Can you have low yields on an inflation narrative that does not also contain an economic slowdown?

Outlook: We are the cusp of a growing Delta Panic or at least a Delta Angst, although we would blame others, too. China’s mysterious attack on cyber and infotech companies is bizarre, even if we think we can understand it from the point of view of the state preemptively protecting itself from moguls. It’s a deliberate rejection of the model in Russia, where privatization bred an elite class of corrupt politicians and their corrupt business cronies. In this context, China’s conduct looks noble in the sense of protecting the general public from capitalist rip-off artists.

But the US gets blame, too. For the Fed to be “removing support” from the economy in the form of tapering at the same time a Delta surge is building is to invite an economic slowdown. That is the message from the bond market as much as its acceptance of the Fed narrative of inflation decelerating.

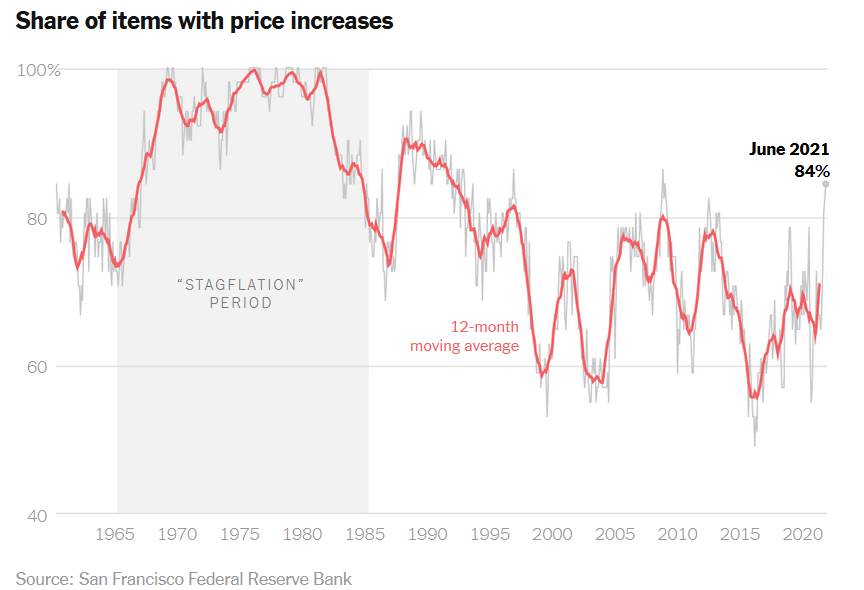

The bond market, from 2 years to 30, is not reflecting expectations of rising inflation. Granted, sticky prices are already falling, according to the St. Louis Fed, where the July reading is a tame 2.4%. The Cleveland Fed has a 10-year forecast of overall inflation at a mere 1.58%. The San Francisco Fed finds that 84 categories of prices are rising and 27 are flat or falling, but this is normal after a recession and nothing to worry about. Notice that the scale of the chart goes all the back to 1964, which messes with your eyeballs.

We have a conflict between recent readings couched in a dozen different ways, and forecasts also measured in a dozen ways. We have month-over-month annualized and year-over-year, not to mention different things included or excluded and seasonally adjusted or not. There is no single inflation number we can pin down as the definitive number. The BLS number for June and July is 5.4%. As for expected inflation, the 5-year breakeven is 2.55%, the 10-year is 2.32% and the 30 year is 2.23%--a falling line.

The high actual at 5.4% and the low expected (2.23-2.55%) all along the yield curve is nice for the Fed, showing the market has confidence in the institution and its ability to judge and manage inflation. Bond traders buying the Fed narrative accounts for the low benchmark 10-year, with maybe a small contribution from those gloomsters who foresee recession arising from the Delta wave.

But a severe conflict is building. Can you have low yields on an inflation narrative that does not also contain an economic slowdown? Last month Goldman projected US growth will slow sharply in 2022, led by a struggling service sector hit by the pandemic. Growth will be a measly 1.5-2.0% in the second half of next year, from 6.6% this year. The labor market will track growth and result in a longer recovery. The Atlanta Fed already has a drop to 6.1% for Q3 this year from 6.8%. A forecast for Q4 can’t be found but if the Delta Angst keeps growing–falling commodity prices, falling stock market indices–we could get a super-bad Q4 and a scary start to 2022.

The hard question is whether this scenario stays the Fed’s hand on tapering. The latest Merrill Lynch investment manager survey shows 84% expect the Fed to taper by year-end, 28% seeing the announcement at Jackson Hole and 33% at the Sept 22 FOMC. Again, tapering is not hiking and everyone still thinks that doesn’t come until 2023, but what if we get vastly slower growth? That would tame inflation for sure and only a fringe of economists see stagflation (although that fringe includes Larry Summers), but it must put the kybosh on the first rate hike.

The degree of slowdown depends on the progress of the Delta wave and thus on the vaccination issue if we believe the Fed’s primary concern is cutting unemployment and somehow getting those 11 million unemployed into some kind of match with those 10 million job openings. This is fitting a square peg into a round hole and will be a problem for years to come–the available labor force is not qualified for the jobs on offer. Much of the labor force can’t go back to work because of child-care issues and fear of catching Delta, along with those who refuse vaccination but work for employers requiring it.

The slow-growth model has not yet caught the imagination and is not the dominant theme today. If stock markets go back to their previous attitude, which can be summed up with “to hell with the pandemic, full speed ahead”– the Delta Angst will fade away–again. This is seemingly what the FX market now believes–at bottom, FX players see equity players are reliably buying the dip and having accepted the idea of the Fed tightening. They are buying dollars on the growth story. They will buy dollars on the gloom scenario, too, as the safe-haven–but the transition from one to the other will be brutal. Keep an eye peeled for stories about a looming slowdown and beware becoming complacent. Also, remember that when the market gets itself into a tangle over the dollar against the majors, the place to be is the crosses.

Note to Readers: We are taking a holiday next week and there will be no reports on Monday, Aug 23 to Friday, Aug 27.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat