RBA provides balanced statement

Market Brief

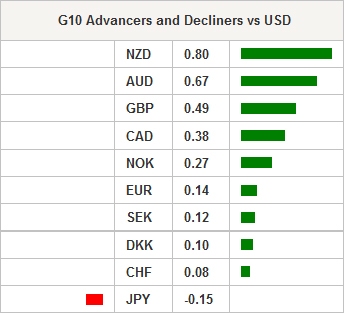

Risk appetite came back marginally in the Asian session. Yet overall volumes and directional momentum was lacking. In FX USD was slightly weaker against the G10 and EM with the AUD and NZD leading currencies higher. Most of Asia was higher with the Shanghai composite 0.5%, Hang Seng 0.9% and ASX up 0.4%. US treasuries were slightly lower with the US 10 year yields down to 1.77% while 2 years closed at 0.817%. No much change but allowed for FX, which is now highly correlated to put USD on the back footing. USDJPY was range bound in low volume trading between 103.70 and 103.95. Japanese Finance Minister Aso reiterated the corporate BoJ a line stating the central banks was watching FX moves carefully. Indicating that excessive volatility could damage the economy. In New Zealand 3Q CPI rose 0.2% from 0.4% in 2Q. While Non-resident holding for government debt fell to 61.9% in September from 63.5% in August. The CPI read did little to shift the markets expectation for a RBNZ rate cut in November. NZDUSD rallied to 0.7190 from 0.7128 with bullish traders targeting 0.7202 Oct high.

In Australia, RBA Lowe provide balanced comments yet the threshold of another interest rate cut feels high. Lowe indicated that the benefit from ultra loose monetary policy globally was losing benefits, while the RBA current poly mix was working well and was comfortable with the level of AUD. Lowe suggested that the 3Q CPI read out next week will be important for rate setting and that the RBA nee to protected inflation expectations from falling to low. AUDUSD was bale to rally to 0.7676 from 0.7624 on the comments.

European data indicated that inflation accelerated in September. However, the jump was mainly due to fuel prices with core read basically unchanged. It unlikely that this higher headlines read will go far is persuading the ECB that the inflation outlook remains weak. In our view there is a low probability that the ECB will make any announcement of changes to the current monetary policy strategy at this weeks meeting. EURUSD was range bound dipping to 1.0995 then firming back to 1.1060. Support is located at 1.0950 but unlikely to be challenged ahead of the ECB meeting and press conference.

Today’s focus is likely on UK and US inflation reads.

| Global Indexes | Current Level | % Change |

|---|---|---|

| Nikkei 225 Index | 16963.61 | 0.37 |

| Hang Seng Index | 23343.1 | 1.32 |

| FTSE futures | 6946.5 | 0.63 |

| DAX futures | 10550 | 0.59 |

| SMI Futures | 8020 | 0.25 |

| CAC futures | 4476.5 | 0.59 |

| S&P future | 2131.2 | 0.38 |

| Global Indexes | Current Level | % Change |

|---|---|---|

| Gold | 1261.74 | 0.47 |

| Silver | 17.67 | 1.14 |

| VIX | 16.21 | 0.55 |

| Crude wti | 50.3 | 0.72 |

| USD Index | 97.74 | -0.15 |

| Today's Calendar | Estimates | Previous | Country/GMT |

|---|---|---|---|

| BZ Aug Retail Sales MoM | -0,50% | -0,30% | BRL/11:00 |

| BZ Aug Retail Sales YoY | -5,00% | -5,30% | BRL/11:00 |

| BZ Aug Retail Sales Broad MoM | -1,00% | -0,50% | BRL/11:00 |

| BZ Aug Retail Sales Broad YoY | -6,10% | -10,20% | BRL/11:00 |

| CA Aug Manufacturing Sales MoM | 0,30% | 0,10% | CAD/12:30 |

| US Sep CPI MoM | 0,30% | 0,20% | USD/12:30 |

| US Sep CPI Ex Food and Energy MoM | 0,20% | 0,30% | USD/12:30 |

| US Sep CPI YoY | 1,50% | 1,10% | USD/12:30 |

| US Sep CPI Ex Food and Energy YoY | 2,30% | 2,30% | USD/12:30 |

| US Sep CPI Index NSA | 241,498 | 240,853 | USD/12:30 |

| US Sep CPI Core Index SA | 248,722 | 248,338 | USD/12:30 |

| US Sep Real Avg Weekly Earnings YoY | - | 0,40% | USD/12:30 |

| US Oct NAHB Housing Market Index | 63 | 65 | USD/14:00 |

| MX Oct.14 International Reserves Weekly | - | $175354m | MXN/14:00 |

| US Aug Total Net TIC Flows | - | $140.6b | USD/20:00 |

| US Aug Net Long-term TIC Flows | - | $103.9b | USD/20:00 |

Currency Tech

EURUSD

R 2: 1.1616

R 1: 1.1428

CURRENT: 1.1013

S 1: 1.1046

S 2: 1.0913

GBPUSD

R 2: 1.2857

R 1: 1.2477

CURRENT: 1.2229

S 1: 1.2090

S 2: 1.1841

USDJPY

R 2: 111.45

R 1: 107.49

CURRENT: 103.91

S 1: 102.80

S 2: 100.09

USDCHF

R 2: 1.0093

R 1: 0.9950

CURRENT: 0.9881

S 1: 0.9632

S 2: 0.9522

- S: Strong, M: Minor, T: Trendline, K: Keylevel, P: Pivot

Author

Peter A Rosenstreich

Swissquote Bank Ltd

Peter Rosenstreich is Swissquote Bank’s Head of Market Strategy and manages the global strategy desk; he has held various positions in several banking institutions in the United States, Europe & Asia.