Will the US Dollar and Yen continue to defy rate expectations in 2026?

- US dollar poised for negative start to 2026

- Will 2026 be a better year for the yen?

- Fed policy is key amid sticky inflation, jobs weakness and new chair

- Uncertainty to stay high amid trade, AI and fiscal policy risks

Trade war and Fed pause overshadowed 2025

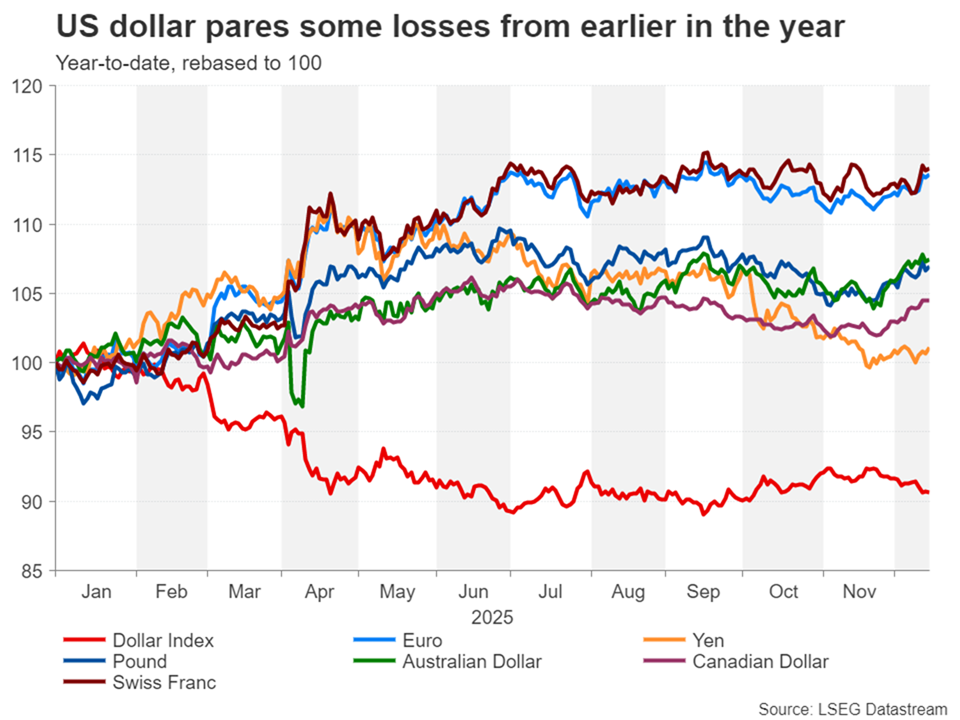

The US dollar looks set to finish 2025 in the red, wiping out the previous year’s gains and sinking to levels last seen in 2022 when measured against a basket of currencies. The losses come despite the Federal Reserve being on hold for much of the year and the eventual resumption of rate cuts not being accompanied by a particularly dovish posture.

Donald Trump’s return to the White House and the launch of Trade War 2.0 certainly hit sentiment for the greenback, as investors feared an all-out tariff war would be more harmful to the US economy than America’s trading partners. However, the Trump administration’s aggressive negotiating tactics, which secured Washington trade deals that were more favourable to the US than its partners, led to a shift in the outlook, spurring a small rebound in the dollar by the summer.

But although recession fears quickly subsided, as Trump backed down from his initial tariff threats, inflation expectations ticked up on concerns that higher levies will push up US goods prices. The Fed had no choice but to adopt a cautious stance, even as it indicated it is willing to overlook temporary spikes in inflation as long as it sees few signs of second-round effects.

Inflation fear and relief

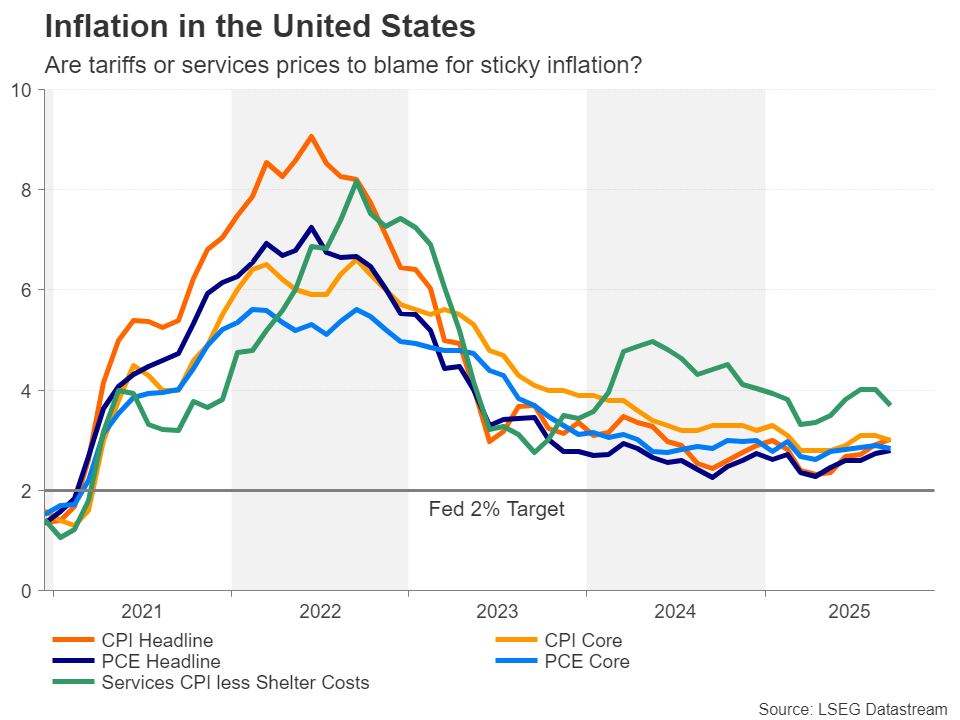

With 2025 almost coming to an end, fears of a tariff-driven surge in inflation have proven unfounded. Early evidence suggests most businesses have absorbed the bulk of the costs of higher import prices rather than pass it onto consumers. However, this is far from the happy ending that Trump could have wished for.

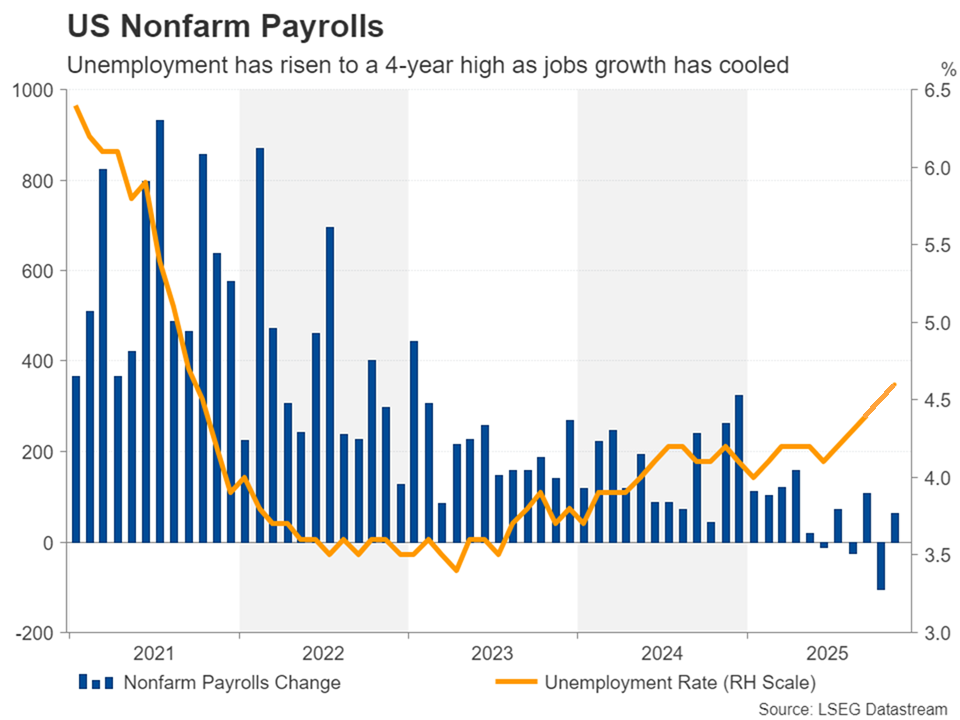

Firstly, companies have responded to the ensuing squeeze in their profit margins by freezing hiring and in some cases, reducing their workforce.

But more importantly, inflation has barely fallen, as services inflation – the primary source of sticky price pressures – has stayed elevated, suggesting strong domestic demand is the Fed’s biggest problem and not tariffs.

Cracks in the labour market

With the labour market stalling, the Fed is faced with the real prospect of stagflation – something that is unlikely to abate in the early parts of 2026. For traders, they’ve been quick to assume that the Fed will respond with greater force to the downside risks to employment than the upside risks to inflation. Fed Chair Jerome Powell, whose term ends in May, has had to steer market expectations to a shallower rate cut path. But with Trump expected to appoint a more dovish candidate as his replacement, many investors are holding on to their bets of several rate cuts in 2026.

The trouble with this scenario is that multiple rate cuts are more likely to come hand-in-hand with a weaker economy than a drop in inflation. With some market commentators pointing to the fact that a hiring freeze usually precedes a jobs cull, a recession, even if it’s only a mild one, cannot be ruled out, especially amidst all the talk of an AI bubble. A crash in AI stocks would almost certainly force tech companies to drastically scale back their AI spending as well as seek savings elsewhere by laying off staff.

Trade tensions ease, for now

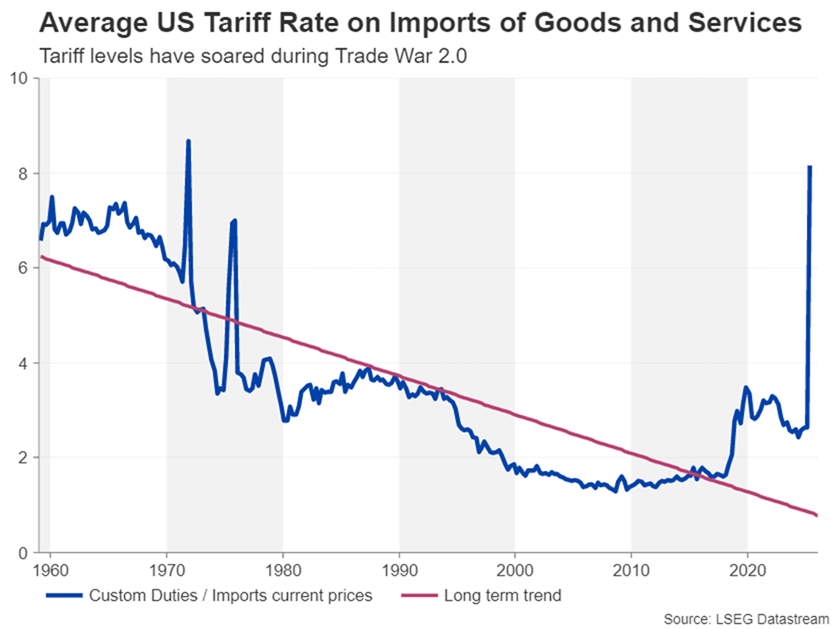

Nonetheless, having come out of the trade war unscathed, the US economy may similarly survive a bumpy ride on Wall Street. There are several reasons for optimism. The White House has signed trade deals with most countries, ending months of tariff-related uncertainty for businesses. Whilst trade risks have not disappeared entirely, for example, the USMCA three-way trade agreement with Canada and Mexico is up for renegotiation in July 2026 and the one-year trade truce with China expires in November 2026, Trump’s more recent actions reflect a desire to de-escalate trade tensions rather than flare them up.

Moreover, although further tariff surprises are highly possible in 2026, the recent announcements of sectoral tariffs have been very targeted, focusing on a much narrower range of products than anticipated. Trump has even been reducing some duties, such as those on food imports, and has made a climbdown on the ban of some chip exports.

Is Trump done with tariffs?

It’s clear that the White House is acknowledging the impact that higher tariffs have been having on households and businesses. And with 2026 being a midterm election year, Trump is pushing for further relief. If Republicans get their way, most American households could be receiving a $2,000 stimulus cheque by the middle of the year. Such a move would be highly inflationary.

Hence, although trade relations with some countries like China could easily sour again over the coming year, the worst of the tariff shock seems to be over. Yes, there’s still a risk of other unexpected surprises, such as liquidity stress in the banking sector, a debt crisis as government borrowing keeps rising, and of course an AI crash. But under the current climate, any weakness is more likely to unfold early in 2026 before growth picks up in the second half, as the Fed’s rate cuts and Trump’s Big Beautiful Bill, as well as potentially the stimulus cheques, boost the economy.

Dollar looks shaky at start of 2026

For the dollar, what is more significant perhaps is that the Federal Reserve has restarted its easing campaign just as most other central banks have ended theirs, with some even considering a rate hike to be their next move.

This theme looks set to prevail at least in the first quarter of 2026. Against the Japanese yen, the key test will be whether any dollar selloff will be large enough to push the greenback below the crucial 140-yen support area, where dollar bulls came to the rescue three times during the past two years.

-1765988766492-1765988766493.png)

The same could happen again in 2026, assuming the 140 level is even tested, as the diverging paths of the Fed and Bank of Japan have so far not fuelled much of a bounce in the yen. Although the yen did begin 2025 on a positive note, it almost fully retraced its gains when the dollar staged a post-Liberation Day recovery. But with the Bank of Japan once again getting ready to raise interest rates, the yen isn’t attracting many bids.

Fed to cut, BoJ to hike, yet no upside for yen

The disappointment that the Fed may not have more than one or two cuts left in its easing cycle is one factor why the dollar is holding firm against the yen. When combined with doubts about how many more times the Bank of Japan will be able to lift rates, there’s even more reason not to get too bullish on the Japanese currency.

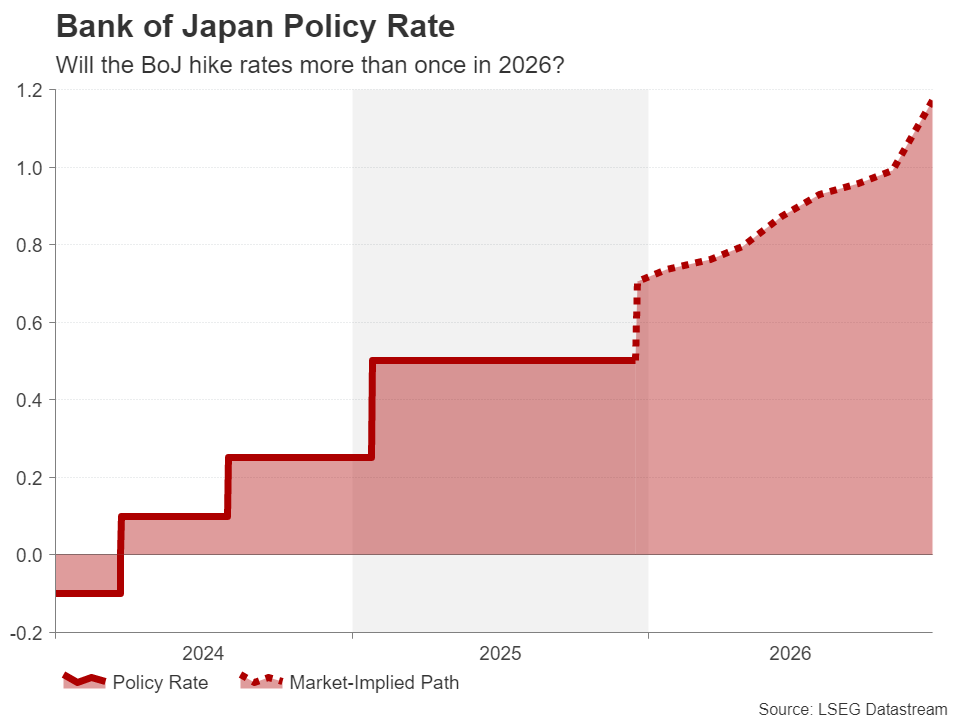

Investors have currently fully priced in just one 25-bps rate hike by the BoJ in 2026, while they see the Fed trimming rates just twice. Hence, the monetary policy divergence may not have much further to go. When considering that any negative developments for the US economy that would prompt the Fed to cut more aggressively would hold back the BoJ’s own tightening plans, as Japan’s economy would also take a hit, there’s little prospect of US-Japanese yield spreads narrowing substantially in 2026.

However, neither does this mean that there is room for more downside for the yen. It’s extremely probable that the Japanese government would intervene in FX markets to defend the yen if it were to depreciate beyond the 158-160 zone.

Will the BoJ be bolder in 2026?

Meanwhile, investors may be underestimating the likelihood of the BoJ hiking rates to more than 1.0%. The new government of Sanae Takaichi has already passed an extra fiscal package of $135 billion, which should bolster growth. If in addition, Japanese businesses pledge pay increases of around 5.0% for the third year running in 2026, the BoJ would be emboldened to stick to its plans to gradually normalize policy.

Sustained wage growth is a key criterion for the BoJ in raising rates and so in the absence of a fresh financial or geopolitical crisis, and the US economy remaining resilient, inflation in Japan would probably continue to stay above the 2% target.

Such an outlook, though, is unlikely to materialize before Q2 2026, and so in the scenario that the dollar rebounds from a weaker first half, the yen could be an exception and maintain any uptrend in the second half. In the event of a yen rally taking off, the 127.50-130.00 region would be one to watch, as breaching it could set off a longer-term uptrend.

Author

Mr Boyadjian graduated from the London School of Economics in 1999 with a BSc in Business Mathematics and Statistics.