What drives FOREX prices?

FOREX traders often mistakenly think that their combined actions in the CFD market are determining the way a currency pair moves. It is true that they have an impact however we are trading a derivative ( a product that tracks the price of the underlying security) and to understand what drives our CFD prices we must understand what is driving the price of the underlying security, in this case the exchange rate of currencies.

The actual exchange rate is decided by the market makers who operate as foreign exchange dealers. A dealer accommodates people who want to change one currency into another, usually for the purpose of trade or investment, dealers charge buyers a higher price than they pay sellers making themselves a profit by providing this service.

To understand what drives FOREX prices we need to understand the foreign exchange dealer function, how do they decide prices and what makes them increase or decrease price.

Jack Treynor in his 1987 article "The Economics of the Dealer Function" provided the definitive view of the way money market dealers operate, he gave us the Treynor model which gives a thorough insight into the motivation and actions of dealers.

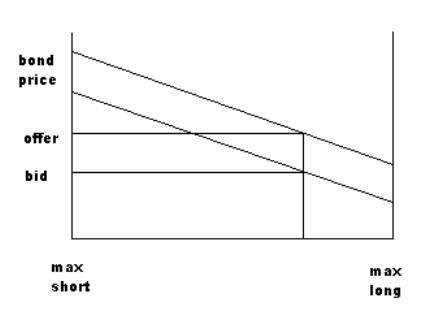

The model shown on the left shows the price of a security on the vertical axis and the exposure of the dealer on the horizontal.

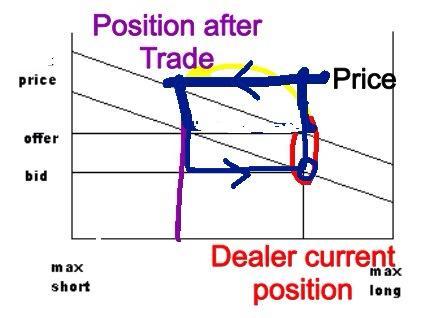

Given a set position for the dealer, in the case highlighted the dealer is currently long the security. The mid point on the horizontal axis would be his flat position. The dealers bid and offer prices are shown, the spread being clear as the difference between these two.

Every time a dealer changes his net position his mean price (average of bid and offer) will change. If a customer who wants to buy a substantial amount of the security the dealer has to decide what price to offer the security at. The trade will alter the net position of the dealer, this new position will change the future price of the security, hence it must affect the current price, indeed the dealers current price must reflect what the price is expected to be in the future if it does not people will be able to make profit simply by trading with the dealer and he will consequently loose money.

As an example of this suppose a trader wishes to buy a substantial number of GBP from the dealer to pay for goods bought in the UK from an exporter. If the current dealer position in GBP is shown in red,(according to the diagram he is net long the GBP) after taking the deal, selling GBP to the customer, he will have less GBP, he may be short GBP, his new position is shown in purple.

To ensure the customer cannot make a profit by undoing the deal he must offer the price that would take effect after the deal. Which is higher than the offer price before the deal. The blue box shows what would happen if the customer sold the GBP back immediately, the dealer would make the spread on both trades and the customer would loose money.

As the size of a dealers position grows they take on more and more price risk, they are not in the business of speculation, they are merely providing a service and taking a profit for doing so. If the orders arrive in a symmetrical fashion, equal buy and sell orders, the dealer will be happy his current position will be flat and he will continue to make the spread.

Often an investor will come to the market who has a view on the asset that is not yet reflected in the price, a series of such investors would result in the dealer holding a large position and getting sand bagged along with the other investors who did not have the new insight. Investors decide if their insight is sufficient to cancel the cost of trading, if not they should not trade.

If the dealer reaches his maximum position he will turn to the dealer of last resort, the central bank, to lay off his position.

The majority of FX dealers do not expose themselves to price risk, they are not speculative dealers. To mitigate the risk the dealer will hedge each position by opening a forward exchange contract. If the value of the security drops it is offset by changes in the forward contract. The price risk has not disappeared it has been transferred to someone else by the forward contract. The forward will often be held by a speculative dealer with a naked long or short position however they may move some of the risk on with more forwards.

The dealer has replaced price risk with liquidity risk as he must now be able to role over the forward contracts as required. Hence the need for liquid markets!

Having discussed the economics of the dealer function which is the main driver of foreign exchange rates we can see that the price that the dealer quotes depends on two distinct things

The volume of buying and selling of a particular currency

The price of the forward contract needed to provide matched book.

High yield on government debt will attract foreign buyers who will have to buy the local currency before they purchase the government bond, this effect is very noticeable at the moment with the euro and some of the more peripheral country bonds offering high yield. Figures of foreign ownership of debt are published by each central bank as is their timetable for issuing new

The forward and the expected spot rate are linked closely to interest rate expectations and hence monetary policy.

Having discussed the dealer function in this way and concentrated on the matched book dealer we have a much better understanding of how changes in the prices of FOREX can be explained.

The actual exchange rate is decided by the market makers who operate as foreign exchange dealers. A dealer accommodates people who want to change one currency into another, usually for the purpose of trade or investment, dealers charge buyers a higher price than they pay sellers making themselves a profit by providing this service.

To understand what drives FOREX prices we need to understand the foreign exchange dealer function, how do they decide prices and what makes them increase or decrease price.

Jack Treynor in his 1987 article "The Economics of the Dealer Function" provided the definitive view of the way money market dealers operate, he gave us the Treynor model which gives a thorough insight into the motivation and actions of dealers.

The model shown on the left shows the price of a security on the vertical axis and the exposure of the dealer on the horizontal.

Given a set position for the dealer, in the case highlighted the dealer is currently long the security. The mid point on the horizontal axis would be his flat position. The dealers bid and offer prices are shown, the spread being clear as the difference between these two.

Every time a dealer changes his net position his mean price (average of bid and offer) will change. If a customer who wants to buy a substantial amount of the security the dealer has to decide what price to offer the security at. The trade will alter the net position of the dealer, this new position will change the future price of the security, hence it must affect the current price, indeed the dealers current price must reflect what the price is expected to be in the future if it does not people will be able to make profit simply by trading with the dealer and he will consequently loose money.

As an example of this suppose a trader wishes to buy a substantial number of GBP from the dealer to pay for goods bought in the UK from an exporter. If the current dealer position in GBP is shown in red,(according to the diagram he is net long the GBP) after taking the deal, selling GBP to the customer, he will have less GBP, he may be short GBP, his new position is shown in purple.

To ensure the customer cannot make a profit by undoing the deal he must offer the price that would take effect after the deal. Which is higher than the offer price before the deal. The blue box shows what would happen if the customer sold the GBP back immediately, the dealer would make the spread on both trades and the customer would loose money.

As the size of a dealers position grows they take on more and more price risk, they are not in the business of speculation, they are merely providing a service and taking a profit for doing so. If the orders arrive in a symmetrical fashion, equal buy and sell orders, the dealer will be happy his current position will be flat and he will continue to make the spread.

Often an investor will come to the market who has a view on the asset that is not yet reflected in the price, a series of such investors would result in the dealer holding a large position and getting sand bagged along with the other investors who did not have the new insight. Investors decide if their insight is sufficient to cancel the cost of trading, if not they should not trade.

If the dealer reaches his maximum position he will turn to the dealer of last resort, the central bank, to lay off his position.

The balanced dealer

In the above discussion which is a simplified view of the dealer function but sufficient for people to get a good understanding of what happens, the dealer will be constantly exposed to price risk for the underlying security. If that were the case they would be speculative dealers making profit from the movement in currency not from providing a service.The majority of FX dealers do not expose themselves to price risk, they are not speculative dealers. To mitigate the risk the dealer will hedge each position by opening a forward exchange contract. If the value of the security drops it is offset by changes in the forward contract. The price risk has not disappeared it has been transferred to someone else by the forward contract. The forward will often be held by a speculative dealer with a naked long or short position however they may move some of the risk on with more forwards.

The dealer has replaced price risk with liquidity risk as he must now be able to role over the forward contracts as required. Hence the need for liquid markets!

Having discussed the economics of the dealer function which is the main driver of foreign exchange rates we can see that the price that the dealer quotes depends on two distinct things

The volume of buying and selling of a particular currency

The price of the forward contract needed to provide matched book.

1. Estimating the physical demand for a currency

We can get a good estimate of this by looking at two things, the trade balance and the volume of government securities being bought by foreigners. There are other reasons to change currency but these are the two major sources of currency exchange. If a currency has a negative trade balance (importing more than it exports) this will put downward pressure on the exchange rate as people are selling the local currency to buy the currency of the exporting country to pay for goods and services.High yield on government debt will attract foreign buyers who will have to buy the local currency before they purchase the government bond, this effect is very noticeable at the moment with the euro and some of the more peripheral country bonds offering high yield. Figures of foreign ownership of debt are published by each central bank as is their timetable for issuing new

2.Estimating the forward price

We must consider two numbers here, the expected price and the forward price, many people believe these two things should be the same(that is the UIP uncovered interest rate parity). If the two numbers were the same it would be impossible for the speculative dealer to make a profit and the balanced book dealer would not be able to hedge his position. The speculative dealer makes money when the forward price is less than the expected spot price, which is proven empirically to be true.The forward and the expected spot rate are linked closely to interest rate expectations and hence monetary policy.

Having discussed the dealer function in this way and concentrated on the matched book dealer we have a much better understanding of how changes in the prices of FOREX can be explained.