Federal Reserve Monetary Policy: Transparency and the fallacy of forward guidance

- Federal Reserve expected to hike 75 basis points to 3.25%.

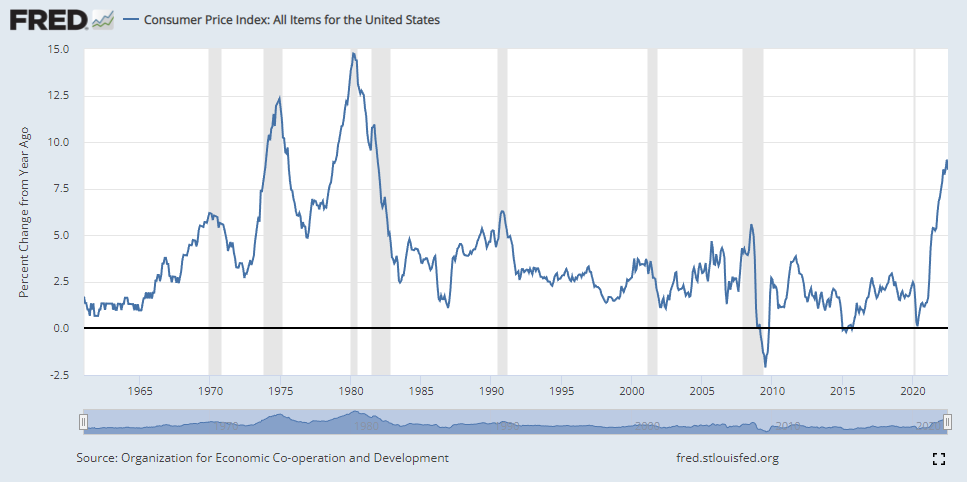

- US inflation was unsubdued in August at 8.3% and 6.3% for core.

- Markets fear an aggressive Fed will prompt a serious recession in the US.

“If I seem unduly clear to you, you must have misunderstood what I said,” Alan Greenspan, Federal Reserve Chairman–Speaking to a Senate Committee on September 22, 1987, quoted by the Federal Reserve Bank of San Francisco.

The Federal Reserve policies of transparency and forward guidance on interest rates, products of the Ben Bernanke era, have become a burden and mistake. Forward guidance forces the central bank into a dangerous certainty about the economic future and transparency makes that judgment public.

Alan Greenspan’s famous quote at first seems snarky and a bit arrogant. More of the notion that you the listener don't understand, than what it actually was, a witty admission that the Fed often doesn't have a clear idea of the economic direction or the correct policy.

Last year, as American inflation began its run to a four decade high in 15 months, Fed spokesman repeatedly claimed that the price surge was transitory. Consumer inflation was, they said, the result of the dislocations in supply and labor from the lockdowns ordered by many US states. In the Fed’s view, inflation would ease once the economy returned to normal operation.

That judgment was widely shared by analysts and economists, though with some notable exceptions, including former Treasury Secretary Lawrence Summers.

By often and assuredly proclaiming that that inflation was temporary, the Fed succeeded in looking foolish and inept. How could such a novel economic situation warrant such certainty?

More importantly, such strident rhetoric, in the face of exceptional and poorly understood phenomena, trapped the bank’s policy choices.

If the main problem was to restore the economy before the lockdowns then zero rates and massive monetary pump-priming were the standard solution. The fed funds rate was duly held at zero to 0.25% for 21 months. Bond purchases pushed Treasury and commercial rates to record lows and more than doubled the Fed’s balance sheet to almost $9 trillion.

But the prescription was wrong. The economy had largely recovered on its own by the end of the second quarter of 2021. In June, the three month average for Nonfarm Payrolls was 422,000, first half growth was 6.5% and inflation had almost quadrupled from 1.4% in January to 5.4% at the half year.

Lockdown costs

Lockdowns accelerated changes in attitudes that had been building for two decades, exacerbated by the lingering paranoia over the pandemic. People did not return to work as expected by the Fed. The participation rate loitered almost two percentage points below the 63.4% level of February 2020 for the better part of two years.

Supply chain disruptions and shortages proved nearly permanent, made worse by the global manufacturing dependence on China and the rolling closures of vast sections of the country as the Beijing rulers tried to justify their zero Covid policy.

For labor, supply and goods shortages, low interest rates and monetary profligacy were exactly the wrong solution.

Yet the Fed persisted in its transitory rhetoric for five more months after last June, until Federal Reserve Chair Jerome Powell said, somewhat ruefully on November 30, “I think it’s — it’s probably a good time to retire that word and try to explain more clearly what we mean.”

Even with that admission the first fed funds rate hike did not come for another five months in April 2022, and then just a quarter point. The bond buying program had ended the month before but by then the Consumer Price Index had soared to 8.5%, its highest since January 1982.

Fed funds

We will never know to what degree the Fed’s damaging delay in changing policy was due to the governors’ desire to appear consistent and credible.

What is patent is that had the Fed been more circumspect in its analysis of the economic effect of the covid lockdowns and less confident in its policy pronouncement, consistency would not have been a topic at all. If the Fed had cloaked its natural and understandable uncertainty about the economic impact and recovery in modest obscurity and a little cryptic commentary, recognizing inflation would not have been such a wrench and the switch to a tightening policy could have been accomplished with far less drama.

Were the Fed governors more cautious in their analysis and forecasts, policy could adapted faster to changed circumstances.

Where did the Fed governors get their economic confidence?

The Federal Reserve and central banks worldwide have claimed responsibility for the long decline in inflation from the early 1980s to its re-emergence last year. Crediting astute and tempered monetary policy focused on a specific inflation target, sometimes stated and sometimes not, and the effective management of expectations with policy transparency and forward guidance for rates, central bankers around the globe convinced themselves and most market participants that inflation was a problem solved.

The eruption of global prices last year, a classic case of supply restrictions colliding with rampant money creation, was such an analytical shock that the Fed continued to claim that the price surges would be temporary, long after it was plain they were here to stay.

In taking credit for the defeat of inflation that had been the chief economic problem of the prior three decades, central bank policy makers made a cardinal, but quite human error. They mistook the initial success, especially in the United ‘States under Paul Volcker, for the permanent decline in price pressures and pricing power brought on by the globalization of almost all industrial and consumer manufacturing processes.

Central bank policy piggy-backed on this evolution of the global economy which drove manufacturing to its lowest cost environment. The number of American and European manufacturing jobs that moved to Asian and other low wage countries, numbered in the many millions. That development, the globalization of manufacturing, is the real source of the long decline in worldwide inflation rates.

How do we know this was the source? As soon as the Covid lockdowns disrupted global supply chains, inflation returned, abetted by the oblivious money printing by many central banks, most notably the US Federal Reserve.

Which brings us to our and the Fed’s current predicament.

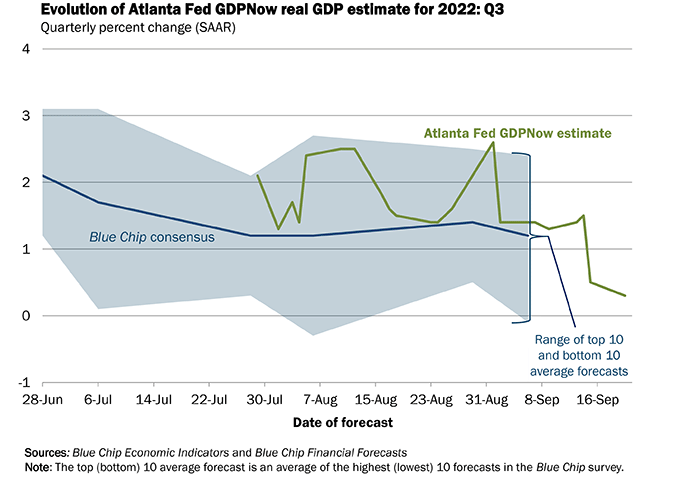

The US economy contracted 1.6% in the first quarter and 0.6% in the second, satisfying the traditional definition of recession. The Atlanta Fed’s GDPNow estimate for the third quarter which ends in little more than a week is 0.3%, the lowest of its two-month series.

What if the current recession continues into the third and fourth quarters? Will the Fed hike rates to 4% and beyond knowing that each increase hightenens the chance of a serious recession?

Treasury yields are already their highest in more than a decade with the 10-year over 3.5% since Monday for the first time since early 2010.

Forward guidance redux

What do you do when you are transparent and wrong?

Forward guidance implies the ability to predict the economic future. Until recently it was too obvious to point out that in order for forward guidance to have any value, it had to be right most of the time on the direction of inflation and the economy.

Why were financial journalists willing to accept the Fed’s recent opinion on inflation when they knew, or should have known, that its record of price prediction has been dismal for more than a decade? After the financial crisis, quantitative easing failed spectacularly to raise inflation to the Fed’s 2% target despite the Fed’s confident and incessant predictions.

If there is one thing that the lockdowns have made clear, the Fed’s understanding of inflation is sorely lacking.

So back to square one.

What is the policy prescription for runaway inflation? The answer is not higher interest rates. The answer is recession. Only a recession can reduce demand sufficiently to make many goods and services surplus. Then and only then do prices decline.

The US economy is already in a mild recession. The Fed has hiked the base rate 225 points to a 2.50% upper target. Adding another 0.75% on Wednesday will bring the fed funds rate to 3.25%. The 2-10 Treasury spread was inverted 41 points at Tuesday’s close.

Does the Fed expect a recession this year? There will be a new set of economic predictions at Wednesday's meeting conclusion. In June the expectation for GDP in 2022 was 1.7% and that was before the second quarter GDP arrived at -0.6%.

Will the Fed keep raising rates until it sees a substantial improvement in inflation? One certainly hopes not, since by that time the US could be mired in a far more serious slowdown.

The Fed may have already done enough to induce a recession. Because it insists on transparency and has tied forward guidance to inflation, the governors will be reluctant to stop hiking until inflation begins to respond. This is why the markets had such a dire response to August core CPI at 6.3%.

Were the Fed less obsessed with letting markets know the policy future, the governors could put the brake on rate increases, knowing that the lagging impact will do the necessary work.

Just as the Fed vastly overshot the need for economic stimulus after the lockdowns, pursuing inflation and growth, so the bankers are very likely to exceed the rate increases necessary to induce a recession and curb inflation. Prediction is a fool's game that the Fed has been playing far too long.

None of this means the governors will choose 100 points on Wednesday. After two 75 point hikes in a row the Fed has nothing to prove on aggression. However, it does mean the rate endpoint will be higher and further off than it would have been had the Fed not bungled the inflation call, making a deep recession this year or next far more likely.

The Fed should forswear forward guidance and return its monetary policy to the flexibility suited to an uncertain world.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.