A closer look at Q2 earnings: What can investors expect?

Here are the key points:

Total S&P 500 earnings for the June quarter are expected to be up +4.9% from the same period last year on +3.9% higher revenues. While negative revisions to Q2 estimates have stabilized in recent weeks, estimates for the period have been under significant pressure relative to other recent periods since the June-quarter got underway.

Q2 earnings estimates for 13 of the 16 Zacks sectors have come down since the quarter got underway, with Aerospace, Utilities, and Consumer Discretionary as the only sectors whose estimates have modestly moved higher since the start of April.

Q2 earnings estimates for the Tech and Finance sectors, the two largest contributors to aggregate S&P 500 earnings, accounting for 51% of all index earnings, have also been cut since the quarter got underway. The quarter started with significant pressure on Tech sector estimates, but the negative revisions trend notably stabilized in the subsequent weeks.

In terms of year-over-year growth, three sectors are expected to enjoy double-digit earnings growth in Q2: Aerospace (+15.1%), Tech (+11.8%), and Consumer Discretionary (+105.6%). On the negative side, seven sectors are expected to earn less in Q2 relative to the year-earlier period, with double-digit declines at the Energy (-24.9%), Construction (-14.4%), and Autos (-30.2%) sectors.

The Q2 earnings season will really get going once JPMorgan, Bank of America, and Wells Fargokick-off the June-quarter reporting cycle for the Finance sector.

Making sense of earnings expectations for 2025 Q2 and beyond

The start of Q2 coincided with heightened tariff uncertainty following the punitive April 2nd tariff announcements. While the onset of the announced levies was eventually delayed by three months, the issue has understandably weighed heavily on estimates for the current and upcoming quarters, particularly in the first few weeks following the April 2nd announcement.

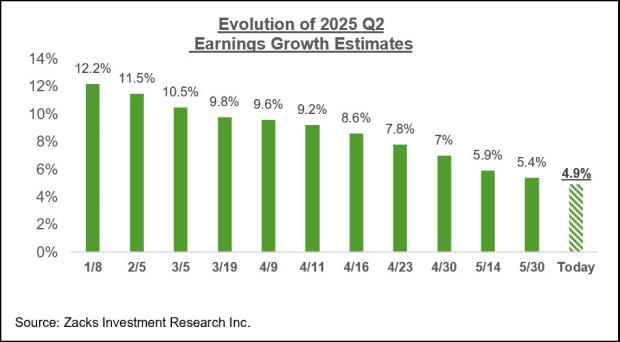

The expectation at present is for Q2 earnings for the S&P 500 index to increase by +4.9% from the same period last year on +3.9% higher revenues. The chart below shows how Q2 earnings growth expectations have evolved since the start of the year.

Image Source: Zacks Investment Research

While it is not unusual for estimates to be adjusted lower, the magnitude and breadth of Q2 estimate cuts are greater than we have seen in the comparable periods of other recent quarters.

Since the start of the quarter, estimates have come down for 13 of the 16 Zacks sectors, with the biggest declines for the Transportation, Autos, Energy, Construction, and Basic Materials sectors. The only sectors experiencing favorable revisions in this period are Aerospace, Utilities, and Consumer Discretionary.

Estimates for the two largest earnings contributors to the index – Tech & Finance – have also declined since the quarter began.

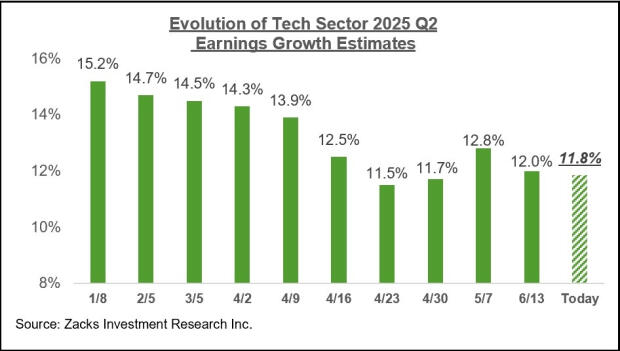

Tech sector earnings are expected to be up +11.8% in Q2 on +10.8% higher revenues. While these earnings growth expectations are materially below where they stood at the start of April, the revisions trend appears to have notably stabilized lately, as we have been flagging in recent weeks. You can see this in the sector’s revisions trend in the chart below.

Image Source: Zacks Investment Research

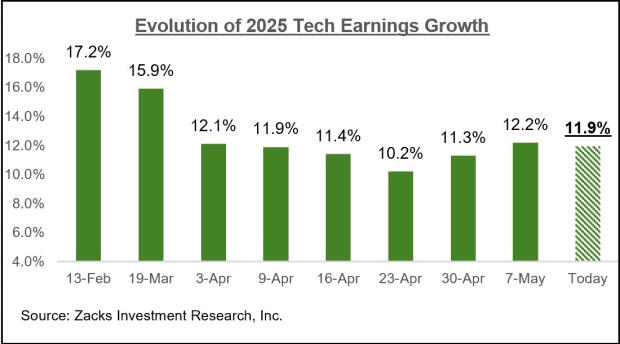

This stabilizing turn in the Tech sector’s revisions trend can be seen in expectations for full-year 2025 as well, as the chart below shows.

Image Source: Zacks Investment Research

The two charts above show that estimates for the Tech sector have stabilized and are no longer under the type of downward pressure experienced earlier in the quarter. The Tech sector is much more than just any other sector, as it alone accounts for almost a third of all S&P 500 earnings.

The earnings big picture

The chart below shows expectations for 2025 Q2 in terms of what was achieved in the preceding four periods and what is currently expected for the next three quarters.

Image Source: Zacks Investment Research

The chart below shows the overall earnings picture for the S&P 500 index on an annual basis.

Image Source: Zacks Investment Research

While estimates for this year have been under pressure lately, there haven’t been a lot of changes to estimates for the next two years at this stage.

Stocks have recouped their tariff-centric losses, although the issue has only been deferred for now. While some of the more dire economic projections have eased lately, there is still plenty of macro uncertainty that will likely continue to weigh on earnings estimates in the days ahead, particularly as we gain visibility on the tariffs question.

Want the latest recommendations from Zacks Investment Research? Download 7 Best Stocks for the Next 30 Days. Click to get this free report

Want the latest recommendations from Zacks Investment Research? Download 7 Best Stocks for the Next 30 Days. Click to get this free report

Author

Zacks

Zacks Investment Research

Zacks Investment Research provides unbiased investment research and tools to help individuals and institutional investors make confident investing decisions.