AAPL Stock Forecast: Apple Inc price remains strong as it straddles tech and value

- AAPL the trillion-dollar now two trillion dollar company!

- Apple stock has been a laggard as tech suffered.

- Buffet last sold some but is he wrong this time?

Rumours of Apple's demise have been greatly exaggerated, but the stock is lagging recently as tech and the Nasdaq bow to the reopening stocks. AAPL topped out in January at $145.09 and has retraced since. Apple dropped to $116.21 before recovering some ground.

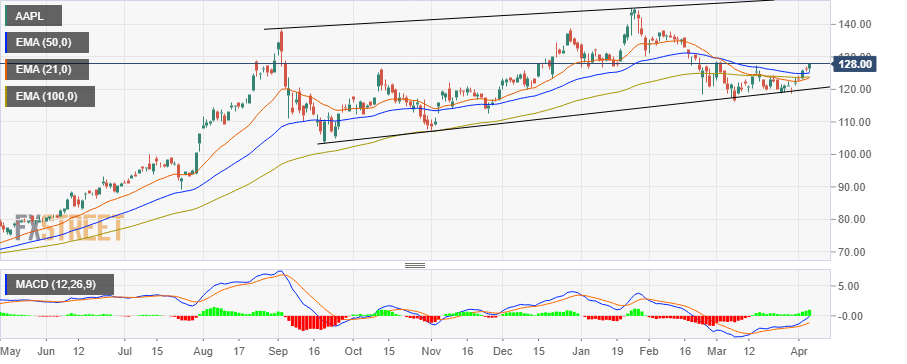

Currently AAPL stock is trading at $128.09 in Thursday's pre-market.

Is Apple stock going to split

Apple did a 4 for 1 share split in 2020, which has meant the shares look more affordable to the retail investor perhaps due to psychological effects. Berkshire Hathway is Apple's biggest shareholder and is famously known for never doing a share split. Hence Berkshire shares trade at a whopping $395,888! Apple has previously done share splits in the past as well: a seven-for-one in 2014. Future share splits cannot be ruled out. However, for now given the recent one in 2020, it will be a while longer for another split or else the stock needs a decent run-up in the share price.

Apple stock forecast

Apple is a resounding success with strong growth metrics, a loyal consumer base, and brand recognition beyond any other company. Recent earnings per share (EPS) forecasts show growth may be slowing as analysts predict a 30% growth rate falling to under 10%. But the pandemic lockdown has seen a rise in exercise-related product sales, and Apple has positioned the Apple Watch as the premium must-have fitness wearable. Partnerships with Nike for Apple Watch have added to its status. Loyalty to the Apple iPhone is unlikely to diminish any time soon as recent security concerns have seen Apple take the so called moral high ground in terms of data sharing and security features. Consumers, even those outside the Apple ecosystem, do see Apple products as probably more secure than competitors.

Growth metrics may be forecast to slow with EPS growth set to drop from above 30% to below 10% as mentioned, but that is assuming constant metrics with products and sales. Apple though is nothing if not innovative, so expect new product features and new products in the years ahead to sustain growth. We are in an ever increasing and quickening technological revolution, and product innovation is Apple's strong point. Consumers know and trust that Apple will provide a cutting edge, quality-designed product, and that is why launches are always a catalyst for Apple's finances. The company is rumoured to be launching wearable glasses, a new watch, a car partnership. The list is endless. This is a company that never stands still and has the cash and know-how to try new products. Some will fail, but others will likely become blow outs. That is the Apple way.

Revenue growth is also forecast to slow, from an impressive +20% to a lower 5-7% range. Again, this assumes static product rollout without any kickers from new products. While Buffet may have sold recently, it was a minuscule amount. Berkshire is Apple's largest shareholder, and the world's greatest value investor does not make too many mistakes. As a value investor Buffet likely sees the outstanding management, a strong balance sheet and revenues setting the company up for further appreciation. Buffet is notoriously wary of growth stocks, but Apple straddles both value and growth.

Apple technical analysis

AAPL shares have retraced nicely from earlier highs to put in a consolidation phase. MACD has crossed and given a buy signal and a break above $128 moves the stock out of the recent range and brings new highs into view. The 50 and 21-day moving averages have also worked well, and AAPL broke these and remains above all key averages, a bullish trend.

At the time of writing, the author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

This article is for information purposes only. The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice. It is important to perform your own research before making any investment and take independent advice from a registered investment advisor.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to accuracy, completeness, or the suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. The author will not be held responsible for information that is found at the end of links posted on this page.

Errors and omissions excepted.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Ivan Brian

FXStreet

Ivan Brian started his career with AIB Bank in corporate finance and then worked for seven years at Baxter. He started as a macro analyst before becoming Head of Research and then CFO.