USD/JPY Weekly Forecast: Before the Fed and after

- USD/JPY and the dollar revive after Fed meeting.

- FOMC and Chair Powell signal March fed funds increase.

- Treasury yields rise as Fed inflation fight comes into focus.

- Japanese inflation weakens, pinning BOJ policy to accomodation.

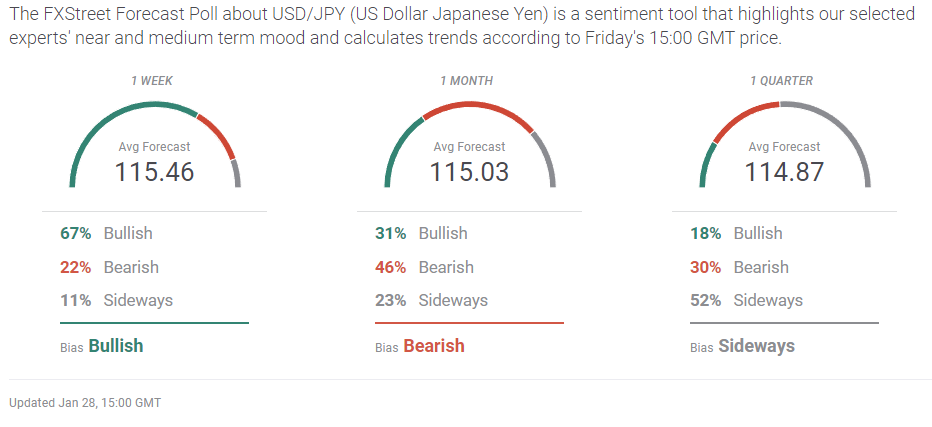

- FXStreet Forecast Poll sees consolidation below 116.00.

The Federal Reserve meeting on Wednesday not only came at mid-week but it split trading into two distinct halves. Before the Fed and Chair Jerome Powell’s press conference Dollar yen had dropped below 114.00 on Friday for the first time since December 21, and closed there for three days running.

After the Federal Open Market Committee (FOMC), 114.00 and 114.50 disappeared and 115.00 vanished on Thursday. The formerly defunct trend line from late September that had been broken conclusively on January 12 and 13, was recrossed at 115.20 on the way to Thursday’s close at 115.36.

Tokyo took the pair to 115.69 on Friday but US PCE inflation deflated the brief surge.

-637789773586110021.png)

“With inflation well above 2 percent and a strong labor market, the Committee expects it will soon be appropriate to raise the target range for the federal funds rate,” said the FOMC statement accompanying the decision to to leave the fed funds rate unchanged at 0.25% and to end the bond purchase program in March, as ordered at the December meeting. The Fed also issued guidelines for reducing its $9 trillion balance sheet.

Fed Chair Jerome Powell’s question and answer commentary beginning 30 minutes later, reinforced and extended the clear intent to begin a rate cycle at the March 16 meeting.

“I think there’s quite a bit of room to raise interest rates without threatening the labor market,” was one of a slew of responses that prompted immediate reactions from traders in the equity, credit and currency markets.

(See our coverage of the Fed meeting: Federal Reserve rate cycle to begin in March, markets reverse on warning, FOMC & Fed Meeting, News & Analysis)

Equities reversed sharply on Wednesday as the Fed’s plans became ever more transparent with Mr.Powell’s remarks.

The S&P 500 and the Dow shed large prior gains, 2.2% and 1.5% respectively to end in negative. The NASDAQ lost its 3.4% improvement finishing up just 2.82 points. Thursday’s trading was volatile, swaying between gains and losses but at the close the Dow was off 0.02%, the S&P 0.54% and the NASDAQ 1.4%.

Treasury returns rose after the Fed meeting, particularly at the short end of the yield curve in the 2-year and 5-year securities. From Monday’s open at 1.016%, the 2-year yield had added 17 basis points to 1.18% just before Friday's open. The 5-year return had climbed 8 points from 1.576% at the start of the week to 1.66%. The 10-year added 6 basis points to 1.83% and the 30-year was just 4 points higher on Thursday at 2.125%..

The dollar was higher in all pairs on Wednesday and the gains continued on Thursday with the euro closing at a 20 month low at 1.1143. The US currency set new 2022 highs against every major competitor on Thursday.

Third quarter Gross Domestic Product for the US, issued on Thursday, was much stronger at 6.9% than the 5.4% forecast.This gave the dollar an additional boost as it suggested the performance of the economy had a better base to start the New Year. Durable Goods were weaker than predicted in December though November’s results were revised markedly higher. Jobless claims fell back from their 13 week peak on January 14, but the four-week average remained at a two-month high. Rising unemployment claims have been carefully watched for signs that the US economy is slowing.

Inflation scored another record for the Personal Consumption Expenditure Price Index (PCE) in December with 4.9% for core and 5.8% for the overall. Personal Income rose 0.3% in December, missing the 0.5% forecast and Personal Spending dropped 0.6% as expected.

Japanese data was limited. Annual Tokyo CPI was slightly less than expected at 0.5% in January, and down from 0.8% in December which had been the highest in 24 months. Core inflation fell to -0.7%, more than twice the -0.3% pace in December.

USD/JPY outlook

The diverging rate policy of the US Federal Reserve and the Bank of Japan (BOJ) remains the fundamental fact motivating traders. The Fed’s aggressive approach to inflation at Wednesday's meeting, especially the extended discussion of the balance sheet reduction, seems to have convinced the credit and currency markets that the governors’ recent conversion to a tighter monetary policy is genuine. By historical levels, there is considerable room for US Treasury rates to rise.

US 2-year Treasury yield

CNBC

The fourth quarter GDP figures provided some assurance that the US economy will continue to grow fast enough to withstand the steady application of higher interest rates.

Mr. Powell’s comment that , “I think there’s quite a bit of room to raise interest rates without threatening the labor market,” brought the point home given the Fed’s protracted attention to the job market over the past two years.

The BOJ will not tighten policy in the near future. If anything, another spending package can be expected from Prime Minister Fumio Kishida's government, a pointless but by now, traditional endeavor for a new leader.

Japanese industrial production for December is expected to decline as is Retail Trade (sales). Consumer Confidence has been down for so long that any positive movement would be notable, none is forecast for January. Recently imposed Omicron restrictions may dampen economic activity in the first quarter.

In the US Nonfarm Payrolls for January and Purchasing Managers Indexes are the main events ahead Job creation is expected to be modest at 200,000, in line with the two previous months. Any improvement would support Treasury rates and the dollar.

Federal Reserve policy is enabled by the growth of the US economy. As long as the major economic indicators, GDP, payrolls, jobless claims and consumption remain stable or improve, the FOMC will follow the inflation deterrence it has publicly charted.

The USD/JPY bias is higher with a return to 115.60 the initial target followed by the four-year high of 116.35 from January 4.

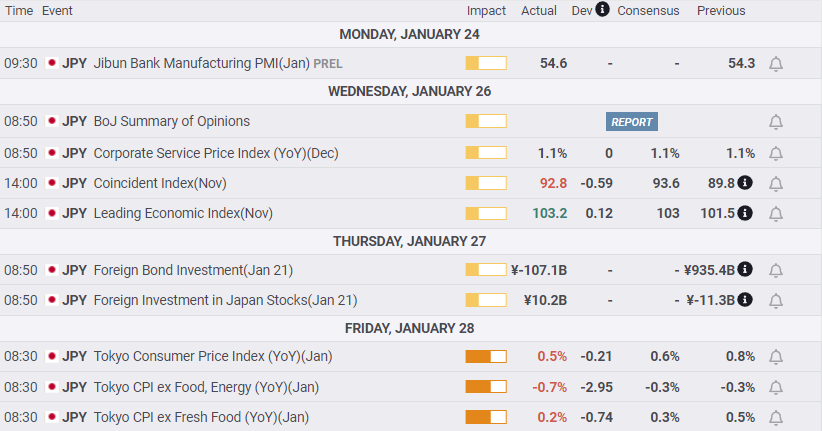

Japan statistics January 24–January 28

FXStreet

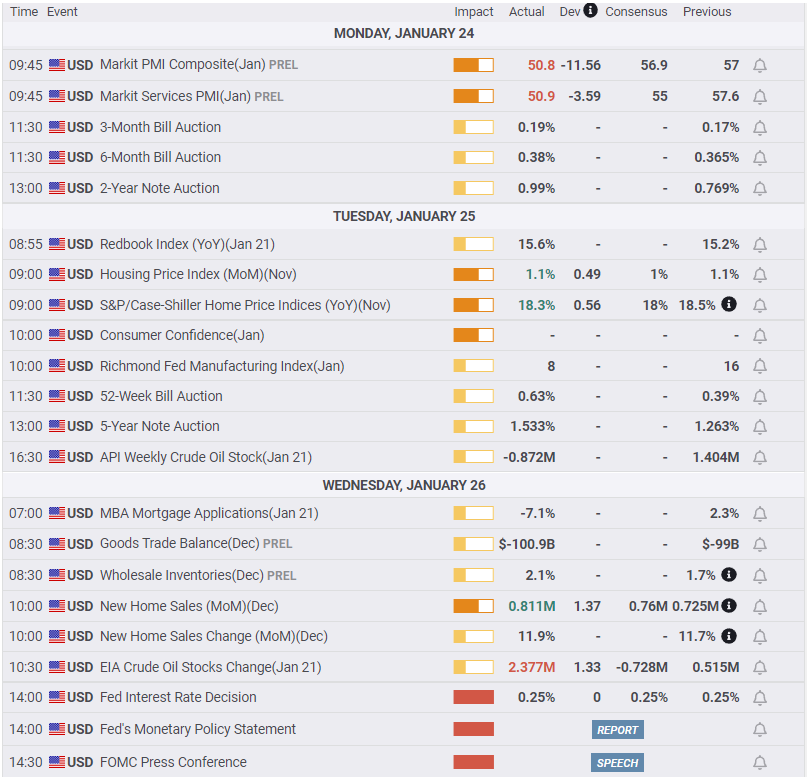

US statistics January 24–January 28

FXStreet

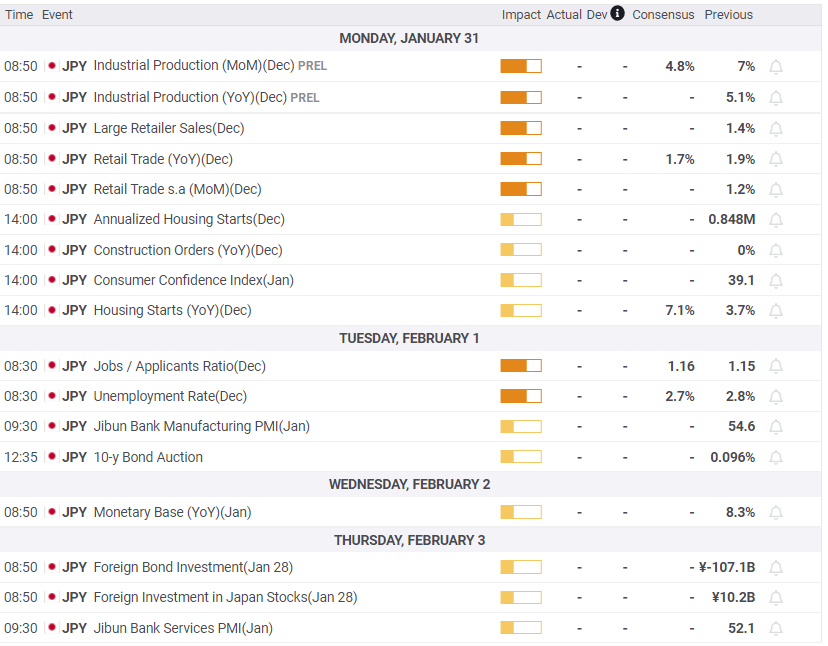

Japan statistics January 31–February 4

FXStreet

US statistics January 31–February 4

FXStreet

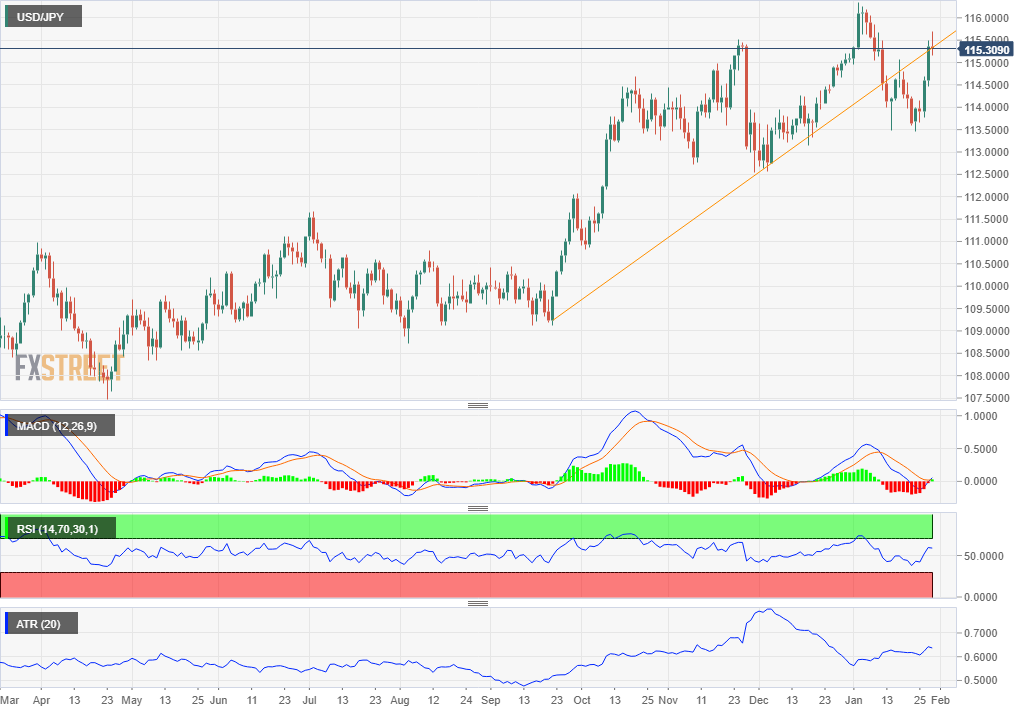

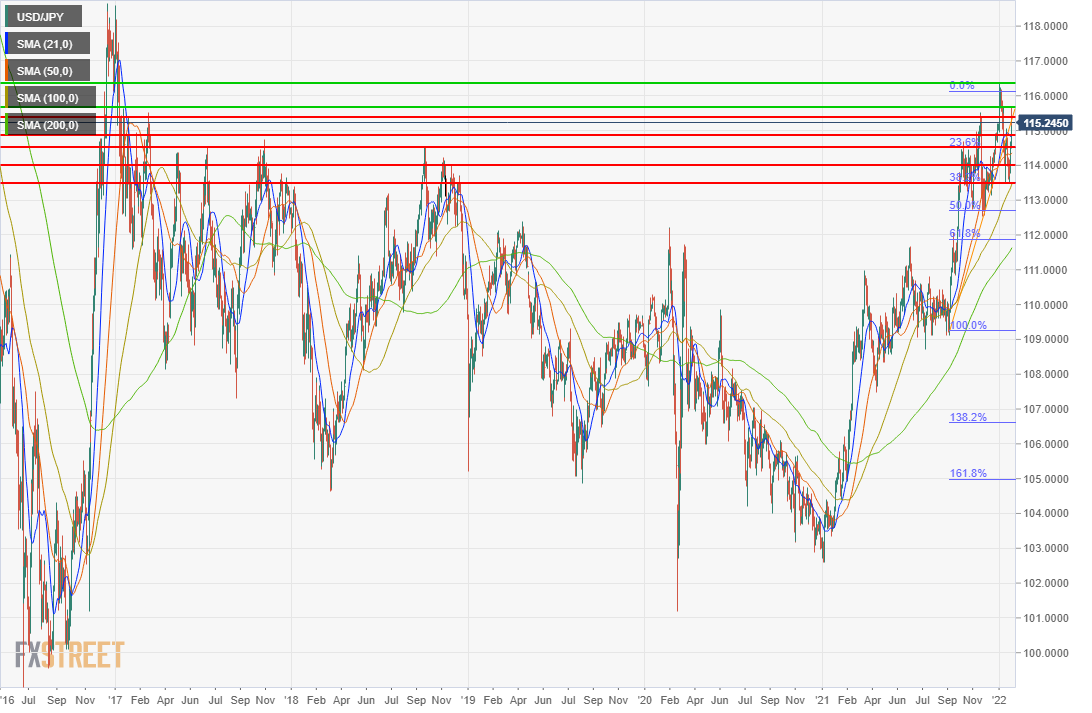

USD/JPY technical outlook

The USD/JPY rise since last Friday's close at 113.64 has brought the MACD (Moving Average Convergence Divergence) to the brink of a reversal. Strictly, the MACD line crossed the signal line on Friday but the Dollar yen's fall from the day's high at 115.69 makes the completion of the move tenuous and not yet fully positive. The Relative Strength Index (RSI) likewise moved into positive territory on Tuesday after rising from last Friday's nine month low. Volatility ebbed on Friday in the Average True Range (ATR) but was appreciably higher for the week and should resume its climb as the USD/JPY again approaches its four-year high at 116.35.

Support is the order of the day in USD/JPY. The line at 114.85 is supported by the 21-day MA at 114.86; the line at 114.50 is backed by the 23.6% Fibonacci level at 114.51: the line at 113.50 is seconded by the 38.2% Fibonacci at113.50 and the 100-day MA at 113.46. All three are substantial. Resistance is sparse and above the early January high must reference levels from early 2017 and are weak.

Resistance: 115.65, 116.35

Support: 114.85, 114.50, 114.00, 113.50

FXStreet Forecast Poll

The FXStreet Forecast Poll does not expect that the interest rate fundamentals will be sufficient to push the USD/JPY above 116.00. So far this year that analysis has been correct.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.