The market has built in an acceptable number to the dollar

Outlook:

What's built in and what is not? Chatter about a low Australian inflation number had been constant for weeks. When something is so well signaled so long in advance, we usually get a pop in the other direction. We had the same effect from the Bank of Canada's dovishness. The one place we got the expected market response was the euro. A lousy IFO shoved it down, but it bounced back in short order (only to fall again for reasons nobody can point to except maybe fatigue).

What does this mean for tomorrow's GDP? The market has built in an acceptable number to the dollar. What is "acceptable"? presumably more than the NY Fed at 1.37% but probably less than the Atlanta Fed at 2.8%. The WSJ is now showing 2.5%.

The first quarter is over but this time analysts are not dismissing the data as too-old or outdated. The Fed meets next week (April 29-May 1) and despite having plenty of other data points to consider, GDP is a summary number. The Fed can't admit talking about a cut if the number is on the high side and can't avoid talking about it if the number is extra-low. (Heaven only knows what the Fed is going to do with payrolls only two days later (Friday, May 3).)

Reminder: Q1 GDP forecasts:

Atlanta Fed: 2.8%

IMF: 2.3%

St. Louis Fed: 1.89%

NY Fed: 1.37%

WSJ: 2.5%

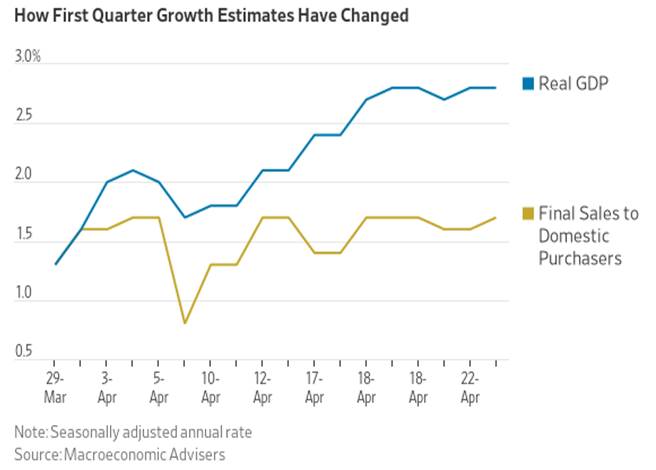

The WSJ Fed-watcher Ip notes that Macroeconomic Advisors just revised its forecast from 1.3% to 2.8% (the NY Fed to the Atlanta Fed, so to speak) but also warns the gains arise from "lower imports and higher inventories, neither a sign of vigorous spending at home. Consumer spending has been revised up while business investment has been revised down. So the firm thinks final sales to domestic buyers—a popular measure of underlying demand—grew just 1.7%, up only slightly from its early-April estimate." The headline numbers will "mask" subdues demand and that is not a healthy thing.

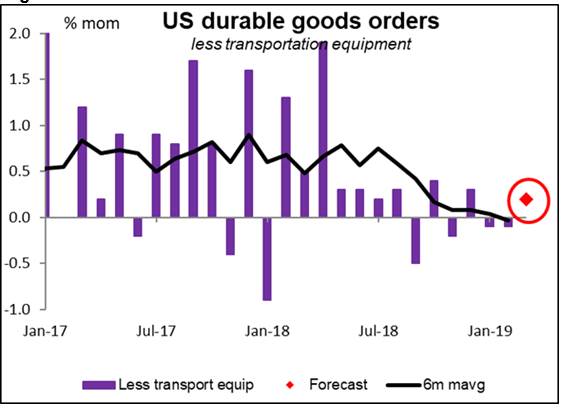

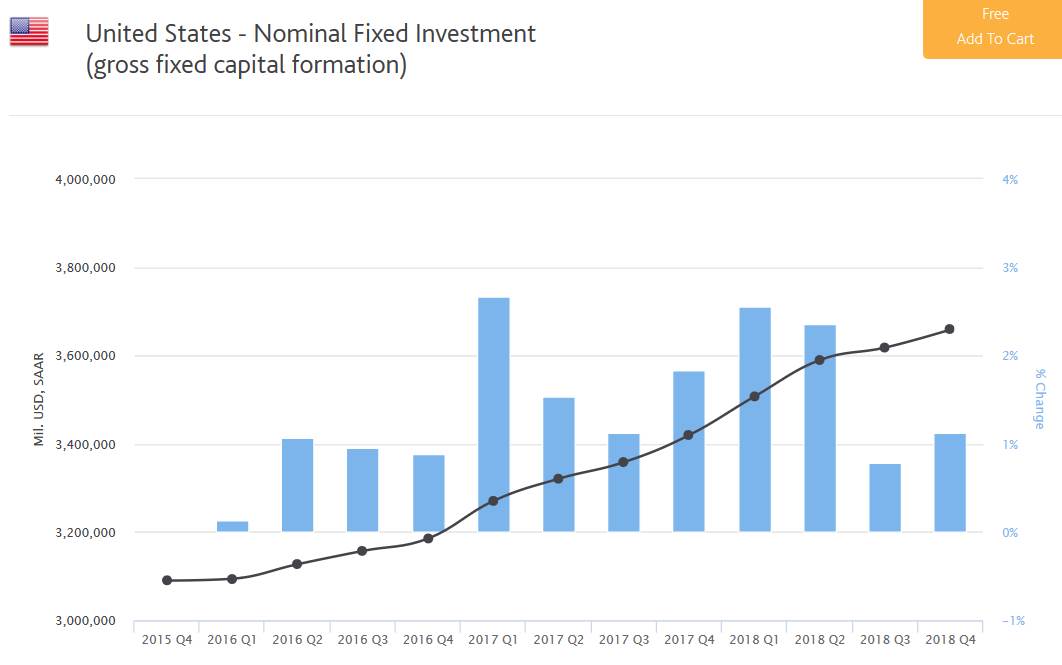

Another warning of sorrow to come could arrive in the form of durables less transportation. Given Boeing's woes, this version of durables is more important than ever. Gittler at ACLS has one of his terrific charts showing a year-long drop in this version of durables, a proxy for investment. The actual number, gross fixed capital investment, is doing fine, thank you—chart from Moody's—but a lousy GDP number should inspire talk of reduced investment expectations. We could use something like Japan's Tankan right around now.

On the surface, the US is the best performing economy among the majors today. It would seem that despite these warnings signs above, the first half of the year will not disclose cracks and fissures that would undermine the economy. How can the Fed possibly be considering a rate cut, or talking about one? Well, perhaps because the global economy is not so hot and "everybody's doing it."

It started with New Zealand talking about potential cut. We don't follow the Swedish Riksbank, but today it delivered a shocker—a QE bond-buying program to begin in July. The benchmark repo rate is kept at the same -0.25% and will remain there for longer than the Riksbank had thought only in February. The krona fell about 1% against the euro to the lowest since 2003, according to the FT.

Elsewhere, emerging markets are in the soup as Turkey persists in mismanaging. The FT reports the lira is down 7% year-to-date and fell some more today on the central bank removing a phrase referring to future tightening. Argentina is facing an election and investors don't like the outlook. "Investors stampeded out of Argentine assets on Wednesday amid fears that a deep recession and record-breaking inflation will pave the way for a return to populism after presidential elections in October. Although there was a sell-off around emerging markets as the US dollar strengthened, Argentine debt, stocks and the currency suffered outsized falls as former leftist president Cristina Fernández de Kirchner continued to grow stronger in the polls. The spread on interest rates between US Treasuries and Argentine sovereign debt widened by nearly 1 percentage point to 9.56 per cent on Wednesday, the highest level since February 2014. Meanwhile, the peso tumbled by about 3.5 per cent."

You'd think that there might be discretion applied to better-managed EM currencies, like Mexico, but no. It's plain old-fashioned EM contagion. It's hard to say how much influence the EM flight has on the dollar but if you are looking for a haven, the dollar is the obvious choice.

So, is it a race to the bottom? A central bank signals cuts and its currency falls. In practice, a Fed cut might not have the standard effect because of the dollar's reserve currency status, yield advantage (if slipping) and the variety/range of investment opportunities. But you can't count on it. A lousy GDP tomorrow might well get over-interpreted to mean Fed cut. That would drive yields lower and stock market indices up. We could get that effect even if GDP is okay, now that so many are baking a cut into the cake regardless of evidence. We have low inflation and low inflation expectations, and that may suffice. We hesitate to predict a falling dollar on a low GDP number.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a free trial, please write to [email protected] and you will be added to the mailing list..

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat