Disconnection between Fed speakers and bond markets

Outlook:

Weare a little surprised that the mar ket has retur ned to its pre-hike skepticism about the Fed' hawkish intent. Yesterday two Fed regional presidents said four hikes this year are possible, but the bond market persists in doubting three and rejects four altogether. Market News reports Chicago Fed Pres Evans said "There is some chance that we could do four" under the right conditions. Philly Fed Harker said he "wouldn't rule out anything at this point," even more than three rate hikes if the economy strengthens enough.

But "The market well knows that for such a thing to materialize, either inflation would need to rise more markedly or hard U.S. data sets must be much stronger." WSJ bond market analyst Zeng concurs. Just look at the 10-year yield, down to 2.472% yesterday [and 2.496% this morning] from 2.6% just ahead of the Fed. This is a curious outcome and its persistence can be traced to inflation expectations out of sync with Fed comments. The University of Michigan inflation expectations last Friday is not on the rise. The 10-year breakeven rate (Treasuries minus TIPS) was 2.01% yesterday—almost the same as the 5-year version. If inflation is really coming, the 10-year breakeven should be higher than the 5-year.

Does this mean Minneapolis Fed Kashkari is right? He dissented from the hike decision on the grounds inflation has a long way to go to justify tightening. And yet the Fed's preferred measure, the PCE price index, is up 1.9% y/y and core PCE is up 1.7%. Maybe we are so unaccustomed to inflation that we just don't believe our own eyes.

We get another boatload of Fed speakers today, including Boston Pres Rosengren, New York Pres Dudley and Kansas City Pres George. Of these, Dudley is among the top Feds with Yellen and Fischer, and is the one that has the biggest chance of impressing the bond gang. He has already spoken in London and we are not seeing any fireworks.

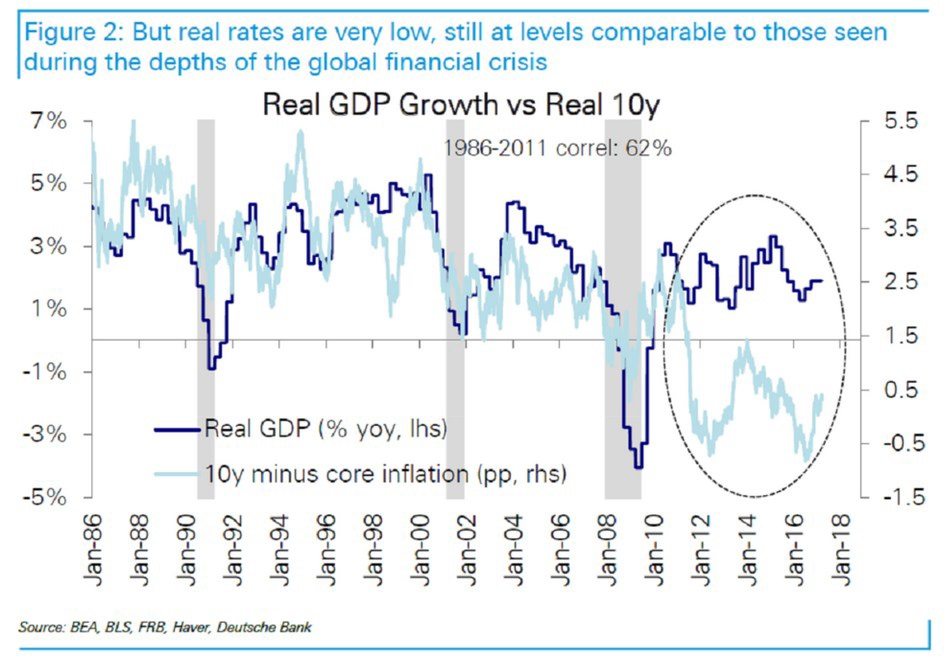

We have a gigantic disconnect between some variables that should be moving in lockstep. If US inflation is at or nearly at the 2% Fed target, and Feds are out all over the place defending the three-hike scenario, why does the market not believe it? Bloomberg has a story on Deutsche Bank analysis who say the disconnect is the Fed's fault. The Fed has driven mispricing of real yields and the divergence of yields from real growth is not sustainable. See the chart.

Equity players see a reflation trade, but that's is direct opposition to what the bond gang sees. The real 5-year yield is negative. "Real rates, which have generally moved in lockstep with real gross domestic product, are some two percentage points below what's implied by the momentum of the U.S. economy, an unsustainable divergence, according to Deutsche Bank. ‘We see real rates as extremely misvalued if not in a bubble.' Inflation-adjusted yields can't defy economic gravity for much longer, they argue, setting the stage for a correction that may imperil risk appetite in bond markets over the summer."

The trigger for a shock adjustment will be rising wages, says Deutsche Bank. Bloomberg opines "Judging by benign market pricing, that view remains an outlier." Others, including Goldman and BoA, are worried about an uptick in real rates and advising clients to steer clear of long-dated paper. One scenario is higher real rates by June when core inflation really does pick up and the "dollar shock" fades, inspiring the Fed to get truly hawkish instead of the "dovish hike" we just had.

We like to invent scenarios as much as the next guy, but this sounds like wishful thinking. It also completely ignores the oil price and its long tentacles. If we continue to get oil prices under $50-55, US production will continue to offer supply that offsets whatever cuts OPEC manages to get. We are far more likely to get an inflation effect downward from oil than an upward effect from wages—not now that unions are dead and the US worker has no wage leverage, skilled labor shortage notwithstanding. Companies have become accustomed to underpaying labor. Inflation will have to get much higher before wages catch up.

Besides, analysts are starting to question the so-called reflation trade. It relies on a boost in growth and inflation from government policies like deregulation, tax cuts and stimulus spending. We are not getting any of those things until later in the year, if then. Reflation traders jumped the gun. Well, overshooting is rampant in all markets. For once the dollar may be the leader and not the follower.

Politics: Yester day was wall-to-wall testimony from the FBI director and NSA chief to a Congressional committee. To news junkies, it was like a candy store for a kid. Some of the Dems asked really smart questions (put these people on the finance committee, please) and some of the Plubs asked mostly those directed more to the crime of leaking than to the content of the investigations.

Our worst fears were realized. First, Trump lied about Obama or anyone else in government (or the UK) surveilling him. Nobody has any evidence and Trump refuses to admit that evidence does not exist— he made it up. Secondly, the FBI is indeed investigating whether there was cooperation or collusion by any Trumpies with the Russians hacking and otherwise disrupting the election. At least four persons in the Trump camp had direct relationships with Russia; one of them knew about the DNC hack ahead of time and another may have gotten a huge payoff (19% of Rosneft) for committing to cutting sanctions and downplaying the Russian invasion of Ukraine. All four are now gone but boy, does it smell fishy.

Comey is slippery as an eel. He has to be, since he is not allowed to disclose the existence of ongoing investigations, let alone any information about them. Three things: Comey did not disclose the FBI investigation into the Trump campaign "links or cooperation" with Russia in July when it started, but he felt compelled to disclose the renewed investigation into Clinton's emails in October, six days before the election. Many people, including Bill Clinton, think the FBI re-opening the investigation cost Clinton the election. This remains a blot on Comey's otherwise strong reputation. Second, Comey is impressive and has massive self-control. You would not want to be interrogated by him. His refutation of the Trump tweets about being surveilled is named a "rebuke" in the press. Presidential historian Brinkley says such a rebuke is unprecedented in American history. Imagine J. Edgar Hoover saying a sitting president is a liar! Brinkley also said there is "a smell of treason in the air."

Third, Trump can fire the FBI director only for cause. Otherwise, Comey's term lasts another six years and he may be a thorn in the side the whole while. The problem, of course, is that Comey can talk only when forced to by a Congressional committee.

It's not hard to imagine blow-ups. Trump can try to fire Comey. The FBI investigation can drag on for months—or get done just in time for the 2018 mid-term elections. Something else can happen that brings impeachment proceedings and Comey gets dragged into that. Or Trump can tweet some more to try to distract attention. As some wag said on TV, Trump needs an intervention. The mind boggles.

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 112.51 | SHORT USD | 03/21/17 | NEW*WEAK | 112.51 | 0.00% |

| GBP/USD | 1.2462 | SHORT GBP | 03/02/17 | WEAK | 1.2278 | -1.50% |

| EUR/USD | 1.0792 | LONG EURO | 03/16/17 | WEAK | 1.0711 | 0.76% |

| EUR/JPY | 121.42 | LONG EURO | 03/13/17 | STRONG | 122.20 | -0.64% |

| EUR/GBP | 0.8660 | LONG EURO | 03/02/17 | STRONG | 0.8575 | 0.99% |

| USD/CHF | 0.9963 | SHORT USD | 03/16/17 | WEAK | 0.9995 | 0.32% |

| USD/CAD | 1.3322 | LONG USD | 02/22/17 | WEAK | 1.3174 | 1.12% |

| NZD/USD | 0.7057 | SHORT NZD | 02/10/17 | STRONG | 0.7185 | 1.78% |

| AUD/USD | 0.7734 | LONG AUD | 03/16/17 | STRONG | 0.7686 | 0.62% |

| AUD/JPY | 87.01 | LONG AUD | 02/09/17 | WEAK | 85.92 | 1.27% |

| USD/MXN | 18.9413 | SHORT USD | 01/31/17 | WEAK | 20.8108 | 8.98% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat