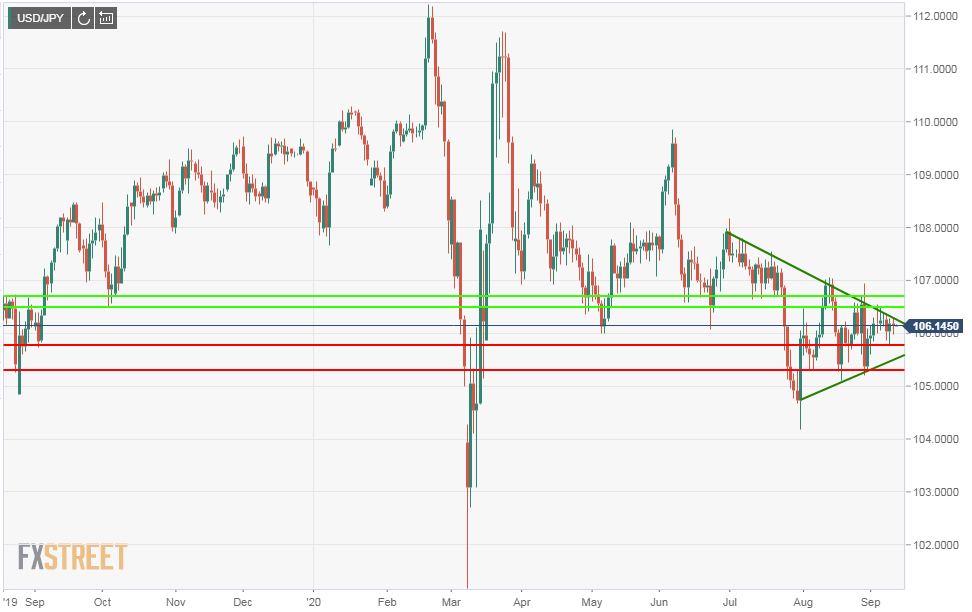

USD/JPY Weekly Forecast: A break is coming

- USD/JPY almost stationary above 106.00 with collapsing ranges.

- Euro failure at 1.1900 after ECB meeting on Thursday promotes USD.

- Japanese and US August economic statistics as yet offer little direction.

The dollar remained stalled just above 106.00 as US and Japanese economic and central bank developments failed to provide direction or incentive for movement.

Interestingly the European Central Bank meeting probably had more impact on the USD/JPY this week than any other event as it illustrated the limit of the weak dollar market view.

European Central Bank rate policy was universally expected to remain on hold at the September meeting. There was modest anticipation that the ECB might follow the Fed down the ‘lower for longer’ path with a version of the FOMC’s inflation averaging scheme.

Ms Lagarde, the ECB president, in her prepared statement and news conference steadfastly refused to hint at what might be coming from the bank’s current policy review. She noted several times that the bank did not target exchange rates and despite a number of pointed currency questions in her press conference would not elaborate on what effect the assessment might have on interest rates or inflation policy.

Markets initially took the euro higher briefly crossing 1.1900 but the lack of follow through soon eroded the gain and by the end of the session the euro had slipped back to 1.1800.

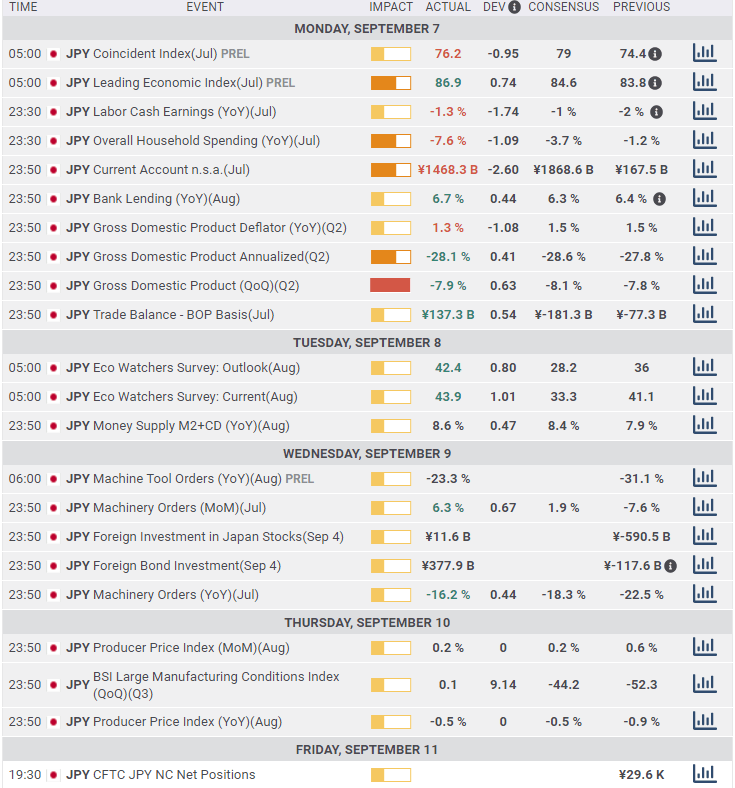

Japanese statistics showed some improvement in the August measures but were far short of a robust recovery. Annualized GDP in the second quarter was revised to -28.1%, worse than the initial release of 27.8% but better than the -28.6% prediction. The Eco Watchers Survey which follows regional trends was stronger than anticipated in August. The outlook gauge measured 42.4 on a 28.2 forecast and July’s 36. The current survey was 43.9, 33.3 and 41.1 respectively.

The producer price index rose 0.2% in August as expected down from the pandemic reversal bounce of 0.6% in July. The annual rate was -0.5% as forecast and -0.9% in July.

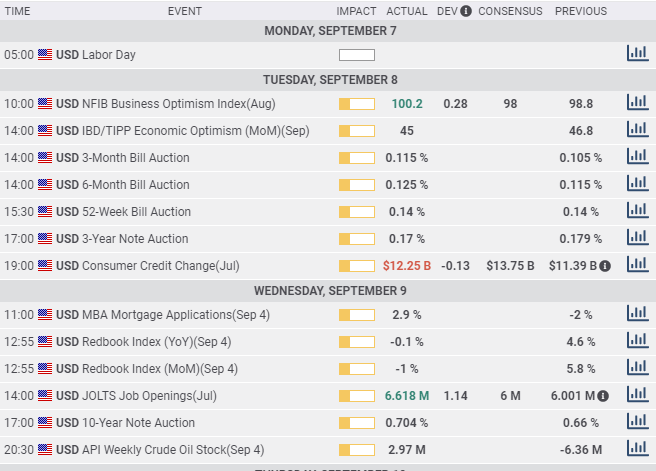

American statistics were mixed. The JOLTS job opening list for July at 6.618 million was better than 6 million forecast and June number but is still below the 7 million average for January and February. Consumer prices were firmer than forecast in August, 0.4% vs 0.3% in the overall and 0.4% vs 0.2% in core with 1.3% vs 1.2% and 1.7% vs 1.6% on the year, suggesting rising consumption.

Initial jobless claims for first week in September were worse than expected, 884,000 vs 846,00 and identical to the week before. Continuing claims rose to 13.385 million from 13.292 million, almost half a million more than the 12.925 prediction.

This lack of firm market direction in currencies and especially for the dollar was evident in the USD/JPY. While the dollar USD is still under pressure and the general view is negative for the greenback, currency movements have reached the limit of this scenario. Until there is a change in the fundamental outlook limited technical action and reaction seems to be the solution.

USD/JPY outlook

Japan’s recovery from the pandemic is hindered by several factors. Global consumption a crucial item in Japan’s export economy has yet to return to pre-virus levels. The fraught US-China relationship while far from a breaking point has inhibited China’s role as assembly point for foreign parts manufacturers and as the destination for new investment. Finally the Covid pandemic, now resurgent in Europe as it declines in the US continues to thwart a full-fledged recovery.

In the choice to replace Prime Minister Shinzo Abe who is resigning for health reasons, chief cabinet secretary Yoshihide Suga, a long-time Abe confident appears to have the inside track. As he has said he is seeking the post to take over the Prime Minister's unfinished work, little initial change in policy or goals are expected.

The USD/JPY remains dependent on the dollar side of the pair. It is clear that the summer rise in Covid case in several large states did not reverse the US recovery though it may have slowed it somewhat. The 31.8% plunge in annualized GDP in the Covid quarter has almost entirely reversed in the third according to the Atlanta Fed’s running estimate at 30.8%.

For more than two decades the US economy has been the more dynamic of the USD/JPY pair. Markets are willing to buy the dollar again but they are waiting for the statistical catalyst.

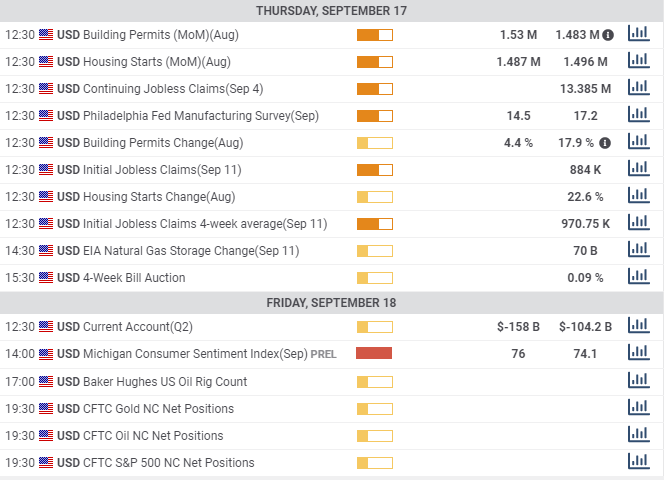

Japan statistics September 7-September 11

US statistics September 7-September 11

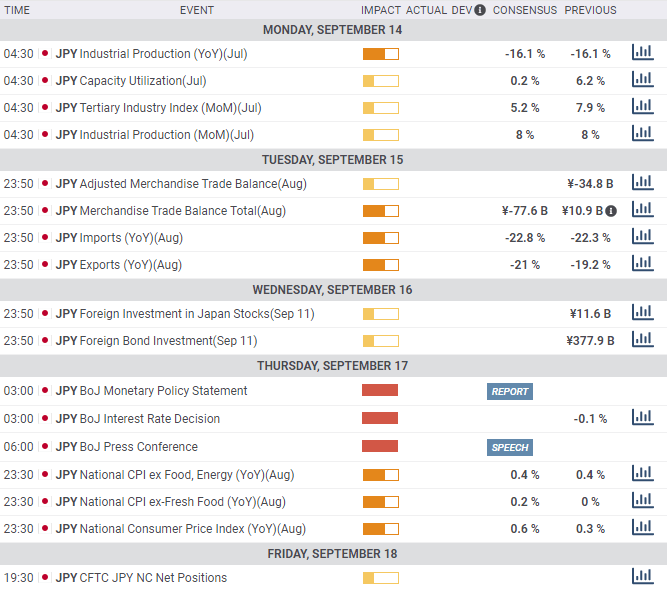

Japan statistics September 14-September 18

US statistics September 14-September 18

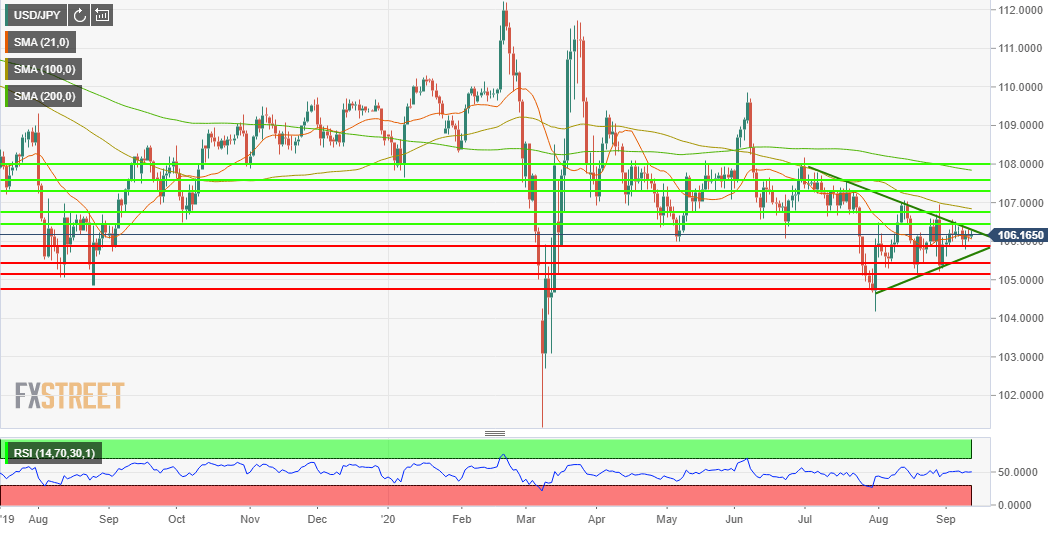

USD/JPY technical outlook

Moving averages; 21-day106.06; 100-day106.84; 200-day 107.84

Resistance: 106.40; 106.75;107;30; 107.60;108.00

Support: 105.85; 105.40; 105.15;104.75

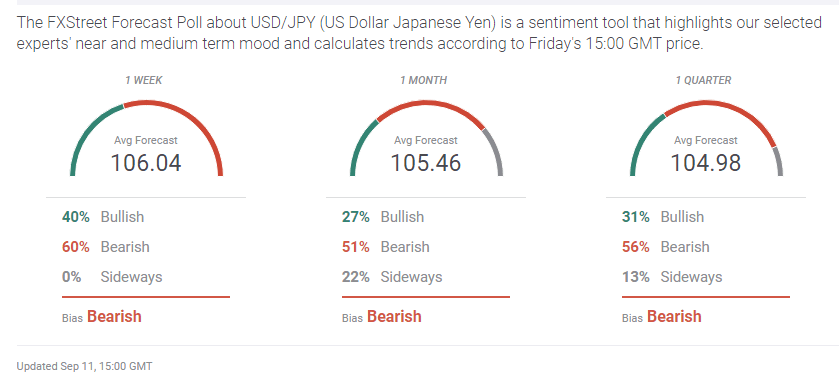

USD/JPY sentiment poll

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.