As markets eagerly await Friday's release of the latest Personal Consumption Expenditures (PCE) Price Index figure, the US Federal Reserve's (Fed) preferred indicator for gauging inflation, investors know that this report will weigh heavily in September's interest rate decision.

But why is this figure, less well known than the Consumer Price Index (CPI), so central to US monetary policy?

PCE vs CPI: Two measures, two rationales

For most Americans, and even international observers, inflation is measured by the CPI.

The CPI, published by the Bureau of Labor Statistics, measures changes in the prices of a fixed basket of goods and services that represent urban household spending.

It's the most widely publicized inflation measure, and the one that hits the headlines when talking about the price of rent, food or gasoline.

The PCE, on the other hand, is less well known to the general public, but is preferred by the Fed.

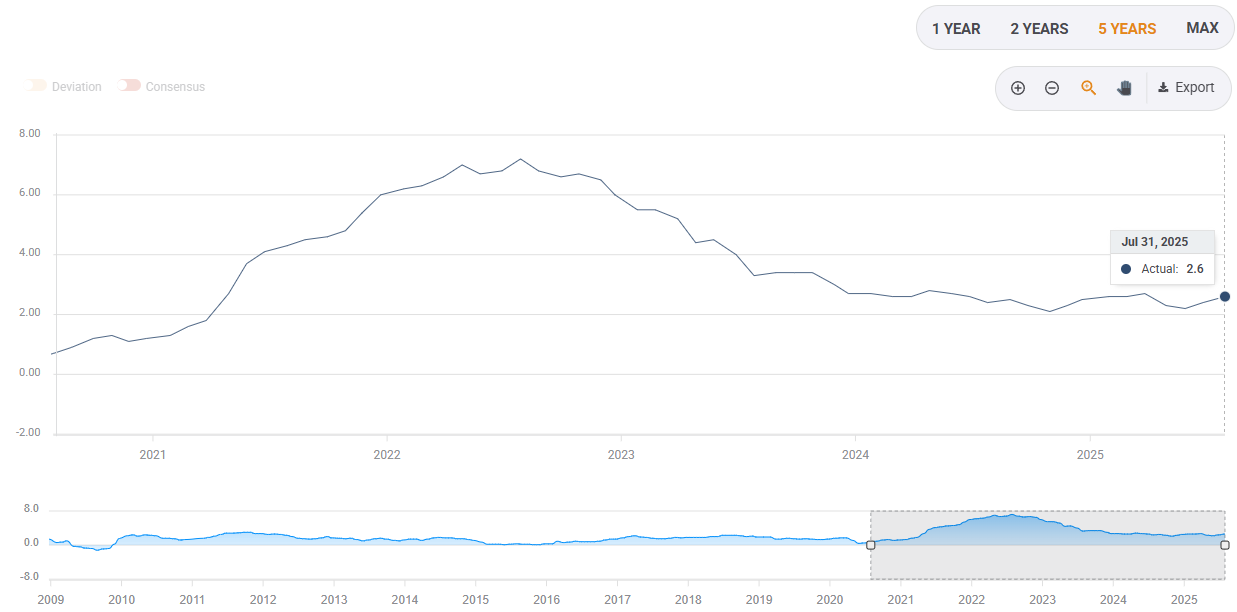

Personal Consumption Expenditures. Source: FXStreet

Calculated by the Bureau of Economic Analysis, it covers a broader field. Not only expenses paid directly by households, but also those paid on their behalf, such as healthcare financed by employers or public programs.

Its more flexible methodology better incorporates changes in consumer behavior. For example, switching from beef to chicken if red meat prices soar. In other words, the PCE more accurately reflects the reality of American consumption.

Finally, the PCE is adjusted to consumer habits or changes more frequently and draws on a wider range of administrative sources, making it a more accurate and stable barometer than the CPI.

It is for these reasons that, since the early 2000s, the Fed has adopted it as its main tool for assessing whether or not inflation is close to its 2% target.

A decisive indicator for the September meeting

Friday's report is of particular importance. It will be the last PCE inflation release before the September 16-17 Federal Open Market Committee (FOMC) meeting.

The analysts' consensus expects headline PCE to have risen by 2.6% year-on-year in July, a pace still above the Fed's target.

More worryingly, the core PCE, which excludes the more volatile food and energy prices, is expected to have accelerated to 2.9%, after 2.8% in June.

Economic calendar. Source: FXStreet.

These figures complicate the Fed's task. On the one hand, keeping key interest rates high, currently in the 4.25% to 4.5% range, would make it possible to contain inflationary pressures fuelled in particular by the US President Donald Trump administration's tariff hikes.

On the other hand, the marked slowdown in the labor market argues in favor of easing policy to support activity.

Powell between inflation and employment

During his speech at the Jackson Hole symposium, Fed Chair Jerome Powell underlined this dilemma: "The labor market appears to be in equilibrium, but it is a curious equilibrium, marked by a joint slowdown in the supply and demand for workers", he declared.

Job creation has slowed sharply to an average of just 35,000 new jobs per month over the past three months, according to the Nonfarm Payrolls report, while statistical revisions have removed hundreds of thousands of previously announced jobs.

This context is prompting the Fed to reconsider the weighting of its dual mandate: price stability and full employment.

After a long-standing focus on inflation, Powell hinted that employment risks could now weigh more heavily on the central bank's decisions.

"If these risks materialize, they can do so quickly, in the form of a sharp rise in layoffs and unemployment," he warned.

A risky bet for the markets

Financial markets are betting heavily on a rate cut as early as September, which would give the economy some breathing space.

However, too rapid monetary policy easing could rekindle inflation at a time when tariffs continue to push up the prices of consumer goods.

In other words, Friday's PCE report could well tip the balance: confirm that inflation remains too high to justify monetary easing, or, on the contrary, allow the Fed to begin a cycle of interest rate cuts.

Either way, the equation is more complex than ever. Chair Powell will have to arbitrate between persistent inflation and an increasingly fragile labor market.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

If not otherwise explicitly mentioned in the body of the article, at the time of writing, the author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice.

Recommended content

Editors’ Picks

USD/JPY extends recovery toward 158.00 despite intervention risks

USD/JPY extends its recovery toward 158.00 in the Asian session on Tuesday. However, buyers remain wary amid further intervention risks. A joint US-Japan FX intervention on Friday and hints of further action continue to underpin the Japanese Yen. Furthermore, fresh US-Iran concerns keep the US Dollar's rebound intact, supporting the major.

AUD/USD rises back above 0.7000 after upbeat Australian data

AUD/USD has found fresh buyers, advancing above 0.7000 in the Asian session on Tuesday, following the release of strong Australian Household Spending and ANZ Job Advertisements data. However, further upside could be capped by the slow US Dollar recovery, underpinned by renewed US-Iran tensions and Fed concerns. The focus also remains on the US JOLTS Job Openings data.

stalling the previous day's retracement slide from the highest level since June 17. Receding Fed rate-hike bets cap the overnight US Dollar recovery, which, in turn, supports the currency pair. Traders, however, seem hesitant and opt to wait for further developments surrounding the Middle East crisis amid reports of Iran strikes on a vessel near the Strait of Hormuz.

Gold ranges around $4,050 as Mideast risks and US jobs data loom

Gold trades with caution around $4,050 in the Asian session on Tuesday, even as the US Dollar stalls the overnight bounce from its lowest level since June 17. However, reports of Iran's strikes on a vessel near the Strait of Hormuz keep the geopolitical risk premium in play, supporting the safe-haven buck and keeping the bullion confined within a familiar range ahead of US jobs data.

Morgan Stanley cuts Circle price target to $38 as stablecoin growth stirs concerns

Circle (CRCL) shares came under pressure on Monday after Morgan Stanley downgraded the company to underweight and sharply cut its price target. Morgan Stanley lowered its price target for Circle to $38 from $106, citing concerns over slower growth in USDC circulation and increasing pressure on the stablecoin issuer's core revenue model.

NFP week: What awaits Bitcoin and Gold BRANDED

This is an NFP week as markets brace for the release of a large influx of job market statistics. The data rollout begins with the JOLTS Job Openings report on Tuesday, continues with the ADP Employment report on Wednesday and Jobless claims on Thursday, and finishes with the Nonfarm Payrolls report on Friday.

WTI remains well on the defensive below $80.00

Prices of WTI retreat markedly, coming close to the $78.00 mark per barrel, or four-day lows on Monday. The severe pullback follows President Trump’s decision to hold off on another attack against Iran while seeking a deal to reopen the Strait of Hormuz. In addition, a planned OPEC+ output increase adds to the pressure on oil prices.