Will USDJPY rally last?

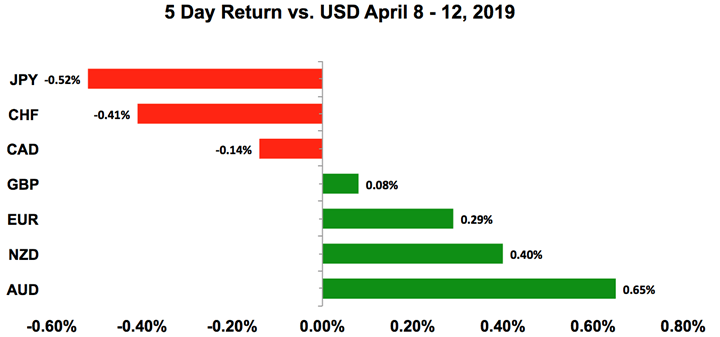

USDJPY climbed to a one-month high last week as euro rose to its best level against the US dollar since the 26th of March. The only times that we see simultaneous strength in pairs like USDJPY and EURUSD is when risk appetite is strong.

Stocks pulled back at the start of last week but they rebounded strongly on Friday to end the week not far from 6-month highs. There's been a lot of talk about recessions, trade tensions between the EU and US are escalating and there's still no final resolution to US-China trade talks or Brexit. And yet investors are optimistic because bank earnings are strong and they believe that policy accommodation abroad will help to mitigate a deep slowdown in global growth. They are also relieved that the Federal Reserve won't add to the pain by tightening again this year. While this may be incredibly optimistic, until all signs point to a significant slowdown in the US that will spill over to the rest of the world, investors see their glasses as half full.

Easter week is always an interesting one in the FX market – we usually see a burst of activity the first three days followed by consolidation. This year may be different because there are a number of important economic reports scheduled for release on Thursday so volatility could extend until then. Nonetheless, most markets are closed for Good Friday and Easter Monday (the US is only closed Friday) so many traders will leave early for their long weekend and look to square up or reduce their positions shortly after the US retail sales report is released.

US DOLLAR

Data Review

-

Factory Orders -0.5% vs. -0.5% Expected

-

CPI MoM 0.4% vs. 0.4% Expected

-

CPI Ex Food & Energy 0.1% vs. 0.2% Expected

-

CPI YoY 1.9% vs. 1.8% Expected

-

CPI Core YoY 2% vs. 2.1% Expected

-

PPI 0.6% vs. 0.3% Expected

-

PPI Ex Food & Energy 0.3% vs. 0.2% Expected

-

Jobless Claims hit 40 year low

-

University of Michigan Sentiment Index 96.9 vs. 98.2 Expected

Data Preview

-

Empire State – Potential upside surprise given the softness of prior report

-

Trade Balance – Upside risk given a stronger manufacturing ISM

-

Retail Sales – Higher gas prices and rise in Redbook Retail sales points to improvement in spending

-

Philadelphia Fed Index – Will have to see how Empire State fares but last month's rebound was very strong, so weaker number likely

-

Housing Starts & Building Permits – Recovery in housing expected after a sharp drop in February

Key Levels

-

Support 111.00

-

Resistance 114.00

USDJPY – 114 or 110?

Treasury yields rebounded last week, squeezing USDJPY higher in the process. US economic reports were stronger than expected with consumer and producer prices ticking upwards. The rise in price pressures was driven mostly by higher food and energy costs, which is not sustainable but when low inflation is one of the main reasons why central bankers are slowing policy normalization, it is good news for the greenback. Jobless claims also fell to a 40-year low. This confirms that the labour market, the strongest part of the US economy is still very tight. More than 190K jobs were created last month and USDJPY's strength reflects the market's hope that job growth will exceed 200K in April. Retail sales are scheduled for release and with gas prices on the rise and job growth rebounding, spending should recover in March after falling in February. This report will not be released until Thursday but when it comes out, it should be positive for USDJPY.

The big question now is whether the trend has completely shifted for USDJPY making 114 more likely to be hit before 110. We are sceptical of the rally because US growth is slowing not accelerating and central bankers are worried. Last week, Vice Chair Clarida said the labour market is healthy and the economy is in a good place but Fed President Bullard thinks the March hike marked the end of policy normalization and favours removing the word "patient" from the policy statement because it suggests a tightening bias. Fed fund futures are pricing in a 48% chance of a rate cut in January so easing is certainty on their minds. Fundamentally USDJPY should see 110 before 114 but technically, USDJPY hit a 7-week high and the positive momentum is strong. The 200-week SMA is at 112 so if the pair breaks this year's high of 112.14, the next stop should be 113.

AUD, NZD, CAD

Data Review

Australia

-

Home Loans 0.8% vs. 0.5% Expected

-

Investment Lending 0.9% vs. -1%

-

Westpac Consumer Confidence Index 100.7 vs. 98.8 Previous

-

Consumer Inflation Expectation 3.9% vs. 4.1% Previous

New Zealand

-

PMI Manufacturing 51.9 vs. 53.7 Previous

-

Card Spending -0.3% vs. 0.5% Expected

Canada

-

Housing Starts 192.5K vs. 196K Expected

-

Building Permits -5.7% vs. 2% Expected

-

New Housing Price Index 0% vs. 0% Expected

Data Preview

Australia

-

RBA Minutes – Likely to be dovish given recent changes in RBA Statement

-

Employment Report – Weaker employment conditions in manufacturing offset by stronger job growth in services

-

Chinese GDP, Industrial Production & Retail Sales – Chinese data is very market moving but hard to handicap

-

Consumer Confidence – Possible improvement given the robustness of retail sales

-

Consumer Inflation Expectations – Likely increase given higher commodity prices & weaker A$

-

Chinese Trade Balance – Likely to remain subdued given US-China trade troubles

New Zealand

-

NZ CPI – Potential upside surprise given stronger food & commodity prices

Canada

-

Trade Balance & Consumer Price Index – Potential upside surprise given stronger IVEY PMI index and softer price growth

-

Retail Sales – Stronger job growth in February and rise in wholesale sales points to stronger spending

Key Levels

-

Support AUD .7100 NZD .6700 CAD 1.3300

-

Resistance AUD .7200 NZD .6800 CAD 1.3400

AUD rally halted by RBA

The best performing currencies last week were the Australian and New Zealand dollars. There wasn't much in the way of data and the reports that were released were more negative than positive for the commodity currencies. Yet none of that mattered as they took their cue from risk appetite. AUD rose to its strongest level in a month despite reports that the country's biggest lender will be cutting 10k jobs. NZD hit a two-month low versus the US dollar on Friday before rebounding strongly to end the week at its weekly range high despite softer manufacturing activity and a decline in credit card spending. Better than expected Chinese trade numbers and ongoing reports of progress lent support to these currencies but the chance of further gains is lower than the risk of a deeper pullback because layoffs in Australia and slowdown in manufacturing harden the case for rate cuts. Chinese trade data was also distorted by the Lunar New Year holidays. This week's RBA statement should remind investors that the central bank is not optimistic. Australian labour market figures are also scheduled for release along with Chinese GDP. NZDUSD, on the other hand, should be supported by its CPI report because food and commodity prices rose strongly in the first quarter. AUDNZD is at the cusp of a turn. As for USDCAD, it remained confined in a relatively tight range for most of the week. No major economic reports were released but we learned that housing market activity is slowing. This week's retail sales, inflation and trade reports should breathe new life into the loonie and hopefully take the pair out of its consolidative range. These reports take on increased importance because the Bank of Canada is dovish but oil prices are on the rise, giving investors very little direction.

BRITISH POUND

Data Review

-

PMI Manufacturing 55.1 vs. 52.1 Expected

-

PMI Services 48.9 vs. 50.9 Expected

-

PMI Construction 49.7 vs. 49.8 Expected

-

PMI Composite 50 vs. 51 Expected

-

Halifax House Prices vs. -2.8% Expected

Data Preview

-

Trade Balance & Industrial Production – Potential upside surprise given rise in manufacturing activity

Key Levels

-

Support 1.2800

-

Resistance 1.3300

UK gets six more months

One of the biggest stories in the FX market last week was the European Union's decision to extend Britain's exit from the European Union by 6 months to the 31st of October. This was longer than the Prime Minister requested and shorter than the one year option some EU members preferred. There will be a formal review in June and if the UK wanted to leave sooner, it could. As a result, the UK will be participating in the European Parliamentary elections unless it reaches an agreement internally to leave the EU before June 1st. The good news is that this extension averted a no deal Brexit last week that would have caused major disruptions in the financial markets. It also provides six months of relief for UK businesses who were looking at the loaded end of a gun if the UK would have had to suddenly exit out of EU within days. The bad news is that while the agreement brings much-needed respite, the market reaction was less than stellar as Brexit fatigue and lack of clear outcomes have clearly taken their toll on traders. The EU refuses to renegotiate the Withdrawal Agreement and the fear is that Prime Minister May still won't receive the support she needs to pass the current Withdrawal Agreement in 6 months time. After all, is said and done UK still faces the same three choices - a hard Brexit under WTO rules, a possible 2nd referendum that could overturn Article 50 or some sort of a customs union that would leave the issue of the Irish border unresolved. Cable held steady under the 1.3100 figure but showed little sign of life. Finally, the six-month delay could prove to be positive for the UK economy as it may provide a boost in spending from a more confident UK consumer. Regardless of pick up in data, the BOE is likely to remain stationary erring on the side of caution as the risks of hard Brexit remain and this should keep a cap on cable unless some genuine political breakthrough is achieved.

In the near term, this 6-month relief allows investors to turn their focus back to data. The latest economic reports were mixed with manufacturing activity slowing and service sector activity accelerating. This week's inflation, employment and retail sales reports will provide a better look at how much of a toll Brexit uncertainty has had on the economy.

EURO

Data Review

-

ECB Leaves Rates Unchanged, Dovish Bias

-

German Trade Balance 17.9B vs. 16B Expected

-

German Current Account Balance 16.2B vs. 19B

-

Expected EZ Industrial Production -0.2% vs. -0.5% Expected

Data Preview

-

EZ and German ZEW Survey – Potential upside surprise as a rise in DAX and low yields could boost sentiment

-

EZ Current Account – Potential downside surprise given the drop in German and French balances

-

EZ Trade Balance – Potential upside surprise given a stronger German and French trade

-

EZ & GE PMIs – Tough call as ECB is dovish but sentiment is up

Key Levels

-

Support1.1200

-

Resistance 1.1400

Fade the Euro Rally

EURUSD rose above 1.13 last week for the first time since March 26 but the rally should be faded. Data was better than expected with the German trade surplus growing and industrial production falling less but these reports are not enough to be optimistic about the euro. Trade tensions between the European Union and the US are at a boiling point with President Trump threatening $11B in tariffs over Airbus subsidies. In response, the EU is preparing its own list of retaliatory tariffs worth over $22B. The World Trade Organization hasn't officially recommended a penalty for the EU but if they do or the US pushes ahead with the tariffs, it will be very damaging to the region's economy and the euro. This is a risk that the central bank is fully aware of. So much that ECB President Mario Draghi expressed concerns about the slowdown in the economy and teased investors about the possibility of more stimulus during his post ECB meeting presser. He said TLTRO 3 was their first defence to slowing growth and if the weakness deepens, they have "plenty of instruments" at their disposal. In June, they'll also decide if negative interest rates need mitigating but for now, Draghi made it clear that there are many things keeping them up at night from tariffs to Brexit, protectionism, low inflation and the possibility of a recession in Italy. So not only do they feel that rate hikes are unnecessary this year but they could delay them further if needed. In June, they'll announce the details of TLTRO and the program could be more extensive if the slowdown deepens. The German ZEW survey and Eurozone PMIs are scheduled for release this week and if the data softens, reinforcing the central bank's concerns, EURUSD will resume its slide. Ultimately, we expect the pair to test 1.10.

Author

Kathy Lien

BKTraders and Prop Traders Edge