Wake Up Wall Street (SPY) (QQQ): Risk-on rally back on, but for how long?

Here is what you need to know on Tuesday, March 8:

Another dizzying day for equity investors on Monday saw more fresh selling pressure as a further surge in oil prices filtered through to the stock market. It was a shocking day for Nasdaq, which collapsed nearly 4% while the S&P 500 signed for a 3% loss. The realisation that this conflict is likely to play out for quite some time has seen a fresh hit to investor sentiment. Oil surged as the EU and US remained at odds over fresh sanctions on Russian energy imports. The EU has no place to go here, and the conflict is driving up the price of Russia's main source of income. Tuesday sees a small bounce for equities as the EU finally talks about joint debt issuance. This was a serious issue back during the Great Financial Crisis and nearly led to the euro collapsing, so it is long overdue. European markets, in particular, are bulled up with the Eurostoxx recovering some 3% this morning and the euro gaining 0.5% versus the dollar.

The surge in energy prices was picked up very cleverly by the retail set on Monday. They identified numerous small-cap energy stocks and drove them up by some huge margins. This is likely to continue Tuesday as risk appetites return slightly.

The dollar is weaker as mentioned at 99.12 now for the Dollar Index. Oil is higher at $124, and Gold is holding at $2,009. Bitcoin trades at $38,700. Bond markets are lower on risk-off, meaning yields are higher this morning.

European markets are higher: Eurostoxx +2%, FTSE +0.4% and Dax +0.6%.

US futures have turned negative: S&P is flat, Dow -0.1% and Nasdaq -0.4%.

Wall Street (SPY) (QQQ) News

EU to consider joint bond sale to fund energy and defence.

EU drafting new sanctions on Russia.

White House set to ban oil imports from Russia.

Russia threatens to ban oil exports to Europe.

TSLA, NIO, RIVN, LCID: Morgan Stanley says nickel price spike has raised costs of EVs by $1,000.

Shell (SHEL) apologizes for buying Russian oil, says it will shut down operations in Russia.

Mandiant (MNDT) to be acquired by Google (GOOGL).

Dicks Sporting Goods (DKS) up 4% on earnings.

Apple (AAPL) holding product launch later today, budget iPhone rumoured.

Hycroft Mining (MYMC) looks to be targeted by retail traders as commodity prices surge.

CEI, MARPS, INDO, HUSA and other small-cap energy stocks are all strong again in the premarket.

Sibanye Stillwater (SBSW): rumours of possible mine strike, stock down 8%.

Dish Network (DISH) upgraded by UBS.

Visa (V) to boost fees charged to retailers.

Tesla (TSLA): China's February deliveries fell MoM due to Chinese Lunar New Year, up 200% YoY.

Ivanhoe Mines (IVPAF): going to make this my new favourite stock, earnings out.

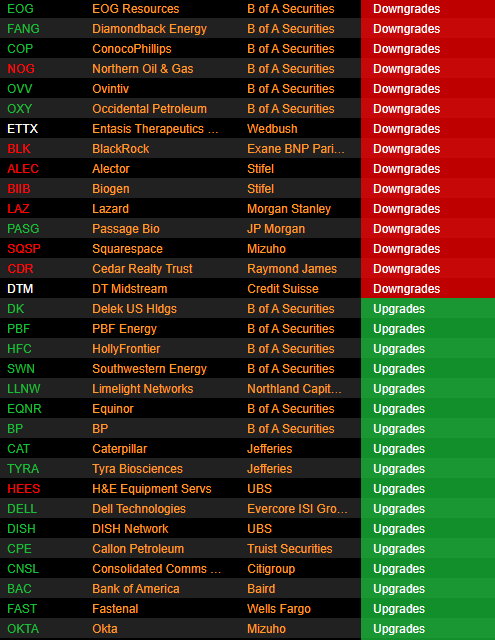

Upgrades and Downgrades

Source: Benzinga Pro

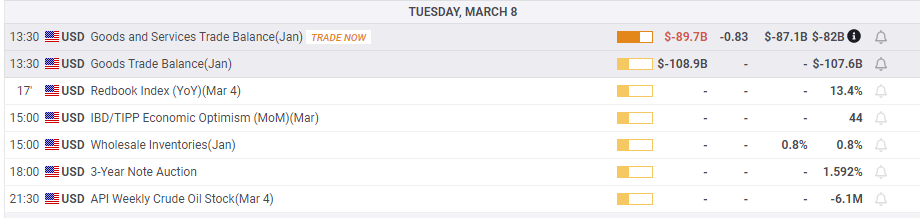

Economic releases

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Ivan Brian

FXStreet

Ivan Brian started his career with AIB Bank in corporate finance and then worked for seven years at Baxter. He started as a macro analyst before becoming Head of Research and then CFO.