Trump is undoubtedly a dollar-negative

Outlook:

The big economic story yesterday was Q2 unit labor costs and productivity, but the news failed to make the front page. Nonfarm business-sector productivity rose 0.9% annual-ized, better than 01% in Q1 but only 1.2% y/y. The WSJ notes "That was a pickup from last year, when productivity posted its first calendar-year decline since 1982. It also matched the average pace since 2007, but remained well below the post-World War II average of 2.1% annual growth."

This seems like a dull subject and that's why it's buried in the back pages. But it's critical to the outlook. Bottom line, productivity is too slow. The effect on GDP is to keep it at only around 2%. The effect on wages is to restrain hikes to current levels. The effect on inflation is negative.

Depending on what we get in tomorrow's CPI report, the Fed will have a hard time justifying a rate hike this year, let alone in September. The CMR FedWatch Tool has a probability of a hike this year at 42.2% from 50.9% a month ago on July 10. The CME also notes there are 41 days to go before the Sept meeting.

Instead of a rate hike, all we may get is some fresh news on shrinking the Fed's balance sheet, or at least that is what traders are hoping for from NY Fed chief Dudley at a press briefing this morning. The ques-tion is whether shrinking the balance sheet has the same effect as a hike, as some analysts propose.

Well, no.

First of all, the careful and gradual release of assets back into the market will not be on the same scale and at the same pace as the original acquisition of them, and so we can hardly expect a one-for-one ef-fect. The Fed balance sheet rose by $3.5 trillion from 2007 to now, but the divestiture will be on a far lesser scale, probably $1.2-1.8 billion over several years. The FT reported the Fed's own estimate of the effect on the 10-year yield is only 40-60 points. This is about half of the 120 point gain engineered by QE.

Besides, the market is already pricing in the normalization. And that's exactly what the Fed wants—no surprises, no repeat of the taper tantrum. The FT reports "Janet Yellen has suggested that the expecta-tion of balance sheet normalisation has already increased the bond yield in 2017 by 15 basis points, which she says is equivalent to two 25 basis point increases in the fed funds rate."

And not least is the combination of contracting the balance sheet and rate hikes. If markets freak out about the contraction, the NY Fed will throw liquidity at the market and the FOMC will defer hikes. NY Fed chief Dudley is less vocal about his liquidity obsession these days, but don't imagine it's not uppermost in his mind and he will be tracking liquidity hour-by-hour, if not minute-by-minute, once the contraction plan comes out. As we know all too well from history, you can have a well-functioning fi-nancial sector that is brought down by that one thing, a loss of liquidity.

Isn't this all as little too fancy for the average FX trader? After all, these are the folks who seek single-phrase, knee-jerk "information." While most traders are not big readers of deep analysis of things like unit costs and Fed studies on normalization, somehow they still manage to grasp the essentials. We might summarize it by saying "no inflation so no hike but Fed lifting yields anyway, if only a little—pare dollar shorts."

We have another factor potentially offering dollar support—Congress talking behind the scenes about the one tax deal they can get done—the repatriation of the $2.62 billion corporate profits stashed over-seas. The WSJ says US laws "encourage" companies to leave profits overseas, which is bad wording. Technically there is a tax law (Subpart F) that should apply (and used to apply) to overseas profits to prevent precisely this outcome, but evidently the green eyeshade boys have found a way around it.

Congress, of course, would rather give companies an ultra-low rate to repatriate the dough rather than fix the underlying problem of a tax code that should have been taxing the income in the first place. Trump says "It's been out there for years. Nobody ever did anything about it." Another Trump lie. Bush Two did something about it in 2004 and some $312 billion was repatriated—only to be spent on executive bonuses and stock buybacks, not capital investment.

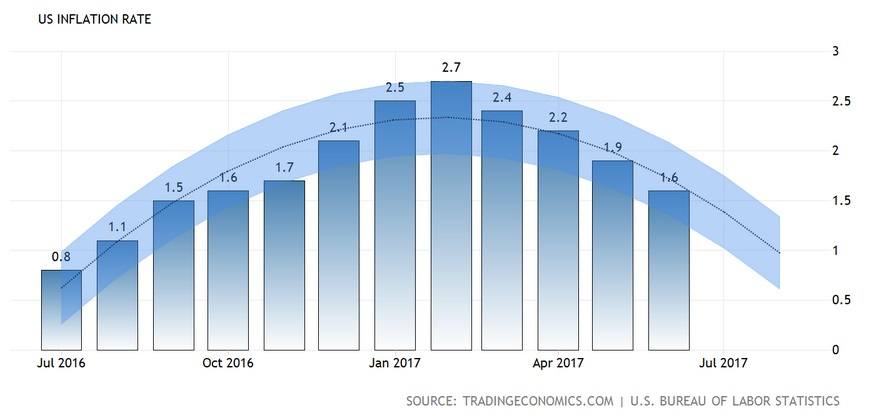

That's the fundamental background. Sorry that it's so dull. The next chapter is pretty dull, too. It's to-morrow's inflation report, likely another dip. Here is the tradingecnomics.com chart, again. The proba-bility of a jump in inflation is virtually zero and the probability of a big disappointment is nearly 100%.

At the start of the week we thought the dollar would retreat sharply on the CPI release. Now we are not so sure. Normally bad news has an exaggerated effect on the dollar. But the N. Korea thing has seem-ingly offset it and that leaves the giant re-positioning (paring dollar shorts) as the lead factor. We are very leery of forecasting that inflation will be bad and therefore the dollar will fall. Everyone already knows the forecast and it's not being heeded as the dollar-negative it should be in the absence of other factors.

We don't really have any more economic factors to consider so that leaves the political risk created out of whole cloth by Mr. Trump. With terrific timing, the NYT ran a story late yesterday headlined "In the Age of Trump, the Dollar No Longer Seems a Sure Thing." The article reads "... those who trade in currencies see tentative signs that the dollar may be losing some status as markets grapple with the un-orthodox actions of the man leading the nation printing the money. Donald J. Trump's presidency has been so full of departures from the norms of international relations that uncertainty has seeped into the calculation of America's plans. That has subjected the dollar to additional skepticism, enhancing the fundamental factors pulling it down, from worries about the strength of the American economy to im-proved fortunes in Europe and Asia.

"The dollar has in some sense become an international medium of expression about the American polit-ical environment. Its value offers a gauge of sentiment for Mr. Trump's prospects in achieving his eco-nomic goals, as well as worries about his potentially impulsive declarations." Initial favorable expecta-tions for the dollar have been dashed by tweeting of wild rants and general turbulence. Mostly tweets.

Meanwhile, Europe has cleaned up its act politically and stopped discounting growth. The dollar is weaker even against not-so-hot currencies like the yen and pound. "The fate of the dollar is now subject to the influences of a presidential administration that has given markets an expectation for the unex-pected. As traders seek to divine the risks of geopolitical hot spots, this appears to be weighing on the American currency. ‘There is some erosion in the relative stability of the United States in light of this administration's inconsistency on global affairs,' said Mr. Posen of the Peterson Institute. ‘The U.S. is at relatively more risk than we thought in the past.'"

Gee, d'you think? It's not so much the content of the NYT story that counts, but rather that the NYT found yet another thing to deride the president with, not that it has to look very far. And it's not even the top story in the business section—that honor goes to the problem if low-wage immigrants, the prob-lem being not having them to do the back-breaking ag work.

Here's our take on the N. Korea story. Those who think Trump is a blot on the US copybook will not like it. He is a blot but blustery bullying worked (this time). By late yesterday, anxiety over the face-off between N. Korean and the US was waning. For one thing, it looked like N. Korea was retreating from its most bellicose stance. Threatening to annihilate Guam is not the same thing as menacing Los Ange-les.

Insiders disclosed that Trump's "fire and fury" outburst was not planned and not a "strategy" based on analysis and briefings, but major press outlets scrambled to find an excuse in Nixon's "mad man" theo-ry, which consists chiefly of keeping the other guy worried you might be crazy. Trump will have no problem putting that one over. And he just can't help lying. He said he had upgraded and modernized the military, including nuclear capability, when in fact that was a process ordered by Obama.

Cable TV played and re-played an interview with Trump from the late 90's in which he said it would be better to bomb N. Korea now than to drag heels until they actually got nuclear capability. Now they have it and Trump is still inclined to think asserting US military power is the right way to tame the un-ruly. In the vast swathe of military history, both the Dear Leader and Trump are actually behaving ra-tionally. In fact, Trump might be crazier than Kim Jun Un.

Here's the strategy as it unfolds: China and Russia come to believe that Trump is indeed crazier than Kim Jun UN and force N. Korea to the table, with a target of a freeze or a cap. That means Trump out-bursts are good for the US position insofar as they bring other parties in to prevent Trump from pushing the red button. How strange is that? And while Trump is undoubtedly a dollar-negative, the madman theory can work in the US favor. If it works, Trump will later claim this is what he had in mind all along. It will be another lie, but he might get away with it.

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 109.85 | SHORT USD | 07/19/17 | WEAK | 111.96 | 1.88% |

| GBP/USD | 1.2992 | LONG GBP | 06/28/17 | WEAK | 1.2701 | 2.29% |

| EUR/USD | 1.1708 | LONG EURO | 06/28/17 | WEAK | 1.1218 | 4.37% |

| EUR/JPY | 128.62 | LONG EURO | 06/27/17 | WEAK | 125.73 | 2.30% |

| EUR/GBP | 0.9011 | LONG EURO | 04/25/17 | STRONG | 0.8490 | 6.14% |

| USD/CHF | 0.9655 | SHORT USD | 08/10/17 | NEW*WEAK | 0.9655 | 0.00% |

| USD/CAD | 1.2730 | SHORT USD | 05/17/17 | STRONG | 1.3621 | 6.54% |

| NZD/USD | 0.7262 | LONG NZD | 05/30/17 | STRONG | 0.7062 | 2.83% |

| AUD/USD | 0.7875 | LONG AUD | 06/08/17 | WEAK | 0.7548 | 4.33% |

| AUD/JPY | 86.50 | SHORT AUD | 08/07/17 | STRONG | 87.66 | 1.32% |

| USD/MXN | 17.9532 | LONG USD | 08/07/17 | WEAK | 17.8507 | 0.57% |

| USD/BRL | 3.1556 | SHORT USD | 07/17/17 | WEAK | 3.1794 | 0.75% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat