We must blame the bond markets

Outlook

In the US, today we get the JOLTS report that will likely show job opening lower than before, but it’s not a market-mover. Tomorrow’s ADP private sector jobs is more important, and expected to show a slowdown to 80,000 from 104,000 in July. Remember that ADP adjusts its forecasts on the Wednesday to match the total payrolls on the Friday.

Bloomberg now has NFP at 75,000 and a rise in the unemployment rate from 4.2% to 4.3%, which is the grand scheme of things is not all that high but will frighten the horses.

Note again that it wasn’t dollar buying yesterday that was the shocker. The big move came at 2-3 am New York time overnight Monday into Tuesday, which is 8-9 am in Europe and a little later in some places. It was selling of pounds (budget) and euros (French political turmoil) that led the way. Others tagged along, keeping the crosses in fair order. The driver was a giant rise in yields in the UK, Germany, France, and Italy, so we must blame the bond markets.

The WSJ notes that yesterday, the too-big pile of debt in the UK triggered a yield jump when the Treasury sold “£14 billion of 10-year gilts at around 4.88%, the highest yield since 2008. As politicians borrow more to fund current expenditure, they must do so at higher interest rates.

“Ditto the existing pile of debt, which must be rolled over from time to time. This is one reason the U.S. Treasury under Secretary Scott Bessent is issuing more lower-rate, short-term bills. It’s becoming normal for debt-service costs to exceed defense budgets.

“A one-day bond selloff isn’t cause for panic, and for the most part Tuesday’s isn’t. But politicians’ enthusiasm for debt-fueled spending could one day transform a routine down day in the bond market into a fiscal crisis. Be grateful that we’re probably not there—yet.”

Bloomberg concurs. In the US, the 30-year rose yesterday to 4.999%, as close to 5% as you can get, before falling back. This means investors want their inflation premium. But at the same time the 2-year fell back, an unusual development named a bear steepener. This is defined as investors selling longer tenors when there is high inflation expectations or a surge in government spending, or both. It’s a negative signal for the economy.

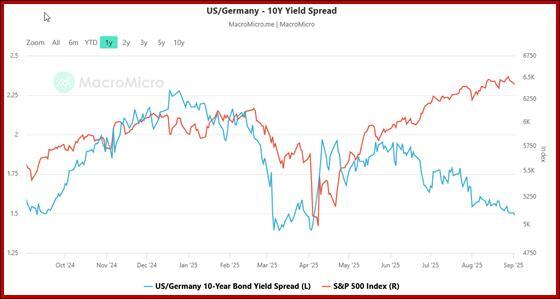

We have noted before that the yield/dollar correlation is one of the better ones. See the Chart Package. Also, below is the US-Germany yield diff, showing a steep fall since he beginning of June. This site adds the S&P, which has continued to rise despite the drop in the differential. Somebody is sure to say this foretells a stock market correction—but the S&P has been rising for ten years come hell or high water, so probably not.

The longer-term rate outlook from ECR Research is a bit scary. It expects German 10-year yields to stay above 2.45% and then proceed higher towards 5%.

The Fed will cut rates this month while the 10-year trends towards a range of 4-4.5% and then “to rise towards 5% or higher later this year.

“In Britain, we expect the Bank of England to cut rates once, at most twice, this year. On balance, we expect British 10-year yields to rise towards 5.25% or higher over the coming quarters.”

To make things more simple than they should be, probably, everyone is going to get a 10-year at 5%.

It’s a lot more complicated than that, of course. To see the full report, request a free trial at https://ecrresearch.com/trial/request.

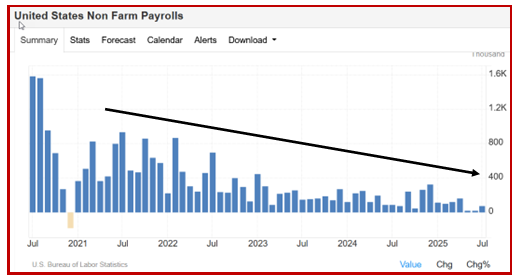

About payrolls: the chart is on the last page all week to keep us grounded. It seems all too likely the number will be bad, meaning less than the 130,000 SocGen’s Juckes says is needed to keep GDP on track. The consensus is 75,000 and we have seen 38,000. Adding to the ordinary economics is the question of whether we can trust the numbers now that Trump owns he BLS. If there is one thing we know about this guy, he lies. He lies a lot. He lies several times a day.

Forecast

As we wrote yesterday, the Treasury yields have the power to offset the bad Trump karma. During the US day, we had a bounceback that was especially big in the Swiss franc in the US morning, so indicating a flash-in-the-pan. It’s a little interesting that the dollar/yuan is a gravestone doji. Unless something else happens today, the flash-in-the-pan is likely very short-lived, so if you got long dollars, get out. Except for sterling. There the story is still developing.

Tidbit: The NY Fed published its “multivariate core trend” for July. It fell to 2.7% from 2.8% with a band of 2.3-3.1%. Services ex-housing and core goods fell while the housing contribution was low at 0.02%.

Now think back to the Richmond Fed survey of businesses raising price that we copied and pasted only yesterday. Which one do you believe? Consider that the NY Fed is dealing with July while the Richmond Fed is more up to date and also contains a forecast into Q4 and 2026.

No wonder the public is confused. If they are not, they should be.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat