USD/JPY Weekly Forecast: Poised to advance

- USD/JPY retreats below 105, finds support at 104.55, recovers.

- Chairman Powell: The US labor market remains weak.

- Chairman Powell: Fed has no plans for rate increases or bond program reductions.

- US Treasury rates move higher after Wednesday low.

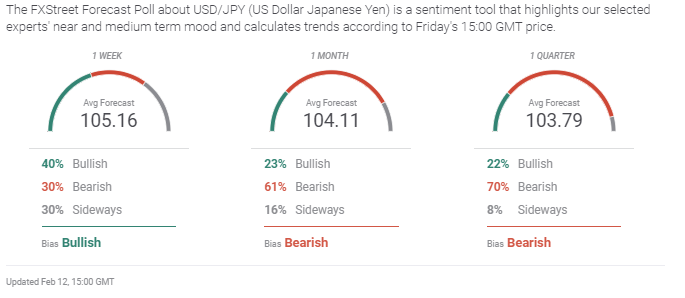

- FXStreet Forecast Poll sees no immediate increase in USD/JPY.

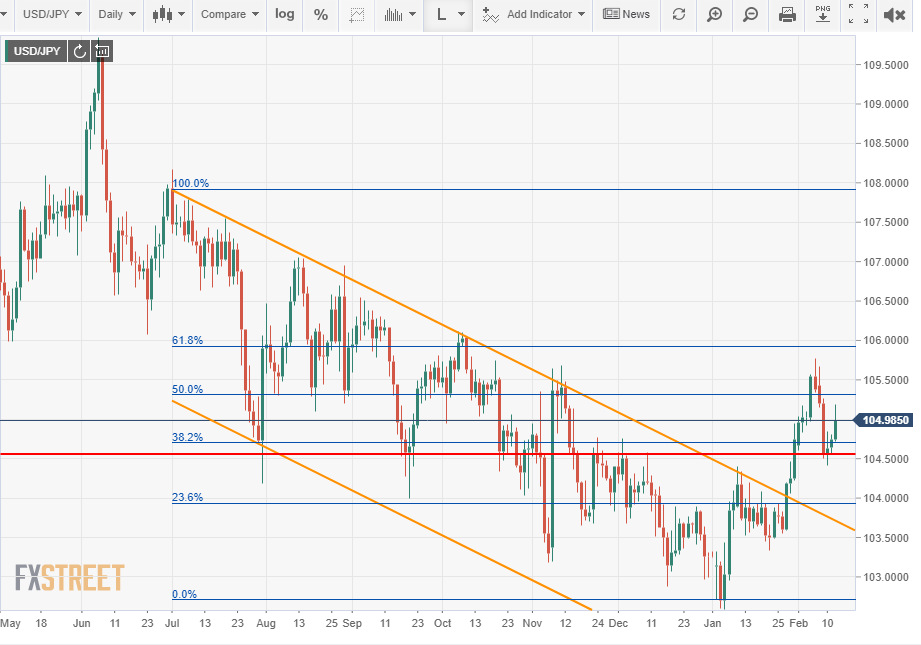

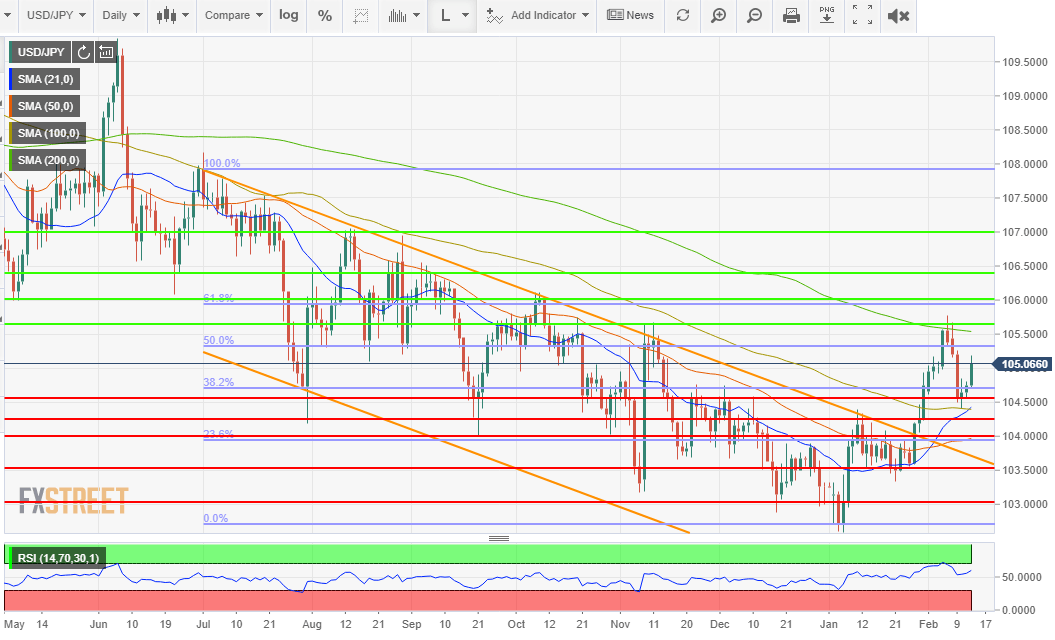

The USD/JPY reneged on its breakout promise this week dropping below 105 on Tuesday but support at 104.55 held on Thursday. The descending channel is increasingly distant and a declining a draw with the upper border below 103. Movement in the pair is tied to improvement in the US economy and Treasury rates.

It was a drop in those Treasury rates mid-week that helped undermine the USD/JPY. After last Friday's close in the 10-year bond at 1.1700, the highest finish since March 18, yields dipped to 1.157 on Tuesday and 1.1330 on Wednesday.

The yield on this benchmark bond, the reference for many commercial rates, had executed a sharp 16 basis point increase in the seven sessions from the close on January 27 at 1.014% and profit-taking rather than a change of circumstances was the likely cause of the swoon to Wednesday. Rates reversed on Thursday climbing back to 1.1650% which helped stabilize the USD/JPYand reaching 1.198% on Friday at 2:28 pm EST.

US 10-year Treasury yield

CNBC

The US stimulus package working its way through Congress has been one source of dollar strength on the assumption that whatever its final composition and amount it will lard consumer spending which was dismal in the fourth quarter. Its delay may be adding some weight to the USD/JPY. Even though January Nonfarm Payrolls were as forecast at 49,000, the much stronger ADP report and the continuing strength of the Purchasing Managers' Indexes had given a lift to late expectations for a better jobs report.

There has also been a minor revival of inflation concerns even though there is no evidence of such and Federal Reserve Chairman Jerome Powell has discounted it. The repetitive size of the US budget deficits over the past five years and money creation by the government is a classic precursor to inflation.

Japanese data was of no trading import and if the slightly better-than-expected PPI rate in January was positive news, Labor Cash Earnings for December fell more than twice as much as forecast.

In the US Fed Chairman Powell's comments in a speech to the Economic Club of New York on Wednesday that the labor market remains weak and the bank is not considering a rate increase or a reduction in the bond purchase program may have tempered the view to higher Treasury rates. The rise in initial claims and the drop in annual CPI does not augur a quickly reviving economy.

The USD/JPY has gained 2.4% since its low at 102.60 on January 5 and while the channel break late last month provided some technical impetus it is primarily due to a change in fundamental perception.

USD/JPY outlook

The USD/JPY remains dependent on an American economic revival and is intertwined with Treasury rates. Fed bond purchases are intended to prevent a rush higher in Treasury yields and to moderate the end point. They are not designed to freeze interest rates.

The differential between US and Japanese real interest rates is approaching break-even for the dollar and as it becomes positive it adds to the desirability of the dollar side of the USD/JPY.

With the last major lockdown in California ended and viral rates declining fast, expectation is rife in markets for a acceleration in the US recovery.

Technically, the USD/JPY has stayed above the descending channels and a re-entry appears unlikely at the moment but that is conditional on better US data. There is good support at 104.50 backed up by the 21 and 100-day moving averages at 104.40.

There is one caveat in the week ahead, if US January Retail Sales on Wednesday does not return to the plus column the upward motion of the USD/JPY may be hard to sustain.

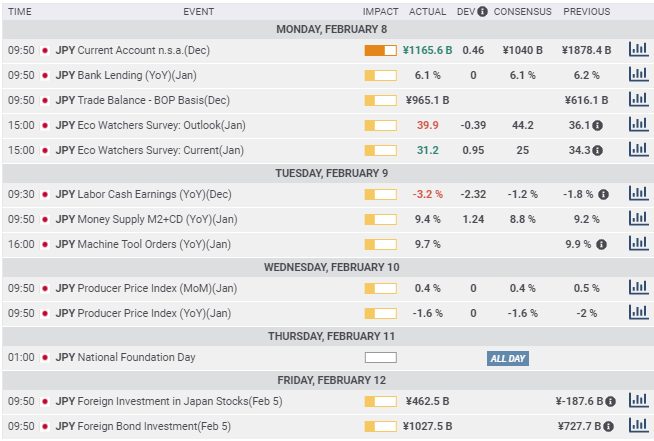

Japan statistics February 8-February 12

None of this week's statistics affected the market. The second monthly rise in the Producer Price Index and the expected slight improvement in the annual figure may give the Bank of Japan some hope on deflation. The nine-month fall in Labor Cash Earnings is a concern for consumer spending.

Monday

The Eco Watchers Surveys Outlook and Current for January split. The Outlook survey at 39.9 was worse than the 44.2 forecast but up from December's 36.1. The Current Survey at 31.2 was better than the 25 estimate but less than the 34.3 December reading. The December surveys were revised down from 37.1 and 35.5 respectively.

Tuesday

Labor Cash Earnings (YoY) fell 3.2% in December more than double the -1.2% forecast and November's revised -1.8% result (initially -2.2%).

Machine Tool Orders rose 9.7% (YoY) in January after the revised 9.9% gain in December, originally 8.7%.

Wednesday

The Producer Price Index (PPI) for January rose 0.4% on the month and fell 1.6% on the year as expected.

FXStreet

US statistics February 8-February 12

In a speech to the Economic Club of New York on Wednesday, Federal Reserve Chairman Jerome Powell was neutral on the state of the US economy and stresssed the need for continuing monetary policy and fiscal support. He said that the job market remained weak though improved from the worst of the recession. He indicated that the central bank isn't considering an increase in the fed funds rate or a reduction in the $120 billion of monthly credit purchases designed to keep interest rates low.

Consistent with the Fed's focus on employment, Mr Powell observed that four million jobless workers have dropped out of the labor force and are not counted in the standard (U-3) unemployment rate at 6.3%. Were these workers included the rate would be close to 10%. He noted that among the highest-earning quarter of the population job loses have been 4%, while layoffs among the bottom quarter were 17%.

The 'Underemployment Rate' (U-6) which counts discouraged and part-time workers was 11.1% in January, the lowest of the pandemic era and down from 11.7% in December. It's peak was 22.8% in April 2020.

Tuesday

Job Openings and Labor Turnover Survey (JOLTS), a measure employment vacancies report from the Bureau of Labor Statistics, registered 6.646 million available posts in December, more thanthte 6.5 million forecast and November's 6.572 million.

Wednesday

The Consumer Price Index in January rose 0.3% as expected, down from 0.4% in December. Annual CPI climbed 1.4% as in December on a 1.5% estimate for January.

Core CPI was flat in January missing the 0.2% prediction, after a 0.1% gain in December. The annual rate was 1.4%, under the 1.5% prediction and December's 1.6% rate. Wholesale Inventories rose 0.3% in December more than the 0.1% estimate and November rate.

Thursday

Initial Jobless Claims were 793,000 in the February 5 week, down from the revised 812,000 prior result, (initially 779,000) but worse than the 757,00 forecast. Claims were 4.545 million in the January 29 week, just over the 4.49 million estimate and lower than the 4.69 million previous week.

Friday

The Michigan Consumer Sentient Index slipped to 76.2 in February from 79 in January. A reading of 80.8 had been forecast.

FXStreet

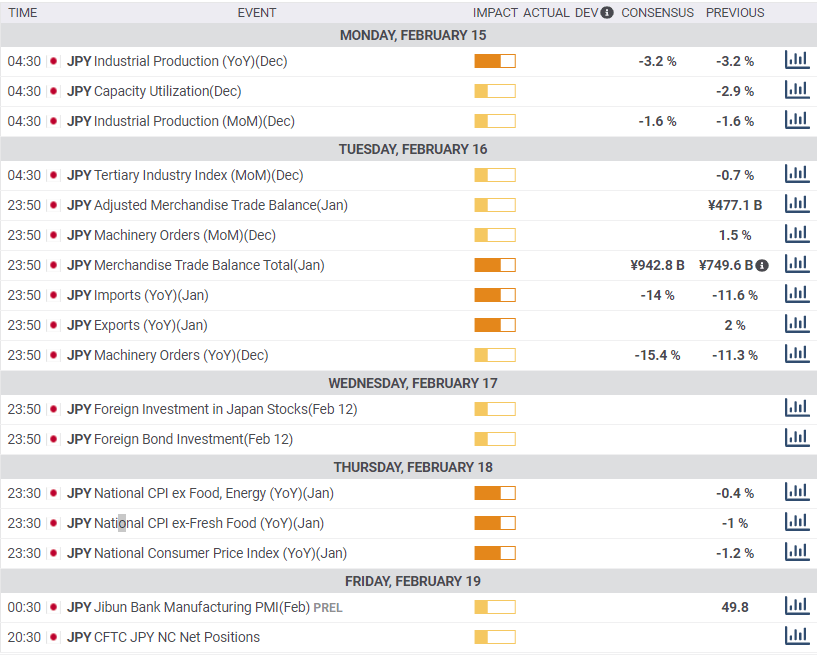

Japan statistics February 15-February 19

Exports, Imports and CPI in January are the most pertinent this week. Trading impact will be small but they are good indicators ffor teh state of the Japanese economy.

Monday

industrial Production is expected to be unchanged in the December revision at -1.6% monthly and -3.2% annually. Capacity Utilization was -2.9% in December.

Tuesday

The Tertiary Index which tracks the domestic service sector was -0.7% in November. Machinery Orders in December are forecast to fall 15.4% on the year after November's 11.3% decline. Imports are predicted to be down 14% annually in January following the 11.6% drop in November. They have fallen for 20 straight months. Exports will rise 1% in January after a 2% rise in December. The Merchandise Trade Balance Total is expected to rise to 942.8 billion yen in January from 749.6 billion in November.

Thursday

The National Consumer Price Index (YoY) should rise to -1.1% in January from -1.2% in December. The National Core CPI ex Food, Energy, should drop 0.2% in January following -0.4% in December.

Friday

Jibun Bank Manufacturing PMI for February is expected to drop to 49.6 in February from 49.8 previous.

FXStreet

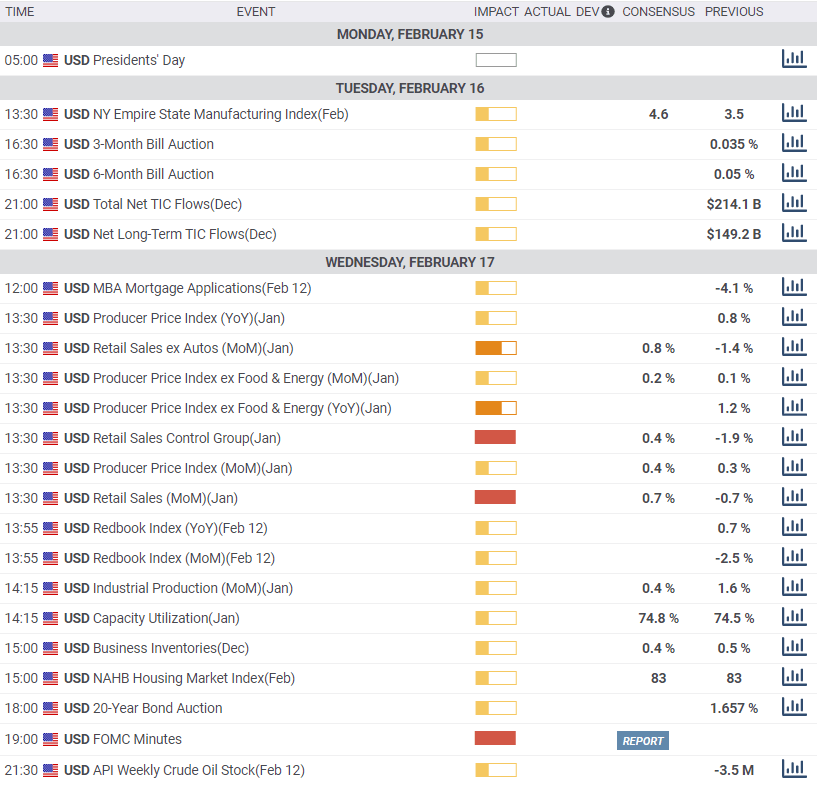

US statistics February 15-February 19

Retail Sales for January predominate. After three unusual negative months markets want to know if the fourth quarter decline in sales has ended now that the California lockdown is over. Variation will translate to the dollar.

Monday

US Holiday President's Day

Wednesday

Retail Sales are expected to rise 0.7% in January after an equivalent negative in December. Retail Sales ex-Autos are forecast to rise 0.8% after falling 1.4% in December. The Retail Sales Control Group is projected to gain 0.4% following the 1.9% plummet I December. The Producer Price Index (PPI) is expected to add 0.4% in January after a 0.3% increase in December. The annual rate rose 0.8% in December. Core PPI is predicted to rise 0.2% in January after 0.1%in December. The annual Core rate was 1.2% in December. Industrial Production is forecast to gain 0.4% in January subsequent to 1.6%in December. Capacity Utilization is forecast to rise ti 74.8% in January from 74.5% prior. The National Association of Home Builders (NAHB) Housing Market Index is anticipated to be unchanged at 83 in February.

Thursday

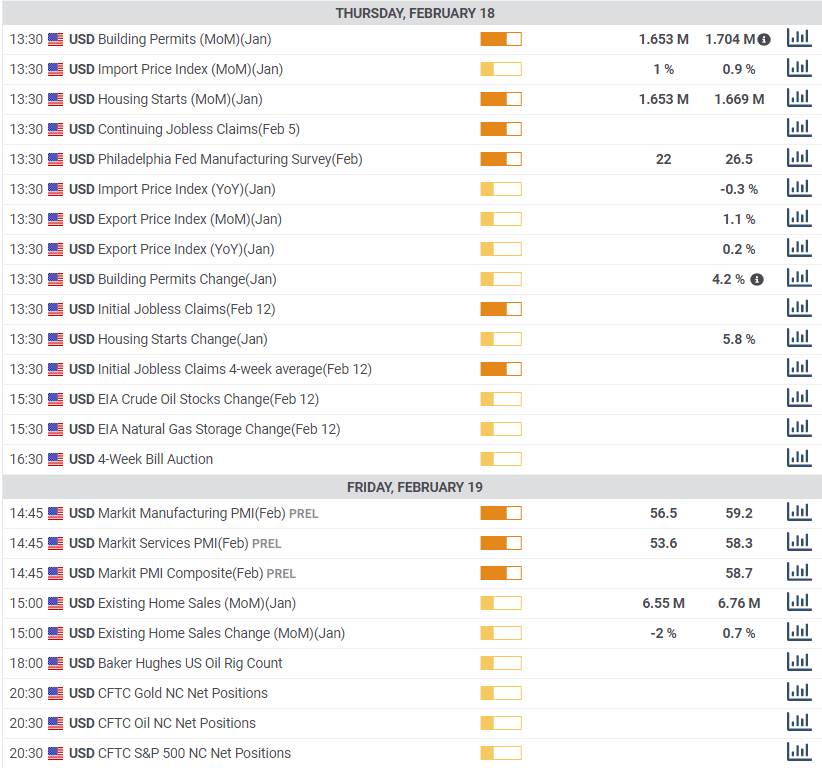

The Philadelphia Fed Manufacturing Survey is expected to drop to 20 in February from 26.5 in January. Initial Jobless Claims are projected to be 775,000 in the February 12 week. Continuing claims are forecast to be 4.575 million in the February 5 week. Housing Starts are expected to rise 0.6% in January to 1.654 million following 5.8% and 1.669 million previous. Building Permits are estimated to be 1.608 million after 1.704 million in December.

Friday

Existing Home Sales are forecast to drop 2.7% in January to 6.56 million annualized after 0.7% and 6.76 million in December. Markit Services PMI for February is projected to drop to 57.5 from 58.3 in January. Markit Manufacturing PMI is expected to fall to 58.5 in February from 59.2.

USD/JPY technical outlook

It is a busy graph this week. The Wednesday rebound at 104.55 supported by the unusual confluence of the 21-day and 100-day moving averages at 104.40 (21-104.43, 100-104.39) and the proximity of the 38.2% Fibonacci at 104.70 gave the USD/JPY a firm technical base. The 50-day moving average at 103.97 is part of the 104.00 support while the 200-day average at 105.54 is coincident with resistance at 105.63. The 50% Fibonacci line, an important milestone in any recovery, lies at 105.31 and having been crossed on the initial surge on February 4 and then re-crossed in decline on Monday may prove more of an obstacle than previous.

Tuesday's sharp drop and subsequent recovery points higher but the numerous resistance lines and the 61.8% Fibonacci at 105.93 will be slow going unless the US economy and Treasury rates show a faster revival.

Resistance: 105.63; 106.00; 106.40; 107.00;

Support: 104.55; 104.25; 104.00; 103.50; 103.00

USD/JPY Forecast Poll

The FXStreet Forecast Poll predicts a negative future for the USD/JPY. Technically, the loss of the 50% Fibonacci level at 105.31, if it stands, jibes with the one week forecast. The one-month and one-quarter views follow that logic lower. Countering that supposition is an improving US economy, on that, the verdict is still out.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.