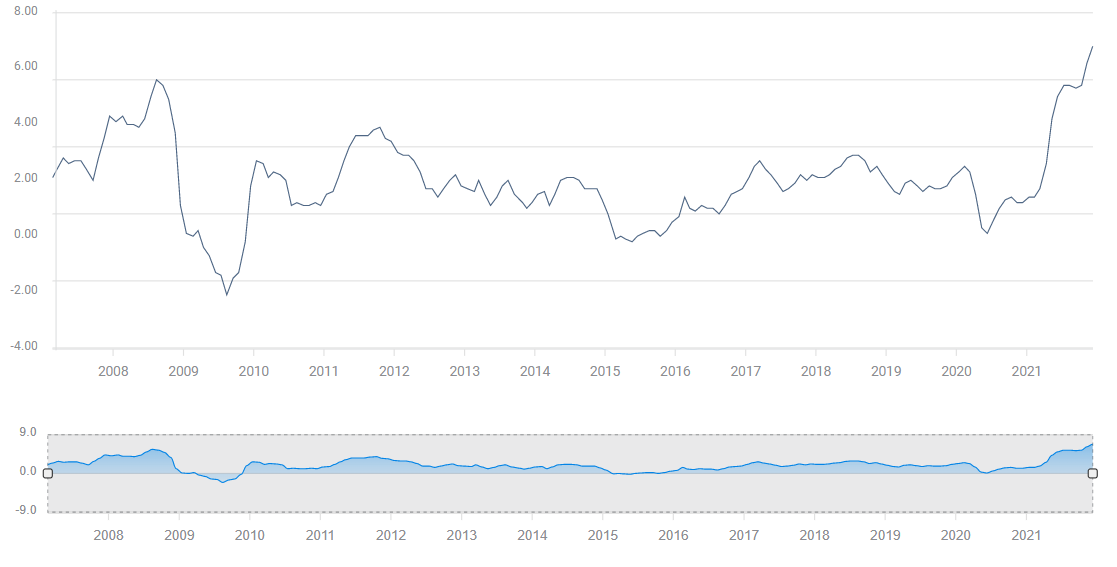

The US Consumer Price Index (CPI) multiplied 4.8 times in eleven months, climbing from 1.4% in January 2021 to 6.8% in November. This is the largest increase in the annual rate over 12 months in history.

CPI

FXStreet

Even in inflation’s heyday from 1973 to 1983, the steepest increase was a doubling of the annual rate from March 1974 at 5.77% to 11.86% in February 1975.

Core inflation, excluding food and energy prices, has vaulted 3.5 times, from 1.4% at the start of last year to 4.9% in November.

Consumer prices are forecast to rise 0.4% in December, after November's 0.8% jump. Yearly CPI is expected to reach 7%. November’s CPI was already the highest in four decades.

Core inflation, which excludes food and energy costs, is projected to be unchanged at 0.5% on the month and to rise to 5.4% for the year. November’s 4.9% increase was the sharpest since May 1991.

If the 7% and 5.4% forecasts for December are correct, overall CPI will have rocketed 500% in 2021 and core will have climbed 385%.

Inflation indicators

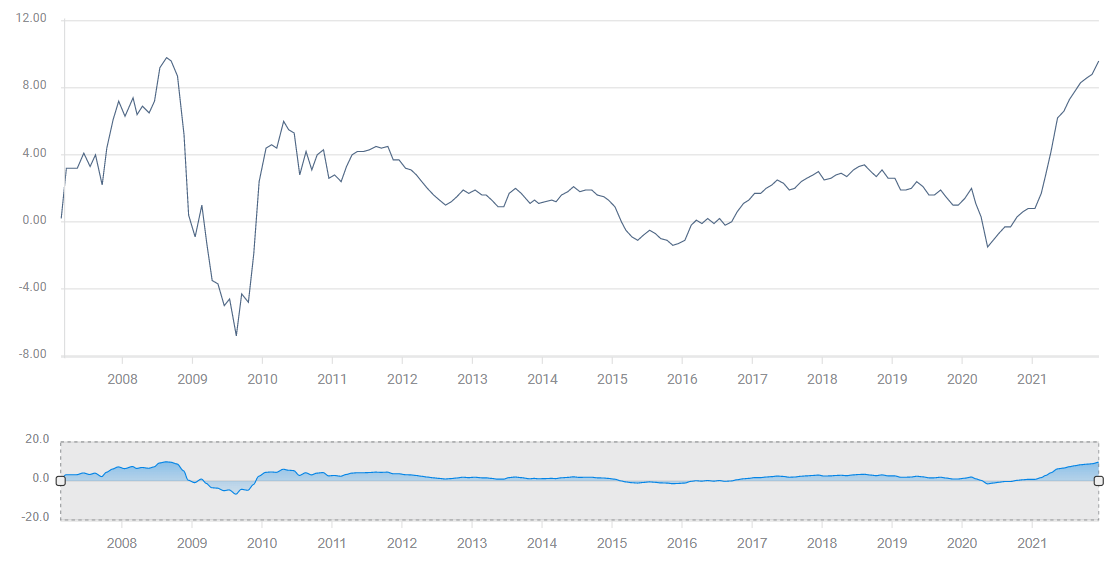

Producer prices are expected to continue their record run in December, rising to the prior high of 9.8% in December from 9.6% in November. The Core Producer Price Index (PPI) is forecast to set its sixth all-time high in a row in December at 8%, up from 7.7% in November.

PPI

FXStreet

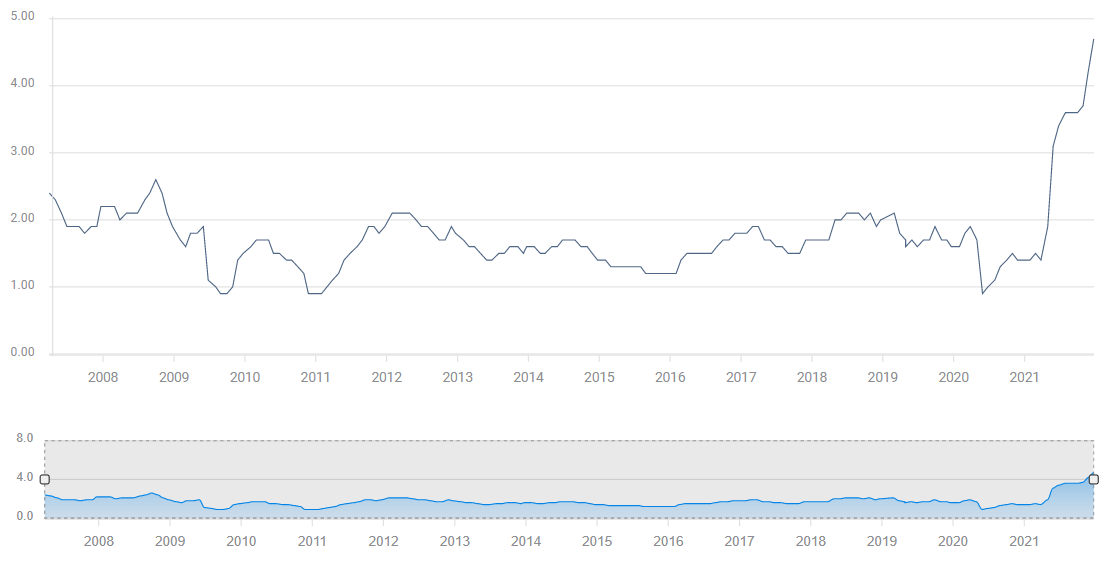

The Fed’s preferred inflation gauge, the Personal Consumption Expenditure Price Index (PCE) exhibits the same surge in consumer prices as the older CPI measure. The headline annual index was 5.7% higher in November, a record, as was the core index at 4.7%. The December figures will be released on January 28.

Core PCE Price Index

FXStreet

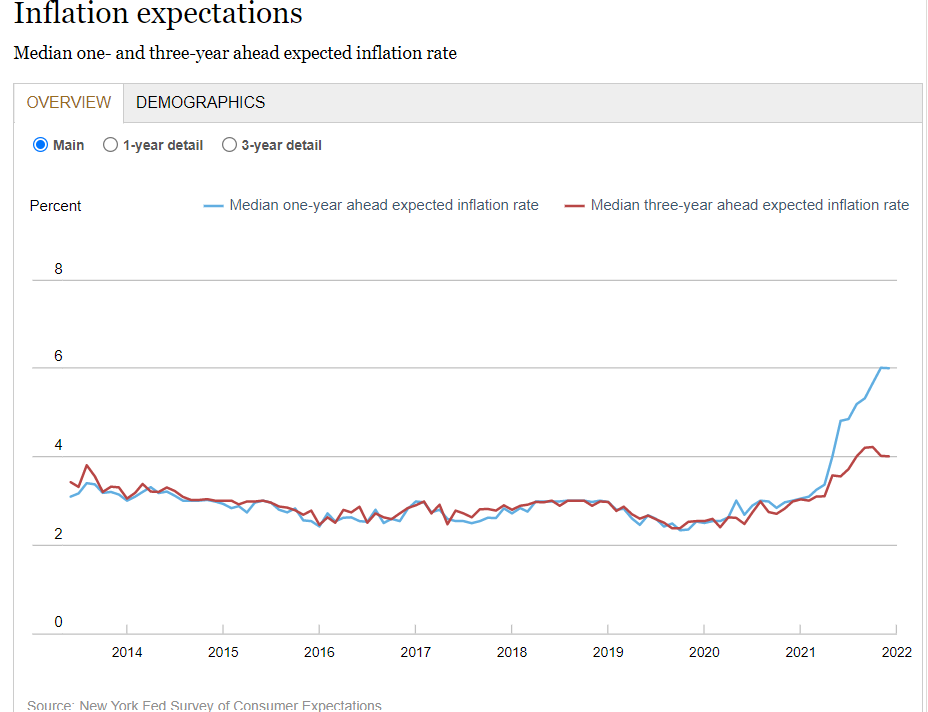

Though the New York’s Fed’s Survey of Consumer Expectations for Inflation one year ahead was unchanged at 6% in December, consumer perception of price movement has rocketed this year. Soaring from 3% in January to 4.8% in June and July, and higher each month to November, it has been above the prior record of 3.4% since May last year.

The three-year estimate dropped to 4% in November and December after reaching its record at 4.2% for September and October.

New York Fed

Purchasing Managers’ Prices Paid Indexes (PMI) in the manufacturing and service sectors, which survey business sentiment regarding inflation, have moderated in the past two months. Expectations in the much larger service sector have dropped to 82.5 in December from their 82.9 record in October. Inflation perceptions have fallen farther on the manufacturing side, where December’s 68.2 index was 23.9 points below the all-time record of 92.1 in June. Even with the December improvement, price pressures as perceived by factory business managers remain well above the median for the past 10 years.

Federal Reserve rate policy

The Fed's dramatic policy reversal at the November and December meetings has moved the bank’s own projections for the fed funds rate at year-end to 0.9% from 0.3%, implying three 0.25% rate increases by December.

Fed funds futures have a solid 76.4% expectation that the first fed funds increase will come at the March 16 Federal Open Market Committee (FOMC) meeting, the same month that the bond purchase programs ends. The odds for at least three 0.25% increases in the fed funds rate by the last meeting of the year on December 14 is 80.5%; the odds for four hikes are 52.5%.

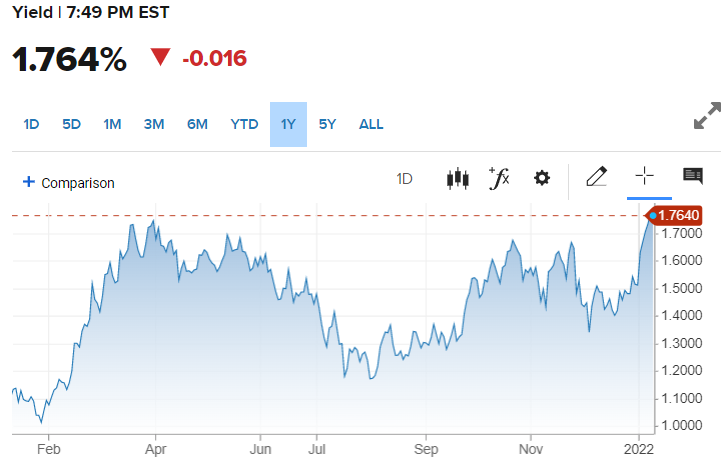

Treasury yields, reflecting the Fed’s new inflation seriousness have moved rapidly higher in the New Year.

The 10-year note has added 25 basis points to 1.764% in the six sessions since closing at 1.512% on December 31. The 30-year return has climbed 18.5 basis points to 2.09%.

US year Treasury yield

CNBC

Despite the increase in Treasury yields this year, they remain well below their pre-pandemic averages.

The sharply higher turn in US inflation that surfaced in the spring has yet to moderate. On that basis Fed policy has been activated through the end of this year. Even if inflation were to pull back in the first half of the year, rate policy is well behind the price curve and can be expected to continue as projected through to December.

Markets

Fed rate policy for 2022 has been determined by the surge in inflation in the second half of 2021. Rate increases will be faster and more certain if US inflation continues to accelerate. Price moderation, which is likely in the second half, will not reduce Fed rate prospects since a gradual decline in inflation will start from a 40-year high. Little short of a recession could instill a change in Fed policy. In the pandemic era that is unfortunately possible, but it is not likely.

Equities

Rising interest rates have brought a minor pull-back to US and global equity averages. The S&P 500 was down 2.7% at the close on Monday from its January 3 high. The Dow was down a more modest 2.0% and the NASDAQ lead US equities in losses, shedding 6.9% from its November 19 top.

S&P 500

CNBC

Equities are balancing the potential drag from higher interest rates against the expected revival in global growth once the pandemic relents and nations adopt health policies that view the virus as endemic, like the flu, rather than the occasion for draconian mitigation or elimination strategies.

Spanish Prime Minister Pedro Sanchez said on Monday that he planned to ask European officials to consider such changes in the union's pandemic approach.

Currencies

Interest rate differentials are back in vogue. The US dollar’s promise varies with central bank policy. For institutions whose rate prospects are static, like the Bank of Japan (BOJ) and the European Central Bank (ECB), the greenback will gain as the year progresses and the Fed acts. For the Bank of Canada (BOC) and the Bank of England (BOE) whose rate structure will follow or lead the Fed, the US dollar will be much less successful.

-637774636061275711.png)

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.