What will the Fed say about the oil problem?

Outlook:

The attack on the Saudi oil facilities is a big deal and could lead to war. A few things: the Houthi rebels are a ragtag bunch who would be fighting with pitchforks if they didn’t have supplies and weapons from Iran. That this attack was done with drones—drones!—is proof positive that somebody else is behind it. These people do not have running water or consistent electricity, let alone the education and infrastructure to produce advanced weapons. But any 8-year old can operate a drone (or an AK 47, if to comes to that). Iran denies it, of course.

Trump is not only a coward, but also loathe to be responsible for yet another war, something he criticized other presidents for starting without having a clear picture of what victory would look like. He promised to end wars in the Middle East and Afghanistan, and that was a popular stance, while hypocritically boosting spending on the military and enjoying boasting about US military capability (“my bombs are bigger than Kim’s,” for example).

Because of the character of the president, we think (so far) that Trump will avoid going to war. It would take an open, public, full-throated request from the Saudis for him to change his mind, and even then he might offer only a smallish bequest—bombing Yemen, say. It’s not a little weird that the only people who know for sure what happened and who did it are the Israelis. To some extent, a US policy of restraint could be the product of Israeli interests. If the US were to start a war with Iran, the first casualty would be Israel—and everyone knows it. The first call Trump took over the weekend was from Bibi. Fortunately for the US, Netanyahu is really smart and really tricky. We’d rather have him dictating the US response than the befuddled, personality-disorder addled Trump. What a thing to say!

This is not what the US is saying out loud, of course. The NYT reports Trump in not (so far) naming Iran, saying he has to consult with the Saudis first. “The government released satellite photographs showing what officials said were at least 17 points of impact at several Saudi energy facilities from strikes they said came from the north or northwest. That would be consistent with an attack coming from the direction of the northern Persian Gulf, Iran or Iraq, rather than from Yemen, where the Iranian-backed Houthi militia that claimed responsibility for the strikes operates. Administration officials, in a background briefing for reporters as well as in separate interviews on Sunday, also said a combination of drones and cruise missiles — “both and a lot of them,” as one senior United States official put it — might have been used. That would indicate a degree of scope, precision and sophistication beyond the ability of the Houthi rebels alone.”

There is going to be a lot of to-ing and fro-ing, but if our evaluation of Trump is correct—he really does not want to be a president who starts a war and certainly not one that destroys Israel—this Event can get fixed. That is not to say we won’t get consequences. One of them will be oil producers and their lackey traders playing up the oil “shortage” as much as they can. So far no OPEC country or Russia has said they will increase output to make up for the losses from Saudi Arabia. But before this Event, there were worries about a glut. If the Saudis restore facilities in short order—and Aramco really is an efficient company—the oil price problem could go away faster than the doom-sayers are now predicting.

Anytime the US goes to war, or escalates war, the dollar goes up on the uncertainty effect. A prolonged rise in the price of oil also makes everyone nervy, including the Fed, although they pretend that because they can’t do anything about it, the price of oil is not a factor in decision-making. Bilge. Oil is the single most critical component in any inflation forecast for the simple reason that it has a long and winding reach. Pretending oil is not an inflation factor is the Fed’s own moral hazard curse.

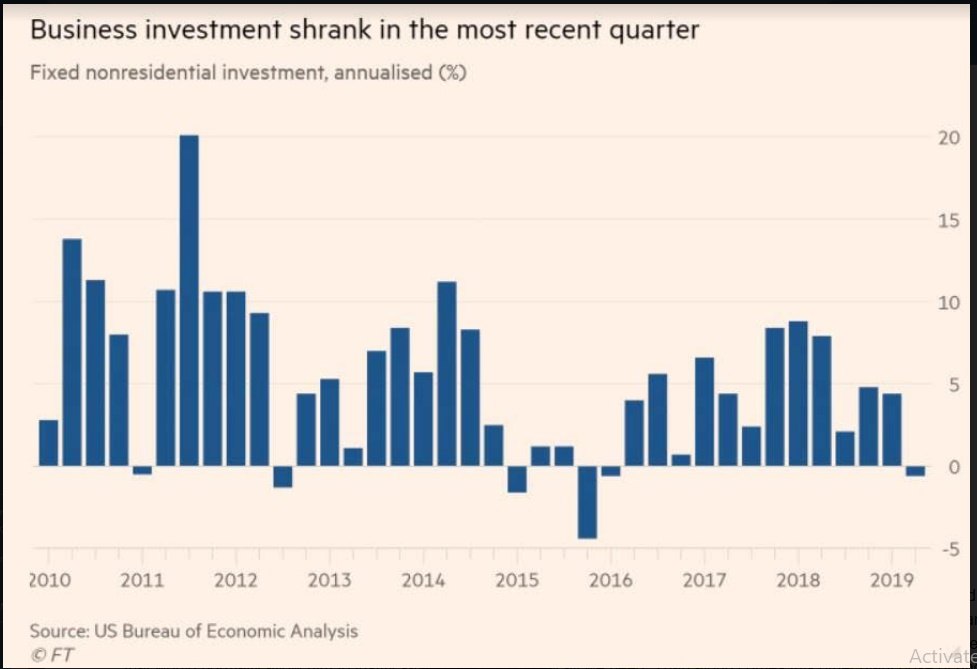

And the Fed meets this week to deliver the first rate cut. What will the Fed say about the oil problem? Because it’s so new, the Fed can get away with saying very little, and saying it cautiously. The FT notes that fixed non-residential investment, aka capex, is already on the downswing. This is where the first round of uncertainty took us, so we approve of this approach (!). Here is the latest chart:

The FT notes that economists are very uncertain about whether uncertainty affects capex, but that doesn’t mean the Fed is not already responding to the uncertainty created by Trump and by the trade war. Notice there are two things there—not just the trade war, but an erratic captain at the helm. You have to feel sorry for Mr. Powell. First he gets strong retail sales and a decent inflation report—3.4% in the latest 3-month period, data that would normally allow him to justify saying one cut is likely all we need. Than along comes this other giant dose of uncertainty, which may imply more cuts and even zero or negative rates. Either way, rising uncertainty favors the dollar. It seemingly favors the dollar even over other oil producers like Canada and Mexico. Nobody ever said the FX market was entirely rational.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a free trial, please write to [email protected] and you will be added to the mailing list..

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat