DXY inter-markets: looking for a (strong) catalyst

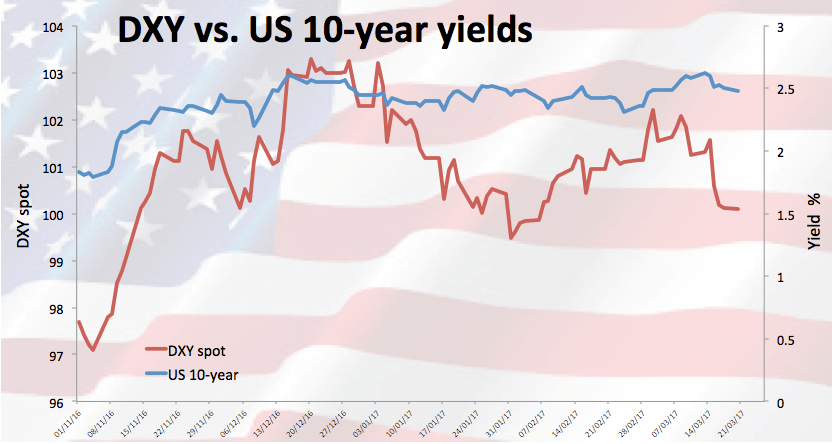

The US Dollar Index – which tracks the buck vs. its main rivals – is trading in a narrow range today, gravitating around the psychological 100.00 handle although without a clear direction for the time being.

Earlier comments by FOMC governors Harker and Evans were supportive of further tightening by the Federal Reserve in the next months. They have even hinted at the possibility of four rate hikes as long as the economy accompanies. However, a tough hurdle still remains the uncertainty around Trump’s fiscal plans, which once unveiled, could be the next significant trigger for another and more sustainable leg higher in the buck.

Yields in the US money markets stay depressed, practically ignoring today’s Fedspeak and trading in the lower end of the daily range, while scepticism on the ability of the Fed to accomplish its goal remains on the rise and hence weighing on sentiment.

In the meantime, the longer-term constructive view around USD stays unchanged while above the support line off 2016 low (91.88 on May 3), currently around 98.15, while YDT low at 99.19 (February 2) emerges as the interim support. A lot of relevant levels lie on the way up, although the most important thing for the greenback in the very near term is to regain confidence and the upbeat sentiment.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.