Q1 2026 equity outlook: Trends intact, sensitivity rising

Q1 2026 sits at a point in the market cycle where many of the obvious questions have already been answered. Inflation is no longer accelerating, the Federal Reserve is no longer tightening aggressively, and recession fears that dominated prior years have eased.

What remains unresolved is how much growth is left, how patient policy will be, and how markets behave once relief has been priced in.

This outlook focuses on that transition. Not on calling a top, but on understanding where optimism remains justified and where risks are quietly building beneath the surface.

What does that mean for equities in the first quarter of 2026?

The big picture: Policy and the unwind story

The macro backdrop has moved beyond crisis avoidance and into second-order effects. Markets are increasingly focused on the idea of a potential yen carry trade unwind, especially as US policy turns more accommodative and Japanese yields rise.

That concern is not baseless, but it is also being overstated by many traders.

At this stage, there are no technical indications that a systemic unwind is unfolding. Price action across equities, volatility, and credit markets does not confirm crisis conditions. What we are seeing instead is heightened sensitivity to a risk that traders know exists, but cannot yet see.

In other words, the fear is visible, but the damage is not.

This creates an important distinction for Q1 2026:

- Policy shifts remain supportive for risk assets.

- Price trends remain constructive.

- Markets are becoming more reactive to underlying funding risks.

The prevailing mode is therefore cautiously bullish, not complacent. Participation remains justified, but awareness matters more than it did earlier in the cycle.

To understand why this risk is being talked about at all, we need to look at Japanese yields.

Japanese yields: Why the market is watching closely

Before diving into our equities analysis, let’s first set the big picture.

For years, Japanese bond yields barely moved. That made the yen cheap to borrow and easy to sell, which helped fund global risk trades across equities, credit, and commodities.

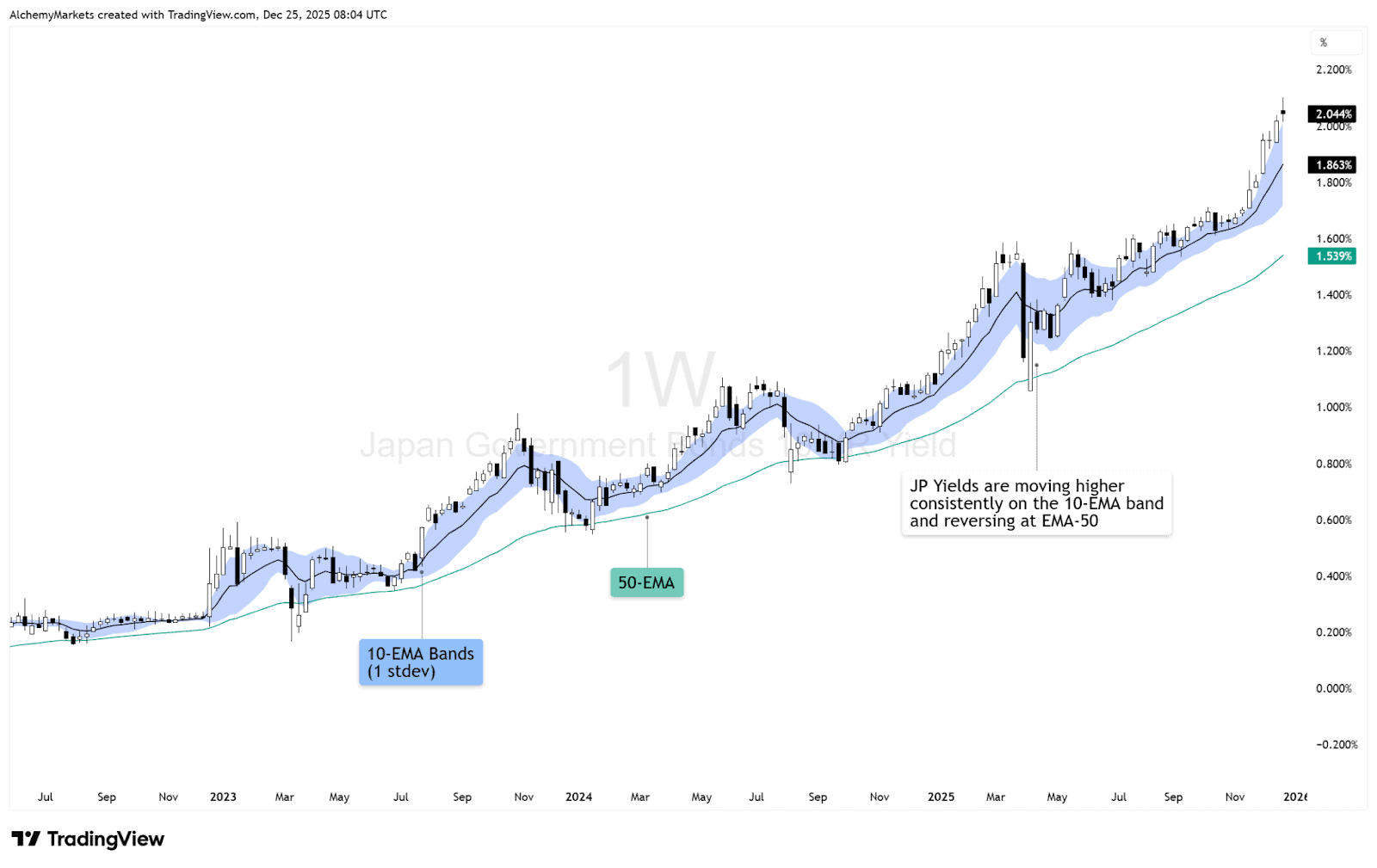

That regime has clearly changed in 2025. Japanese 10-year government bond yields have risen to their highest level in over a decade, pushing above key technical levels and trending firmly above the 10-EMA. This is not a short-term spike. It reflects a structural shift away from extreme yield suppression.

What the magnitude tells us:

- Yields are no longer anchored near 0-1%.

- Funding conditions tied to the yen are slowly tightening.

- The era of frictionless yen borrowing is fading.

This explains why traders are alert. However, it is important to be precise.

Historically, carry trade stress only becomes destabilising when yield moves are fast, disorderly, or policy-forced, particularly in correlation to the US 10 Year Yields.

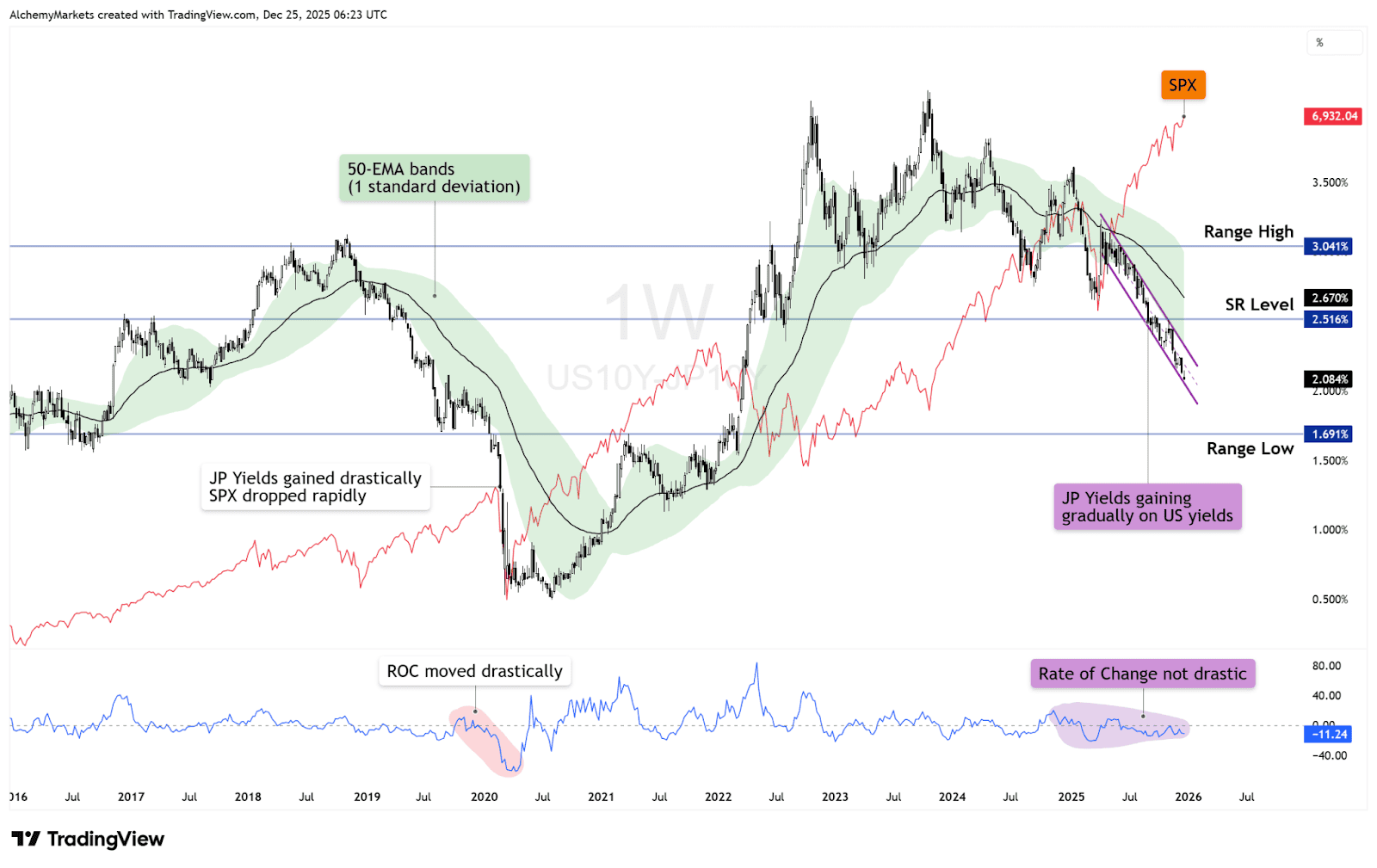

If we take a look at the US 10 year yields MINUS Japanese 10 year yield chart (Weekly timeframe), the context becomes obvious:

Notice how the S&P 500 typically suffers sharp drawdowns only when US yields collapse rapidly against their Japanese counterparts.

Therefore, the implication is not an imminent crisis, but reduced tolerance for excess leverage. Risk-taking adjusts before it unwinds. That is the phase markets are currently in.

Author

Zorrays Junaid

Alchemy Markets

Zorrays Junaid has extensive combined experience in the financial markets as a portfolio manager and trading coach. More recently, he is an Analyst with Alchemy Markets, and has contributed to DailyFX and Elliott Wave Forecast in the past.