Meta vs Alphabet: Has the tide turned?

Key points

-

Meta’s AI-driven ad strategy is delivering stronger returns, while Alphabet’s AI investments face skepticism, especially in Search.

-

Meta’s profitability and cost discipline are outpacing Google, with better operating margins and more efficient capital spending.

-

Risks differ as Meta is heavily dependent on ad revenue and economic cycles, while Alphabet faces a potential DOJ settlement and AI competition in Search.

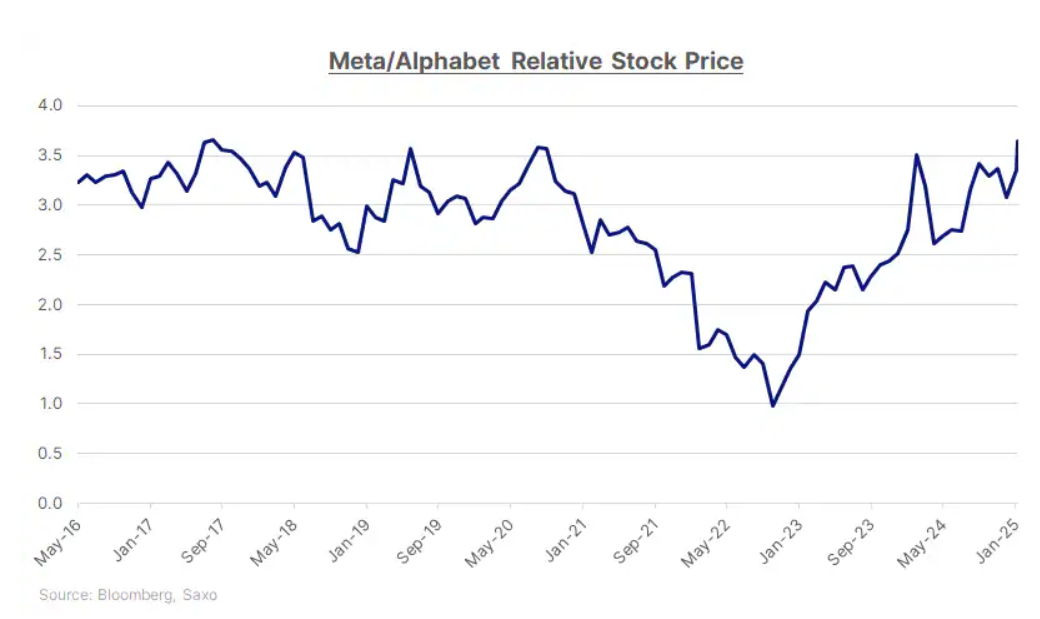

In the competitive landscape of tech giants, Meta Platforms (META) has recently outperformed Alphabet Inc. (GOOGL), the parent company of Google. The relative stock price of Meta vs. Alphabet has reached a 7-year high, raising the question whether Meta’s outperformance has just began, or has it gone too far?

Meta’s AI monetization justifies its AI spend

Meta is pouring a massive $65 billion into capital expenditures (capex), primarily for AI infrastructure, and investors are rewarding it. The stock has surged as Meta has effectively leveraged artificial intelligence (AI) to enhance ad targeting and optimize performance, bringing tangible improvements in engagement and revenue growth.

Meanwhile, Alphabet’s $75 billion capital spend rattled investors, given the tangible returns on AI investments have been less evident so far. In fact, investors are concerned that AI-powered search tools such as ChatGPT and Perplexity AI could disrupt Google’s core search advertising model rather than enhance it.

Meta’s cost discipline and soaring margins

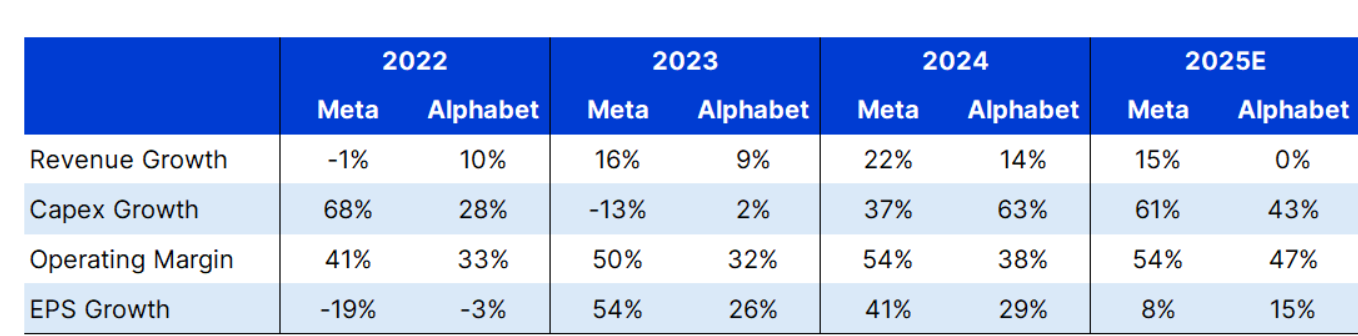

Despite its aggressive AI spending, Meta’s operating margins are soaring. Meta’s 2024 operating margin of 54% is a big jump from 41% in 2022. The company has maintained a stable ratio of capex to operating cash flow, lower than 2021 and 2022 levels, while still seeing strong earnings growth. Meanwhile, Alphabet’s capex growth in 2024 of 63% has outpaced its profit growth of 29%, a sign that its spending isn’t translating into immediate bottom-line gains.

Both companies have made significant cuts to improve efficiency, but Meta’s turnaround feels more dramatic. After its painful “Year of Efficiency” in 2023, Meta has emerged as a leaner, more focused company. Alphabet has also streamlined operations, but regulatory concerns and AI uncertainties still loom over its long-term growth.

Source: Bloomberg, Saxo

Meta’s lead in social engagement vs. Google’s search dependence

Meta owns Facebook, Instagram, and WhatsApp, which remain dominant in user engagement. These platforms generate massive first-party data crucial for ad targeting.

Meanwhile, Google’s core revenue still relies on Search ads, which, while highly profitable, face new challenges from AI-powered search experiences (e.g., ChatGPT, Perplexity AI). If AI-driven answers reduce search queries, it could impact Google’s ad revenue model.

Regulatory overhangs: Meta clears hurdles, Google faces DOJ risks

For years, Meta was in the regulatory hot seat, facing scrutiny over data privacy and competition concerns. But in 2024, those worries largely faded. TikTok once posed a major threat, but the regulatory risks surrounding the Chinese app have largely eased.

Alphabet, however, is facing antitrust cases from the US Department of Justice (DOJ) to prevent it from maintaining its monopoly in online search and other areas. If there is no settlement, that could Alphabet’s ability to maintain dominance in search and digital advertising.

What could go wrong for Meta?

Meta’s economic dependence: With 98% of its revenue coming from advertising, Meta is highly cyclical. If the economy weakens or unemployment rises, small and medium-sized businesses—the backbone of Meta’s ad revenue—could pull back on spending. Google, by contrast, has a more diversified revenue base, with 22% coming from cloud services, subscriptions, and other sources.

DeepSeek cheap AI models could shake things up: China’s DeepSeek AI project, with a $6 billion spending, could reshape the AI competitive landscape, questioning all of the big capex spenders in the AI space. Meta’s capex growth is projected to outpace profit growth in 2025, raising questions about whether the company can maintain its current efficiency. Alphabet’s capex is also expected to rise faster than profit, but at a slower rate than Meta’s.

YouTube’s AI growth potential: YouTube has been one of Alphabet’s brightest spots, with AI-powered content discovery boosting engagement and ad revenue. If this momentum broadens, it could offset some of the challenges in Google’s core search business.

Valuation: How Much More Upside? Alphabet is trading at 20x forward earnings, right around its 5-year average. Meta, in contrast, trades at 27x – way above its 5-year average of 19.5x. This gives more room for Alphabet to expand its multiple compared to Meta.

Bottom line: The risk-reward balance

Meta has outperformed Alphabet in recent months, fueled by AI-driven ad growth, improving margins, and regulatory tailwinds. But with economic risks, rising capex, and valuation concerns, it may not have unlimited upside from here.

Alphabet, meanwhile, is at a crossroads. If AI enhances its core businesses rather than disrupts them, its lower valuation could make it an attractive long-term play. But if regulatory risks and AI cannibalization persist, it could struggle to keep up.

For now, Wall Street is favoring Meta – but the race is far from over!

Read the original analysis: Meta vs Alphabet: Has the tide turned?

Author

Saxo Research Team

Saxo Bank

Saxo is an award-winning investment firm trusted by 1,200,000+ clients worldwide. Saxo provides the leading online trading platform connecting investors and traders to global financial markets.