ADP Net Employment Change June Preview: Can employment stave off a recession?

THIS CONTENT HAS BEEN DEPRECATED

- Private payrolls are forecast to produce 200,000 new positions, up from 128,000 in April.

- Available jobs remain at an all-time record, unemployment claims are historically low.

- NFP expected to rise 270,000 in June down from 390,000 prior.

- Fed July rate hikes not expected to be conditional on employment.

Markets are suddenly convinced a recession is at hand. Crude oil fell below $100 on Tuesday anticipating collapsing demand if the global economy slides into contraction. Retail Sales and real spending and income in the US were negative in May. Equities are a sea of red this year and Treasury rates have fallen sharply from their post-pandemic highs of just three weeks ago.

Only the labor market is keeping the Federal Reserve’s hope for a soft-landing alive.

Private payrolls from Automatic Data Processing (ADP) are forecast to add 200,000 jobs in June following May’s disappointing increase of 128,000. The three-month moving average that month was 193,000 less than one-third of the 631,000 average in February.

The ADP report on Thursday, one day later than normal because of the US Fourth of July holiday on Monday, is the main lead-in for Nonfarm Payrolls on Friday. The job numbers from ADP, the largest provider of payroll services in the US, are monitored for clues to the national employment figures, even though the directional correlation between the two is weak. In the last year, ADP and NFP have moved together half the time and in opposition half the time. In June, ADP is expected to rise and NFP is forecast to fall.

Labor markets

The main statistics for the US labor market remain positive, though one forward-looking series, the Purchasing Managers Index (PMI) for Manufacturing from the Institute for Supply Management, has slipped into contraction and several others have weakened.

Nonfarm Payrolls have seen the three-month average decrease from 602,000 in February to 408,000 in May and are forecast to continue the trend to 270,000 in June.

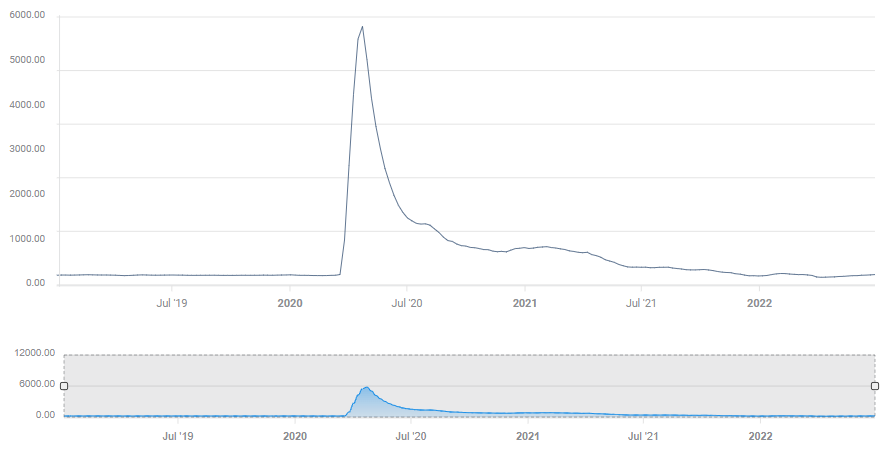

The four-week moving average for Initial Jobless Claims has risen 36%, from 170,250 on April 1 to 231,750 on June 24. While the increase is substantial, unemployment claims are still far below any historical reference and are only slightly higher than the record low before the pandemic.

Initial Jobless Claims

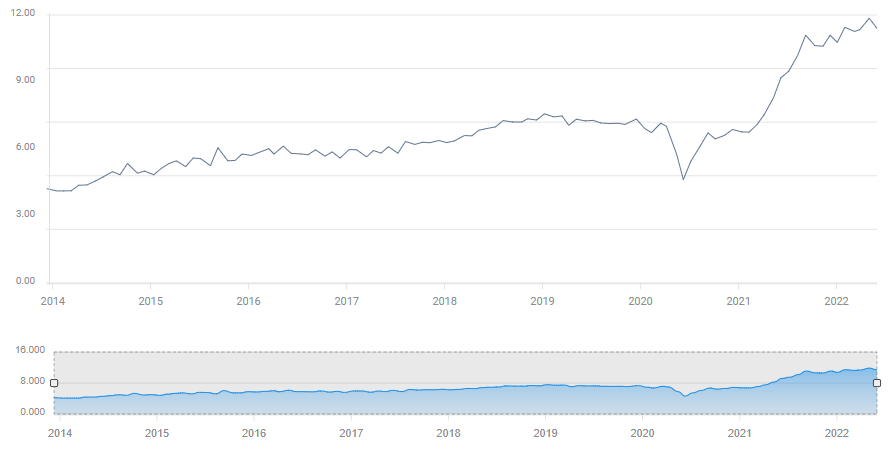

Job prospects are without comparison. The Job Openings and Labor Turnover Survey (JOLTS) average for February, March and April was 11.5 million unfilled positions. May’s 11.0 million forecast will keep the all-time monthly record intact.

JOLTS

June’s PMI for manufacturing employment unexpectedly dropped to 47.3 from 49.6, the second month below 50 indicating contraction. A rise to 50.2 had been predicted. The service employment PMI is expected to drop to 49.8 in June from 50.2 in May.

For most of the recovery the employment problem has been absent workers. People are not returning to their jobs with anything like the anticipated alacrity. The Labor Force Participation rate was 62.3 in May, more than a point below its 63.4 level in February 2020.

While the main statistics remain positive, the NFP and ADP numbers have deteriorated, and the most prescient indicator, manufacturing employment PMI, is in contraction.

Growth and recession

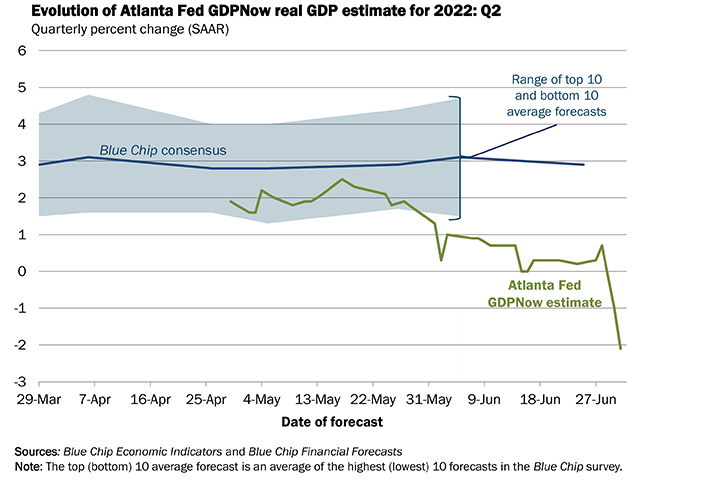

The US economy contracted 1.6% on an annualized basis in the first quarter. Over the past three weeks the Atlanta Fed’s GDPNow model projection for second-quarter growth has fallen into contraction. The July 1 estimate was -2.1%, down from -1.0% on June 30 and 0.9% prior. Those are the first two negative readings for the second quarter.

GDPNow

Federal Reserve

The Federal Open Market Committee (FOMC), the bank's policy-making board, has raised the base rate 125 basis points at the last two meetings.

Headline CPI had jumped to 8.6% in May prompting the 75 point increase on June 15, originally planned at 50 points. The governors are expected to add another 75 points at the July 27 meeting, bringing the upper-target to 2.50%. The Fed’s own year-end projection of 3.4%, implies another 100 points of increases in the three remaining meetings after this month.

Second quarter GDP will be reported on July 28, one day after the FOMC's prospective rate hike. Whether the Fed will be able to continue its anti-inflation campaign if the US is in a recession, is an open question. Fed officials have barely addressed the issue which now seems increasingly likely. Chair Jerome Powell has noted that a so-called soft-landing, where rate hikes reduce inflation without precipitating a recession, is possible, but difficult.

Conclusion: Two scenarios

Employment has been replaced by inflation in the Fed policy hierarchy. The ADP number and its far more relevant successor, NFP, are crucial because the labor market is the last performing sector of the US economy. When hiring falters, a recession is assured.

If ADP payrolls come in at or better than forecast, it will relieve concern, for a time at least, that labor markets have succumbed to the general decline. As the odds are even that NFP will miss forecasts regardless of ADP’s results, markets are unlikely to have a strong response.

If ADP is weaker than expected, concern will adhere to the NFP report, pressuring Treasury rates and equities, but probably giving the US dollar another boost. Markets are so fraught over the prospects of a global recession, that the US dollar safety trade has resumed with a vengeance.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.