Zero interest rate policy: The SNB reopens the door, will the ECB and the Fed follow?

The Swiss National Bank (SNB) struck a blow last week when it cut its key interest rate to 0%, marking a symbolic return to the zero interest rate policy that was thought to be a thing of the past since the post-Covid crisis.

However, this decision, which is highly specific to Switzerland, has rekindled speculation on a key question: could zero or even negative interest rates make a comeback elsewhere, notably at the US Federal Reserve (Fed), the European Central Bank (ECB) or the Bank of England (BoE)?

The SNB faces the trap of deflation and a strong Franc

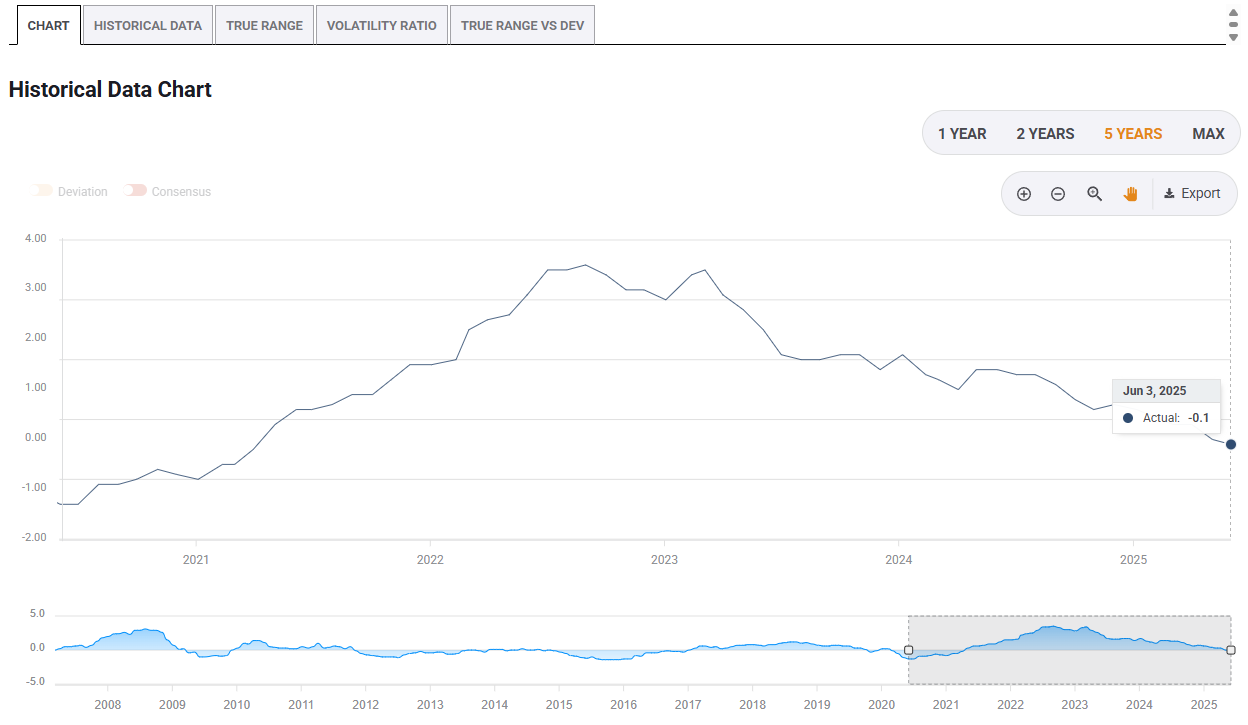

In Switzerland, inflation, as measured by the Consumer Price Index (CPI), turned red in May (-0.1% year-on-year), and the SNB is operating in a very specific context: an ever-stronger Swiss Franc (CHF), fuelled by the global appetite for safe-haven assets in times of uncertainty.

Switzerland Consumer Price Index (YoY) - last 5 years. Source: FXStreet

The trade shock caused by US President Donald Trump's new tariff hikes and tensions in the Middle East have exacerbated this upward pressure on the Swiss currency, threatening both the competitiveness of Swiss exporters and price stability.

USD/CHF price chart. Source: FXStreet

Against this backdrop, cutting interest rates to zero appears to be a defensive measure: to limit the Franc's attractiveness, avoid sinking into deflation, and preserve some room for manoeuvre without plunging back into negative rates too quickly.

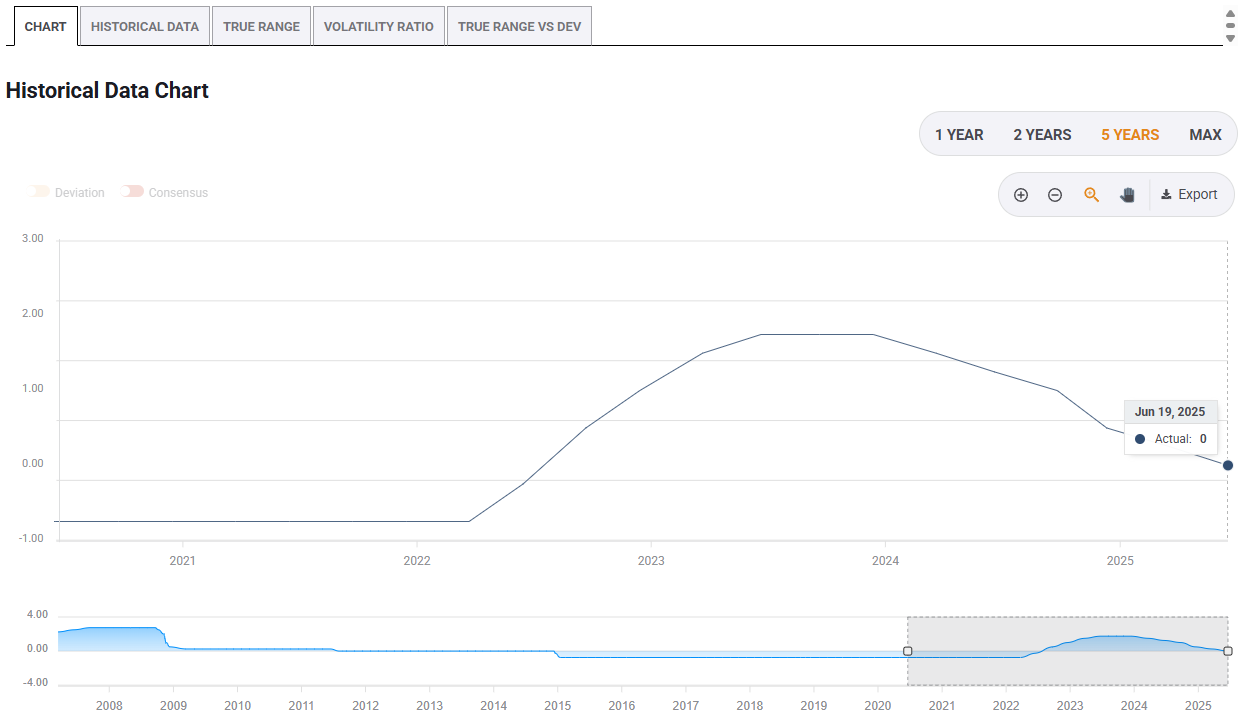

Switzerland SNB interest rate. Source: FXStreet.

But the SNB itself remains cautious. "A return to negative territory is not out of the question, but it is not being considered lightly," said SNB President Martin Schlegel, according to Reuters.

A decade of zero interest rate policy: Powerful but controversial tool

For the record, between the financial crisis of 2008 and the inflationary surge of 2021-2022, zero and sometimes negative interest rates have long been the norm. The ECB, the SNB, the Bank of Japan, Sweden's Riksbank and Denmark's central bank have all tried this unconventional approach, aimed at stimulating demand, combating deflation and bolstering activity.

But these policies have also shown their limits: squeezed bank margins, financial distortions, asset bubbles, and an economic impact often deemed disappointing. The Fed, on the other hand, has never crossed the Rubicon of negative rates, keeping them between 0% and 0.25% in the worst phases (as in 2020), before raising them vigorously as soon as inflation returned.

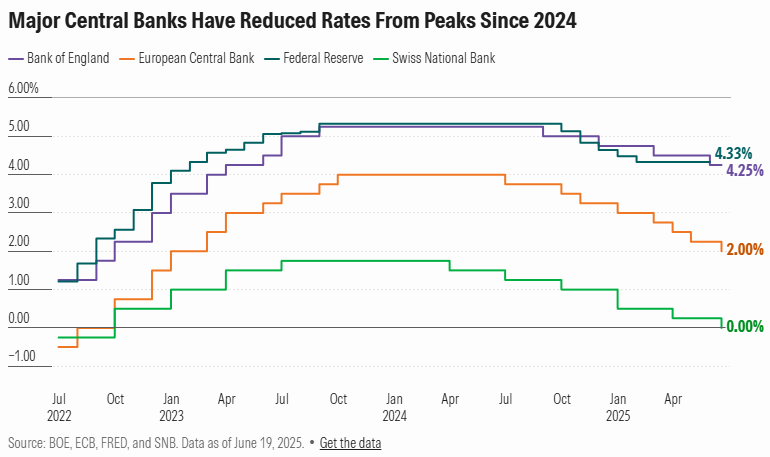

Today, the monetary landscape has changed radically. By mid-2025, the Federal Reserve is holding rates in a range of 4.25% to 4.50%, the Bank of England at 4.25%, and the ECB’s Deposit Facility Rate now at 2%.

These levels reflect both gradual disinflation and the desire of central banks to keep a firm grip on their interest rate policies, in order to preserve room for maneuver in the event of a new shock.

A return to zero interest rates elsewhere? Unlikely, barring a major accident

Interest rate policy in the major economies remains anchored in a logic of normalization, far removed from the emergency levels of the post-crisis period. The prospect of a return to zero interest rates therefore seems unlikely, for several reasons.

Inflation is still too high

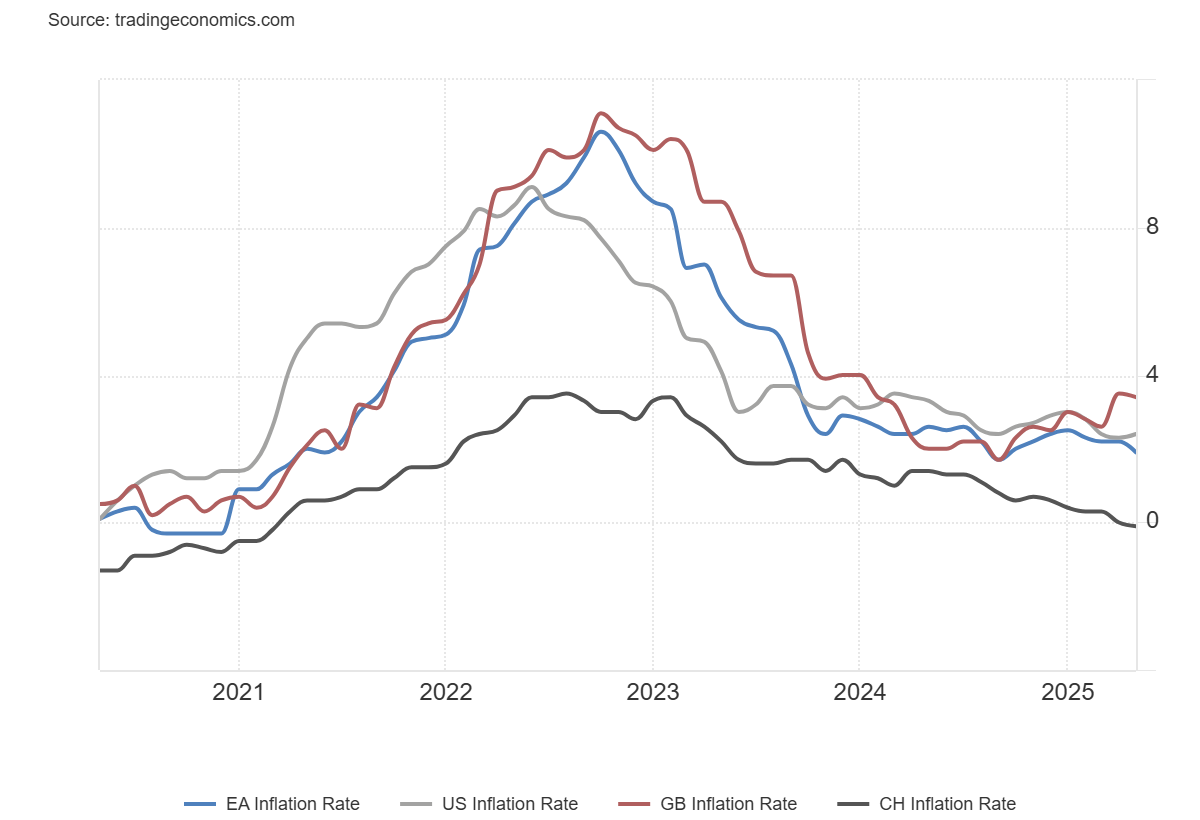

Although disinflation is progressing, not all the major central banks have yet reached equilibrium. In May, annual inflation stood at 1.9% in the eurozone, just below the ECB's 2% target, but the central bank has signaled its intention to pause rate cuts.

On the other hand, inflation is still running at 2.4% in the United States and 3.4% in the UK, levels deemed too high for ultra-accommodative monetary policy.

Against this backdrop, the Fed and BoE are adopting a wait-and-see stance, cautiously adjusting their interest-rate policies in the face of inflation that is still too high. All the more so as inflationary pressure could rise again with the surge in energy prices linked to the Middle East conflict and the potential effects of US tariff hikes.

Geopolitical risk of inflation

With US tariffs, global trade disruptions and the Iran-Israel war fuelling higher energy prices, central banks are more concerned about a resurgence of inflation than a relapse into deflation.

This uncertainty has prompted them to keep rates above zero, even in the event of a slowdown in growth.

Bitter memories of negative interest rate policy

The majority of economists and central bankers now recognize that the experiment with negative rates has had perverse effects. The ambition to make them a lasting tool has been abandoned.

Even in the event of a recession, the temptation will be strong to use other levers, such as fiscal policies, credit targeting or targeted asset purchases.

A Swiss case study, not a global signal

The SNB's decision is fuelling debate, but it remains an isolated case. A return to zero or even negative interest rates is far from being the order of the day in the major economies.

In a world shaken by trade tensions, geopolitical conflicts and more erratic inflation, central banks want above all to preserve their credibility and margins for manoeuvre.

A new cycle of low rates? Perhaps. But a generalized return to zero? That would require a major crisis.

Author

Ghiles Guezout

FXStreet

Ghiles Guezout is a Market Analyst with a strong background in stock market investments, trading, and cryptocurrencies. He combines fundamental and technical analysis skills to identify market opportunities.