First Venezuela, now Iran: The US-China energy war escalates

At first glance, the latest escalation involving the United States with both Iran and Venezuela looks like another chapter in a long-running geopolitical story. But viewed through a broader strategic lens, something else may be unfolding: Energy.

Behind the diplomatic pressure, sanctions threats and regional tensions lies a quieter reality: China’s economic rise remains deeply dependent on securing access to imported energy.

And that vulnerability is not lost on Washington.

China’s energy lifeline

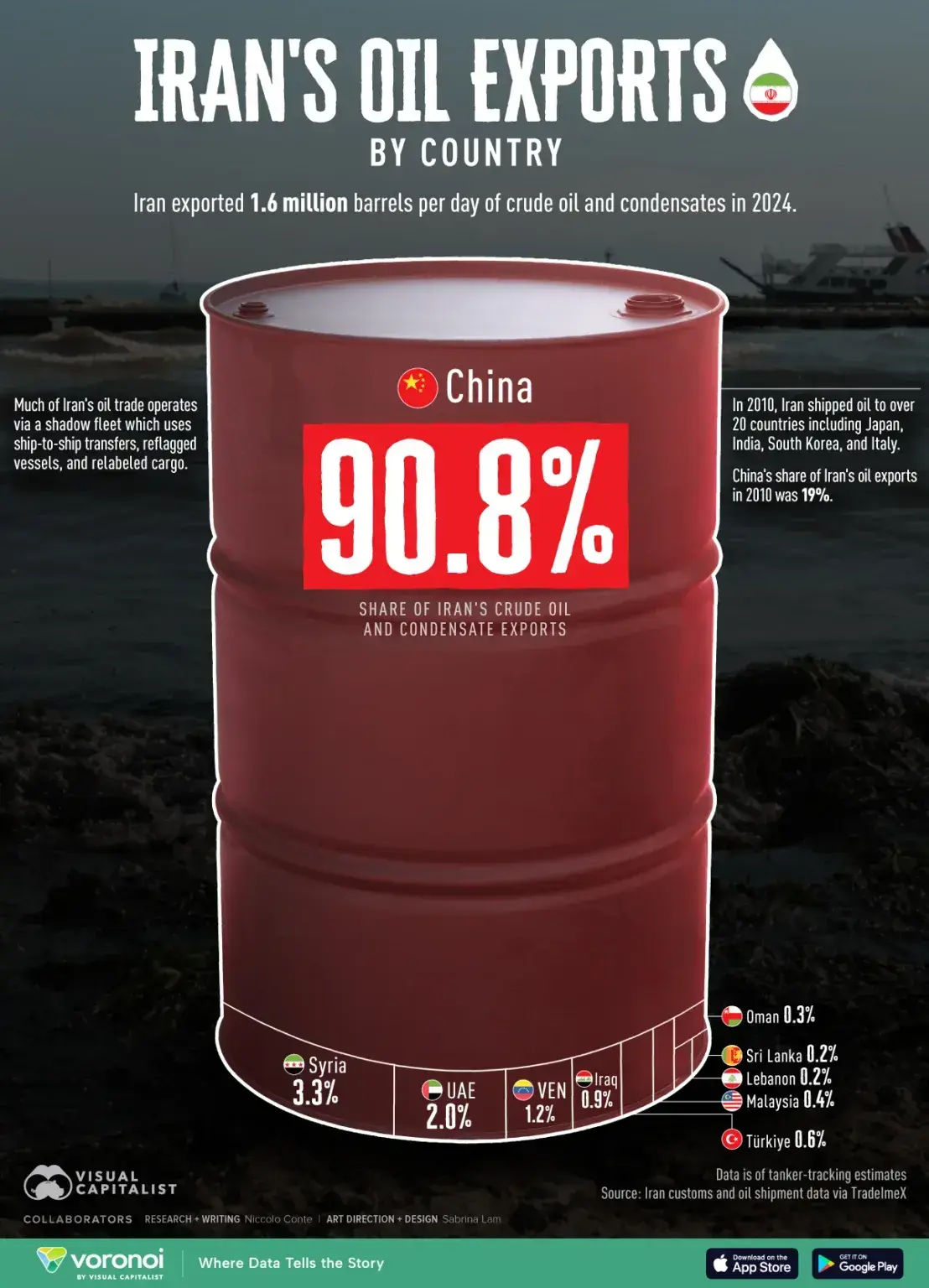

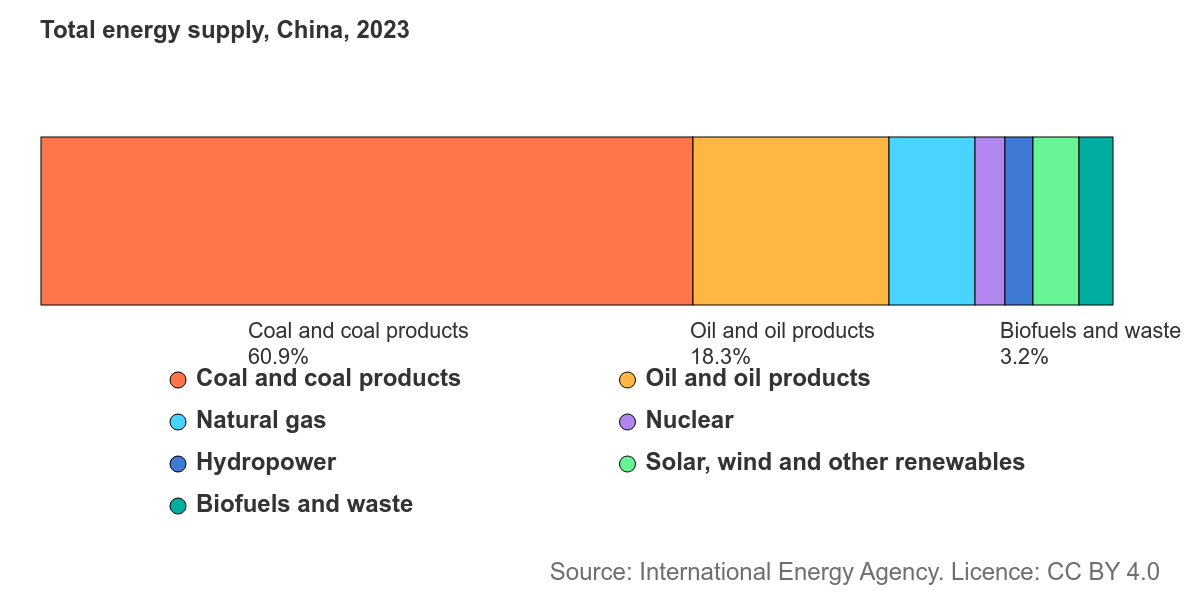

China sits at the centre of global energy demand. It is the world’s largest importer of oil and one of the fastest-growing consumers of Liquefied Natural Gas (LNG). A sizeable share of those imports comes from regions that now sit at the heart of rising geopolitical tensions.

Iranian Crude has increasingly become a key source of discounted supply for Chinese refiners. Venezuelan heavy Oil plays a similar role for certain industrial processes. On top of that, producers across the Middle East remain central to China’s broader energy security strategy.

Much of that energy flows through fragile corridors, most notably the Strait of Hormuz, one of the most critical chokepoints in global energy trade.

When so much supply travels through a handful of sensitive routes, the balance of power shifts. Energy security becomes not just an economic issue, but a geopolitical one.

Pressure on the margins

Recent US actions targeting Iranian and Venezuelan energy flows are often presented as sanctions enforcement or part of a broader regional security strategy. But the implications stretch well beyond those immediate goals.

Any disruption or tightening of supply from those sources forces buyers back into the global market. For China, that means facing stiffer competition for available barrels and LNG cargoes.

In practice, that usually translates into two options: paying higher prices or scrambling to secure alternative supplies. Either way, the pressure gradually builds at the margins of the global energy system.

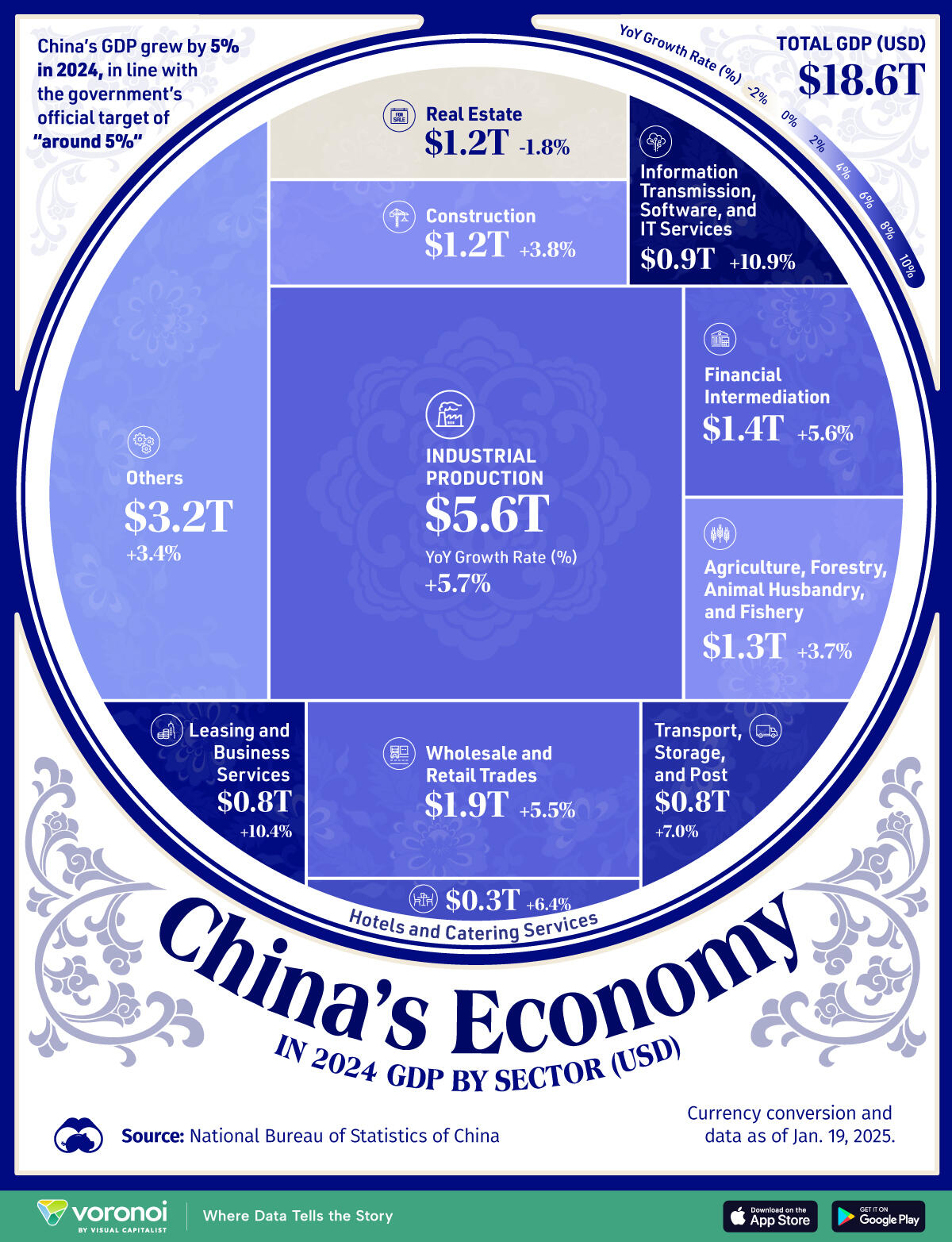

Energy costs matter enormously for an economy built on industrial production, heavy manufacturing and export competitiveness. This is because higher input costs eventually show up somewhere: in margins, in inflation, or in slower growth.

Energy as strategic competition

The idea that energy can serve as a geopolitical tool is hardly new. But in an era of strategic rivalry between Washington and Beijing, access to affordable fuel becomes more than just an economic question.

It becomes a lever.

Constraining energy flows does not require a full blockade. Sometimes it simply requires tightening supply at the margin, raising uncertainty, or increasing transport and insurance costs.

Over time, those pressures accumulate.

Commodity and currency spillovers

If energy costs rise structurally for China, the effects would not be confined to domestic growth.

China sits at the centre of the global commodity ecosystem. Its demand influences markets from iron ore and copper to LNG and coal.

A sustained energy squeeze could therefore ripple outward:

- Industrial production slows.

- Commodity demand softens.

- Export competitiveness weakens.

For currency markets, energy pressure on China matters more than it may first appear.

China is Australia's biggest commercial partner, and changes in Chinese industry swiftly affect the market for Australian goods. Chinese manufacturers would have to pay more for inputs and have smaller profit margins if energy prices go up or become less stable. That may therefore slow down the speed of business and demand for goods.

For the Australian Dollar, the link is indirect but powerful. A China facing higher energy costs tends to import less iron ore, coal and LNG at the margin, weakening one of the key external pillars supporting Australia’s terms of trade.

The strategic layer

None of this suggests that energy pressure alone can derail China’s growth.

But it does highlight a less visible dimension of modern geopolitical competition. Increasingly, countries are not confronting each other directly, they are applying pressure through supply chains.

Indeed, most energy markets are particularly sensitive to this kind of strategy. The global balance between supply and demand is often thin, leaving little room for disruption.

As a result, even relatively small shifts in supply can trigger disproportionately large moves in prices.

All in all

For now, this remains a geopolitical story. But energy flows are rarely just about geopolitics. They shape industrial costs, trade balances and ultimately growth trajectories.

If pressure on Iranian and Venezuelan supply persists, or if transport risks through the Strait of Hormuz intensify, the implications could extend far beyond the Oil market.

China’s economic model relies on secure access to energy. Any sustained disruption raises the cost of that model.

Energy markets tend to react first. Macro consequences usually follow.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.