USD Index climbs to two-day highs near 106.30, looks at key data

- The index advances modestly early on Monday.

- The dollar regains traction on risk-off sentiment.

- ISM Manufacturing takes centre stage later in the NA session.

The greenback, in terms of the USD Index (DXY), adds to Friday’s small gains and revisits the 106.30 region at the beginning of the week.

USD Index focuses on data

The index advances for the second session in a row on Monday on the back of further correction in the risk-linked universe, while US yields remain directionless ahead of the opening bell in Euroland.

In the meantime, the greenback puts further distance from Friday’s lows in the 105.70/65 band and appears to be retargeting the area of recent 2023 peaks near 106.80 (September 27).

There have been no changes to the monetary policy front so far, where investors continue to price in an extra 25 bps rate hike by the Federal Reserve before year-end. In addition, the dollar gained extra strength after the US averted a federal government shutdown at the last minute, all following a Congress vote to pass a short-term funding bill over the weekend.

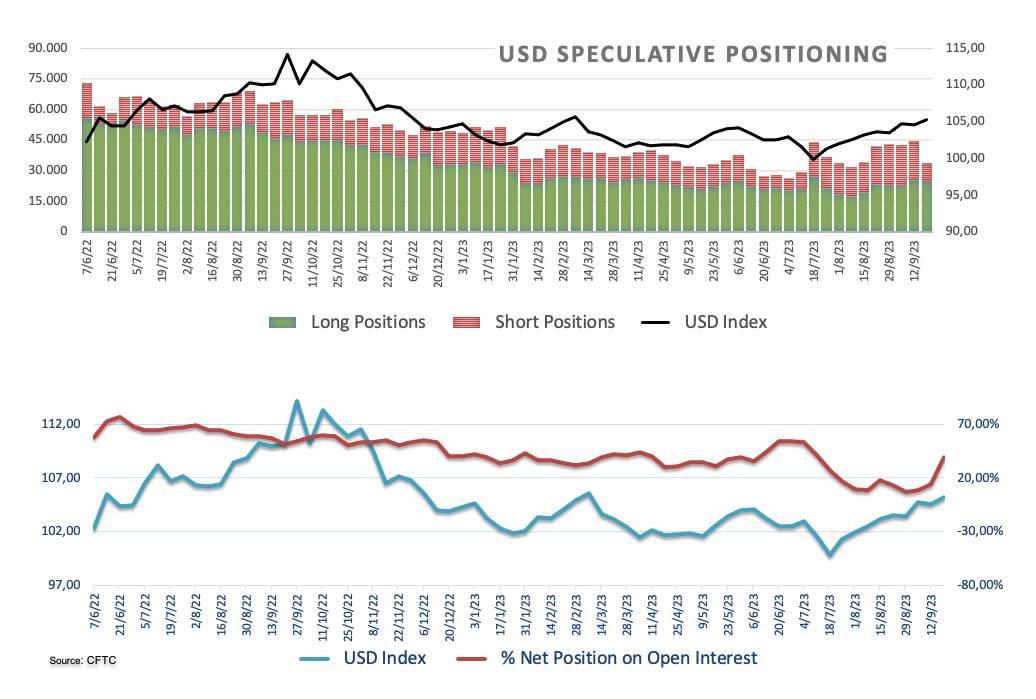

Additionally, the recent rally in the greenback appears supported by the speculative community after net longs in the dollar rose to levels last seen in early January in the week ended on September 26, according to the CFTC’s positioning report.

In the US docket, the ISM Manufacturing PMI will be in the limelight later in the session, seconded by Construction Spending, the final figures of the S&P Global Manufacturing PMI, and speeches by Philly Fed P. Harker (voter, hawk), FOMC Governor M. Barr (permanent voter, centrist), and NY Fed J. Williams (permanent voter, centrist).

What to look for around USD

The greenback looks to extend Friday’s lows, although it seems to have met some initial resistance in the 106.30 region so far.

In the meantime, support for the dollar keeps coming from the good health of the US economy, which at the same time appears underpinned by the renewed tighter-for-longer stance narrative from the Federal Reserve.

Key events in the US this week: Final Manufacturing PMI, ISM Manufacturing PMI, Construction Spending, Fed J. Powell (Monday) – MBA Mortgage Applications, ADP Employment Change, Final Services PMI, ISM Services PMI, Factory Orders (Wednesday) - Initial Jobless Claims, Balance of Trade (Thursday) – Nonfarm Payrolls, Unemployment Rate, Consumer Credit Change (Friday).

Eminent issues on the back boiler: Persevering debate over a soft or hard landing for the US economy. Incipient speculation of rate cuts in early 2024. Geopolitical effervescence vs. Russia and China.

USD Index relevant levels

Now, the index is gaining 0.03% at 106.20 and a breakout of 106.83 (2023 high September 27) would open the door to 107.19 (weekly high November 30, 2022) and finally 107.99 (weekly high November 21 2022). On the other hand, initial support emerges at 104.42 (weekly low September 11) ahead of 103.10 (200-day SMA) and then 102.93 (weekly low August 30).

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.