GME Stock: Nothing can go down in a straight line as GME rallies hard, still overvalued long term

- Gamestop rallied sharply on Thursday, up 30%.

- Results were decent but nothing to justify the current share price.

- GME hinted at a capital raise in an SEC filing.

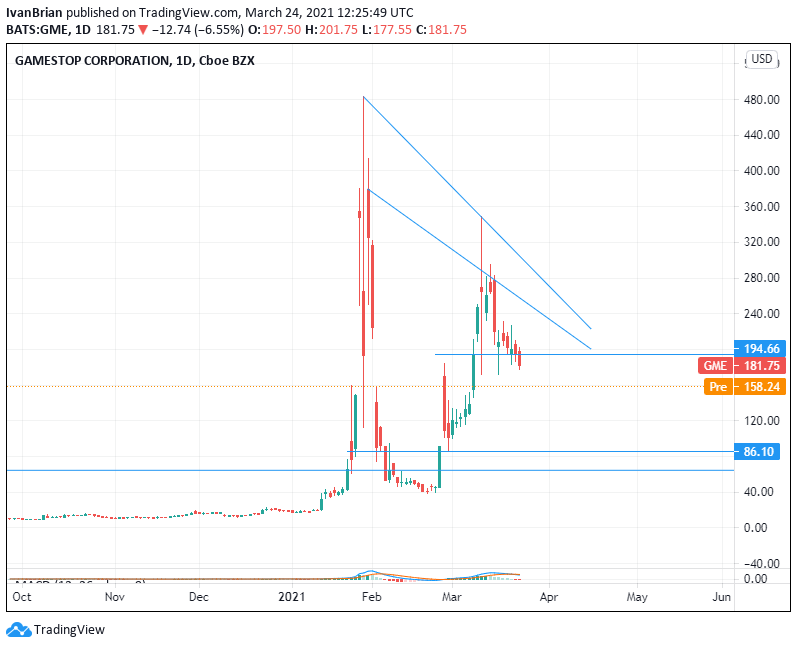

Update: Gamestop has fallen sharply since releasing results and a lack of guidance on Tuesday. GME hinted at a possible share raise as well which further weighed on the stock. On Thursday GME shares are recovering some lost ground and are up 33% at $160. GME shares had fallen from $200 to $120 post results.

GameStop shares disappointed traders after the close on Tuesday when the beloved meme stock released Q4 results. What may have disappointed investors most was the absence of Ryan Cohen from the conference call. Retail investors have seized on Ryan Cohen as the turnaround king after having catapulting Chewy from a legacy pet retailer to a thriving e-commerce concern.

Stay up to speed with hot stocks' news!

The lack of a Q&A section post conference call and any future guidance also disappointed.

GameStop is a struggling online video game retailer with shops located all around the world selling – yes, you guessed it – video games. As we all know, retail is a struggling space as online continues to take over, and this has been a trend for GameStop too. As a result, Gamestop was heavily shorted by hedge funds as they bet that the price would decline further. That's when the fun began with retail traders on Reddit's r/WallStreetBets forum mobbed the stock and moved the shares to nearly $500 in January, before sliding back to sub-$50 by mid-February and now currently trying to hold $200.

GME Earnings

For starters, the earnings are not actually that important. GameStop has long moved away from fundamentals to be a strongly momentum-driven play. But if that is your thing, then here goes.

EPS came in at $1.34 versus a $1.35 expectation. Not bad! Revenue was $2.12 billion, missing the $2.21 billion estimate. This is a fall of 3% YoY. Yes, digital sales did grow, but so did virtually every other retailer as that was the only option during the pandemic. Disappointingly, GME did not provide any outlook for future earnings.

Tellingly, the company did mention a potential share sale.

"Since January 2021, we have been evaluating [...] whether to potentially sell shares of our Class A Common Stock [...] primarily to fund the acceleration of our future transformation initiatives and general working capital needs," GameStop said in a regulatory filing on Tuesday.

But the valuation has gotten way out of any normal criteria. The GameStop P/E ratio is 134, but its Refinitiv forward P/E is 1834! It aims to transform to digital and compete with BestBuy, Target and Walmart, who have P/Es around the 20-30 level. Even Amazon only has a P/E of 75. Nintendo and Sony, which it will compete with for online sales, have P/Es of 17 and 13, respectively. The entire US gaming market is valued at $41.3 billion, according to Newzoo. Gamestop's market cap is nearly a third of this at $13 billion.

There is no valuation metric that can justify such a high GME share price. The initial r/WallStreetBets argument was very clever: GameStop was over shorted but could survive, so squeezing the shorts would make for a self-sustained move. That was a brilliantly executed plan. But as a long-term investment, this is a bubble in the same ilk as Tulips, South Sea, and the 2000 Dot-com Bubble. Gamestop has a future, and Ryan Cohen may well execute on the digital strategy, but the current valuation is just much too high. Be careful and manage your risk in this one.

The author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

This article is for information purposes only. The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice. It is important to perform your own research before making any investment and take independent advice from a registered investment advisor.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to accuracy, completeness, or the suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. The author will not be held responsible for information that is found at the end of links posted on this page.

Errors and omissions excepted.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Ivan Brian

FXStreet

Ivan Brian started his career with AIB Bank in corporate finance and then worked for seven years at Baxter. He started as a macro analyst before becoming Head of Research and then CFO.