Fed hawkish, but US dollar yet to prove its worth as Evergrande risks fade

- Fed turns more hawkish and likely more ready to taper next month.

- Risk assets remain in demand despite the hawkish tones and US dollar struggles to breakout higher.

The Federal Reserve surprised markets on Wednesday with a slightly more hawkish tone from its board members following a two-day Federal Open market Committee that concluded today.

The outcome gave rise to volatility across financial and commodity markets yet left some questions as to why the US dollar was down on the knee-jerk and risk assets higher.

Evidently, there has been a lot of pent-up demand for risk associated assets given the coronavirus spread, higher inflation prospects and an underbelly of risk associated with China.

A Gray Rhino event that took markets off guard last week came with what was once China's leading property developer, Evergrande, coming very close to defaulting on billions of dollars of debts liabilities.

However, the debt-laden property developer has agreed to settle interest payments on a domestic bond on Wednesday and the Chinese central bank injected cash into the banking system, temporarily soothing fears of imminent contagion in financial markets.

What we are seeing is a relief rally in that the Fed is likely still no closer to a taper announcement, in reality, to where it was last month despite the hawkish tone from its statement and the dot plot. The most hawkish of the market was looking for a fixed announcement of when the taper will commence and we did not get that today.

Instead, it is slightly more probable that an announcement will come next month, depending on the next employment report. A really bad jobs report next month would likely prevent lift-off in terms of tapering. However, rate lift-off may be closer at hand according to the dots. Therefore, the dollar could still attract some demand near-term once the dust settles today.

All eyes on Fed Powell

Federal Reserve chairman's press conference is underway. Jerome Powell is now answering questions related to the timings of tapering as well as inflation, economic outlooks and rate hikes. Evergrande and corporate debt is also a topic in discussion and Powell feels there is not a lot of direct exposure to the US nor its corporate sector as a parallel.

Risk markets in demand

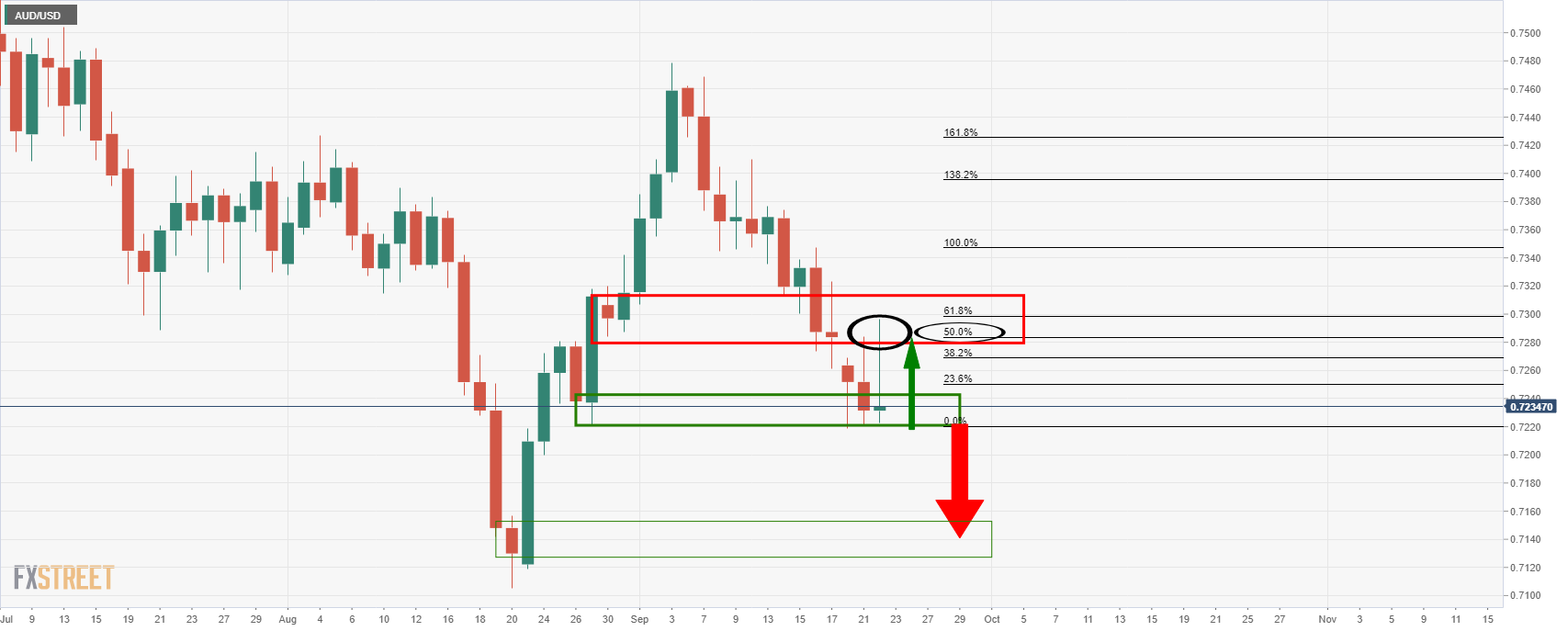

AUD/USD is better-bid as it moves in on the 50% mean reversion target, as projected in the following prior analysis:

As seen, the target has since been achieved and the dollar is battling back, forcing the price into support again. This could equate to the next leg lower if a hawkish Fed gains traction over coming days and weeks.

S&P 500 Index climbs above 4,400 after FOMC announcements

-637679337159363111.png)

The US stock market is still trying to digest the conflict between the hawkish Fed and the Evergrande situation. However, the levels have been marked between near 4,380 and near 4,420 in the case of the S&P 500 benchmark.

DXY attempts to breakout

The Us dollar is catching a bid here at the time of writing as Powell gives the nod to taper next month:

However, while there are prospects of a break-out, there is still a lot more work needed by the bulls until the greenback proves it worth when looking to the daily chart:

93.50 is a critical level ahead of 93.80. Only a break of 93.80 will likely seal the deal for the bulls with targets into the 94 areas and above as earlier than expected US rate rise sentiment takes traction in markets.

Author

Ross J Burland

FXStreet

Ross J Burland, born in England, UK, is a sportsman at heart. He played Rugby and Judo for his county, Kent and the South East of England Rugby team.