Wake Up Wall Street (SPY) (QQQ): Apple bites bears as Amazon prefers clouds over the jungle

Here is what you need to know on Friday, July 29:

Equities:

All eyes were on Apple (AAPL) and Amazon (AMZN) after the close on Thursday, and neither disappointed. Amazon surged 13% in a largely relief rally based on the previous quarter. Apple too was resilient, but Reuters is quoting some analysts as saying Chinese growth is set to slow, which will hit iPhone sales. The CFO also marked down margins, which we think is not being picked up. We are bearish and have updated our price target to $110. Amazon had another shocker on profitability thanks to Rivian (RIVN), but AWS was strong. We have tweaked our model and have a HOLD on AMZN stock.

The weak US GDP number gave more fuel to bulls who see the Fed pivot as more nailed on now as financial conditions continue to ease. After a strong week and with choppiness still the main feature of equities, do not be surprised to see some profit-taking as the week and month come to a close. Overall, we are still favouring equities with positioning still too low.

Bonds

Thursday's weak GDP number saw yields initially move lower, but there was a bit of a retracement overnight. European GDP was not as bad as feared, but European CPI numbers were still too high and yields dragged higher. The US 10-year is back up to 2.7% now after falling to 2.65% in Asia. Money markets are priced for rate cuts in 2023. Fed funds futures see a rate of 3.62% by December 2022 versus 2.88% by December 2023.

Oil market

Oil did not like the US GDP print but got some relief from Europe's GDP this morning. Russia and Saudi Arabia say they are fully committed to the OPEC+ goal of market stability, and there is an OPEC meeting next week. Concerns over global growth and the China slowdown are likely to hamper oil in the near term however.

FX

The yen continues its aggressive unwinding, which could get ugly if this carries on and some serious CTA stops are triggered. This one has been a one-way bet for some time now for trend-following systems. The continued narrowing of the yield spread is hitting the dollar. Thursday's GDP print has just added to this. The CPI overnight from Japan was high, putting more pressure on the BOJ's peg. Overall, the dollar is weaker across the board with the dollar index back to 106.

Bitcoin and Gold

Bitcoin benefited from the risk on pivot by the Fed and has since stabilized around $23,000. Gold is higher after the weak US GDP data and is at $1,758 now.

European markets are mixed: Eursostoxx +0.3%, FTSE -0.3% and Dax +1%.

US futures are higher: S&P +0.65, Dow +0.2% and Nasdaq +1%.

Wall Street top news (QQQ) (SPY)

Eurozone GDP is higher than expected, but so too was CPI. Yields went higher.

Exxon Mobil (XOM) offers up record earnings, beats estimates.

Chevron (CHEV): repeat the above!

Apple (AAPL) beats estimates, but margins are reducing.

Amazon (AMZN) has massive relief rally as AWS impresses.

Astra Zeneca (AZN): strong sales forecasts and earnings.

Intel (INTC) lowers sales forecasts as expects chip demand falling.

ROKU stock lower as ad revenue lower. Revenue estimate for Q3 at $700 million versus $900m consensus.

Proctor & Gamble (PG) barely misses on EPS revenue, but stock down.

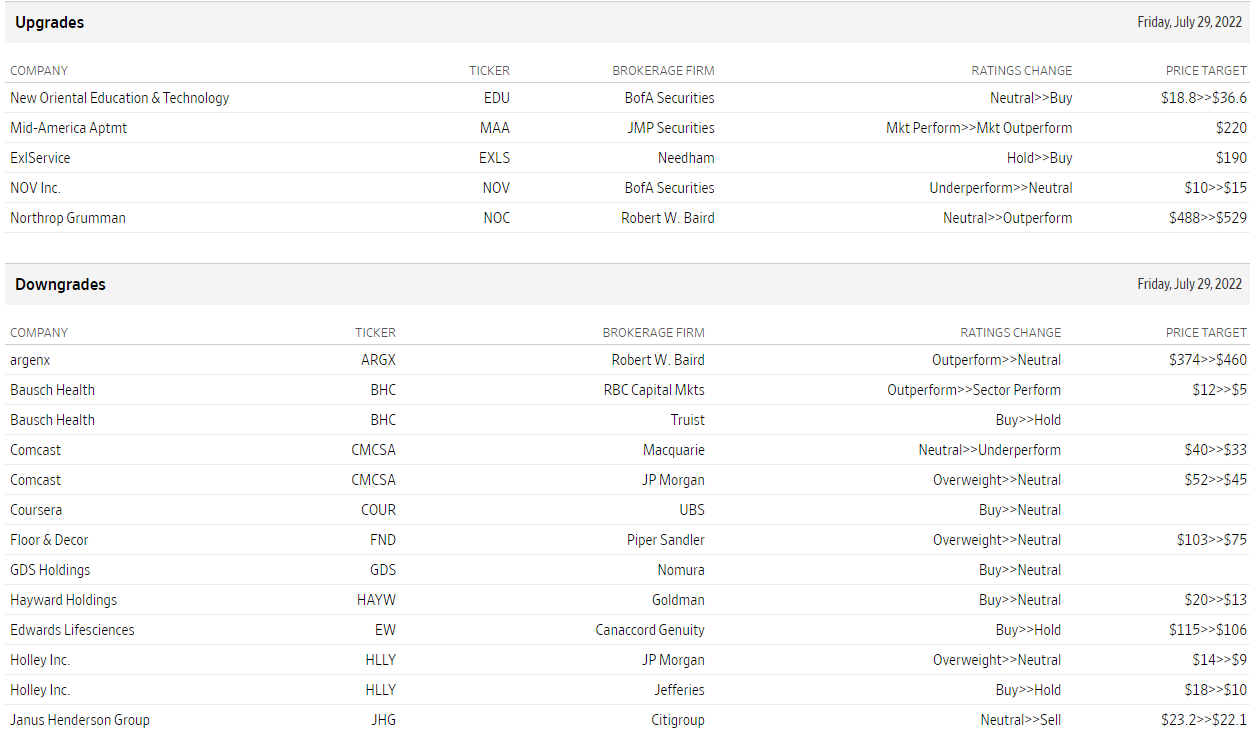

Upgrades and downgrades

Source: WSJ.com

Economic releases

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Ivan Brian

FXStreet

Ivan Brian started his career with AIB Bank in corporate finance and then worked for seven years at Baxter. He started as a macro analyst before becoming Head of Research and then CFO.