USD/JPY Forecast: Waiting for the China impact

- Yen regains status as safe-haven currency.

- USD/JPY collapses two figures on Friday.

- Statistics do not yet encompass the mainland economic shutdown.

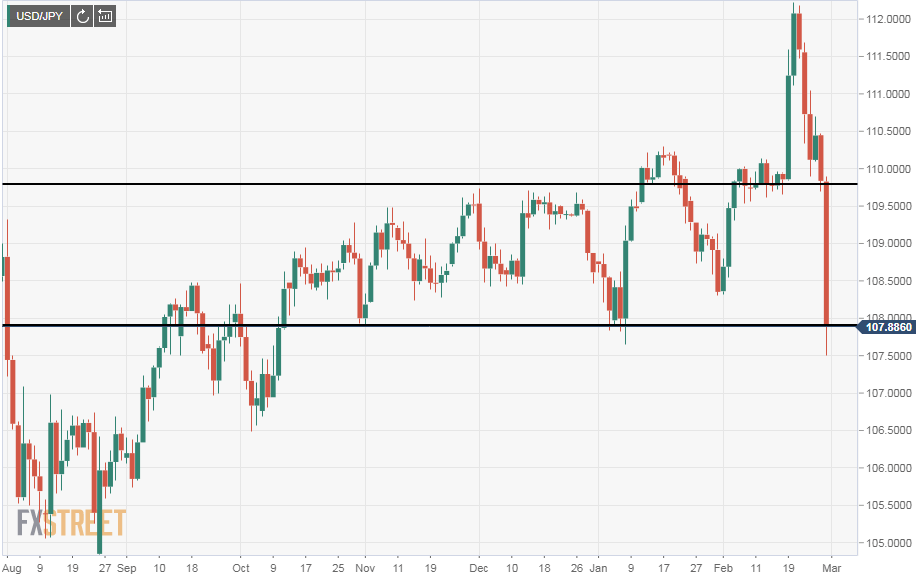

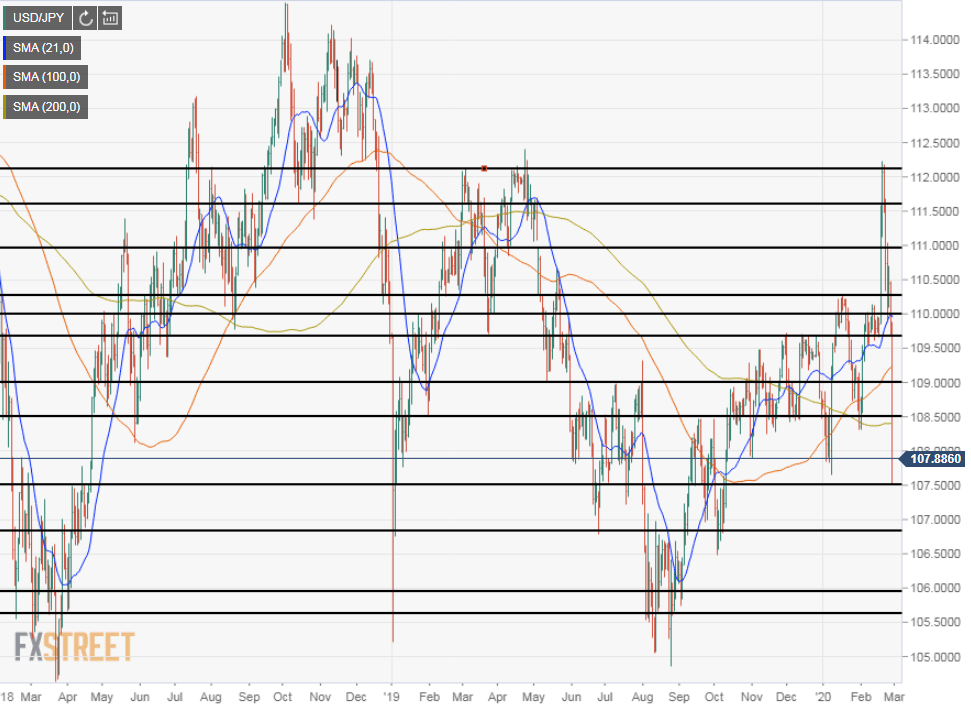

The USD/JPY began to weaken on Monday after closing last Thursday at a ten-month high of 112.07. The yen’s traditional status as a safe port in Asian markets had been undermined in the current Coronavirus turmoil by initially having the greatest number of confirmed cases of the virus outside of China. By the end of last week Japan had been passed by South Korea, Italy and Iran numbers and market had begun to reconsider.

The reversal began last Friday with a close at 111.59 followed by Monday’s finish at 110.73 and Tuesday’s end at 110.12. Wednesday’s saw a minor recovery to 110.44 but the slide resumed on Thursday which briefly penetrated the crucial 109.80 support but closed at 109.83.

That support, which was an amalgam of the lows for the first two weeks of February and a series of tops from November and December last year, was crossed in early Tokyo trading on Friday and the USD/JPY never recovered. From a global viewpoint there was no reason to consider Japan particularly afflicted, and once that idea was disposed, the yen’s traditional status as the safest Asian currency quickly reasserted itself. The close on Friday was at the four-month low, neatly defined by a series of widely spaced bottoms in in early November and then early January.

With the yen’s safety position reestablished, pending further developments, it will be the degree of market fear over the next days and weeks that determines the trading level.

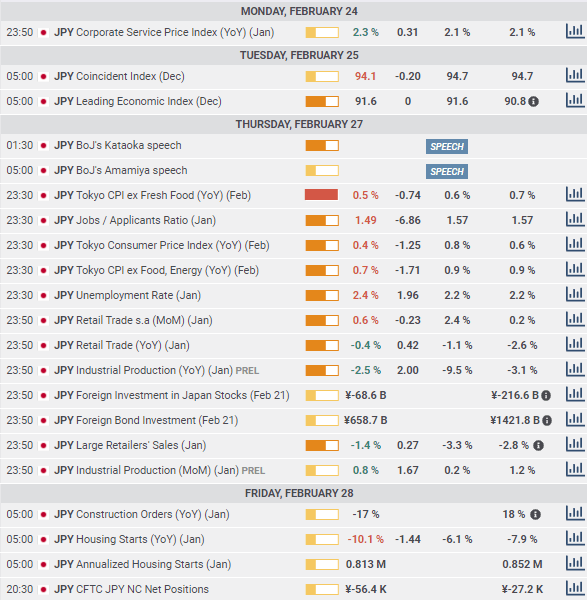

Japanese statistics February 24-28

Japanese economic information continued to display weak growth, sentiment and activity.

Tuesday

The Coincident index for December issued by the Cabinet Office which charts general economic activity was weaker than the 94.7 forecast at 94.1, and is now at the lowest level in almost seven years. The leading economic index for December also from the Cabinet came in as expected at 91.6, up from November’s 90.8 score, but this slight improvement still leaves it nearly a seven year trough.

Thursday

Retail trade which captures aggregate sales by businesses disappointed in January at just 0.6% on the month, 2.4% was forecast and a dismal -0.4% for the year. This is the fourth negative year over year result in a row.

Industrial production in January was better than projected at 0.8% and -2.5% on the year, 0.2% and -9.5% had been predicted. Annual production has declined for fourth straight months.

Japanese statistics conclusion February 24-28

While the industrial production numbers for January were better than expected, neither they nor the other statistics capture the likely decline in economic activity and confidence as the Chinese shutdown reality hits the islands economy. Worse probably lies ahead.

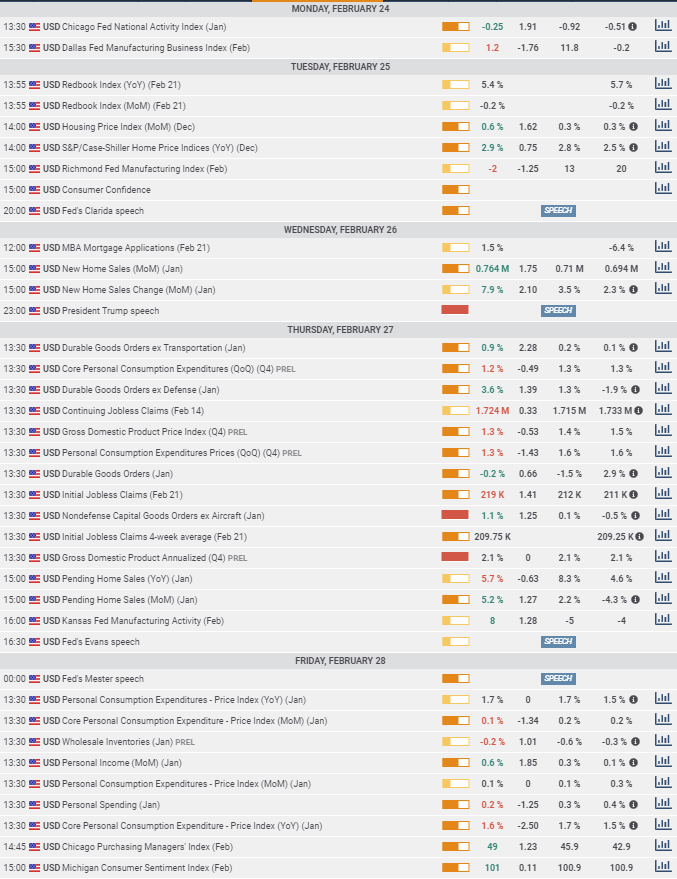

US statistics February 24-28

American statistics had a strong week though overshadowed by the Coronavirus reaction and the plunging US Treasury rates.

Consumer confidence from the Conference Board for February on Tuesday was 130.7 below the 132.0 forecast and January's 131.6 reading, near the mid-point of the last two years but among the highest scores of the past two decades.

New home sales in January, 0.764 million on an annualized basis for January, was better than the 0.71 million forecast and December’s 0.694 million result. It was the highest rate of purchases since September 2007 and is evidence of a thriving housing sector supported by the performance of the labor market.

Durable goods orders for January on Thursday were much better than expected in all four categories. The ex-defense purchases at 3.6% were almost three time the 1.3% prediction and the business investment proxy, non-defense capital goods at 1.1% was far ahead of the 0.1% projection and the highest since last October. Business investment has averaged 0.45% a month since the China trade deal was announced in October 2019. It had been -0.05% for the prior six months. In addition, the December results for all categories were revised higher. Finally, fourth quarter GDP was confirmed at 2.1% in the second release with one more assessment due on March 26th.

Initial jobless claims registered 209,750 in its four-week moving average once again knocking on the door of its half-century low.

Friday’s core personal consumption expenditure price index for January fell to 1.6% from 1.7%, and while this might interest the Fed, low inflation is a consumer asset. Personal income rose 0.6% last month double the estimate and far outstripping December's 0.1% gain. It was the highest monthly gain since December 2012. Personal spending was 0.1% lower than forecast at 0.2% but December’s figure was revised 0.1% higher to 0.4% balancing the effect.

The final version of the University of Michigan’s Consumer Sentiment Index for February improved to 101.0 from 100.9 bringing it to the highest level since March 2018 and the second highest point since the 2009 recession.

Statistics conclusion

While US statistics were far better than those from the Japanese side they were insufficient, in the week's tumult to overcome the emotional and safety drive to the yen. That condition is likely to remain true until the Coronavirus fears subside.

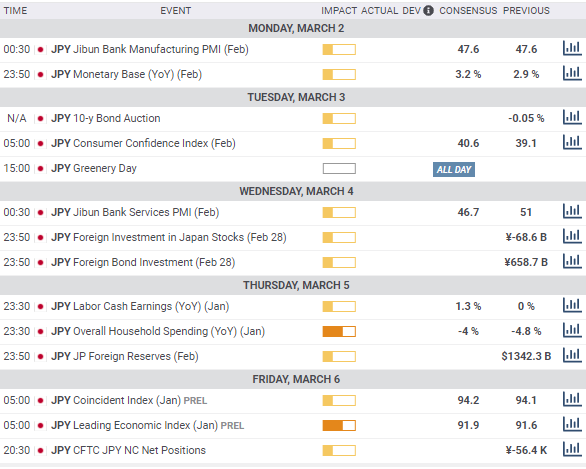

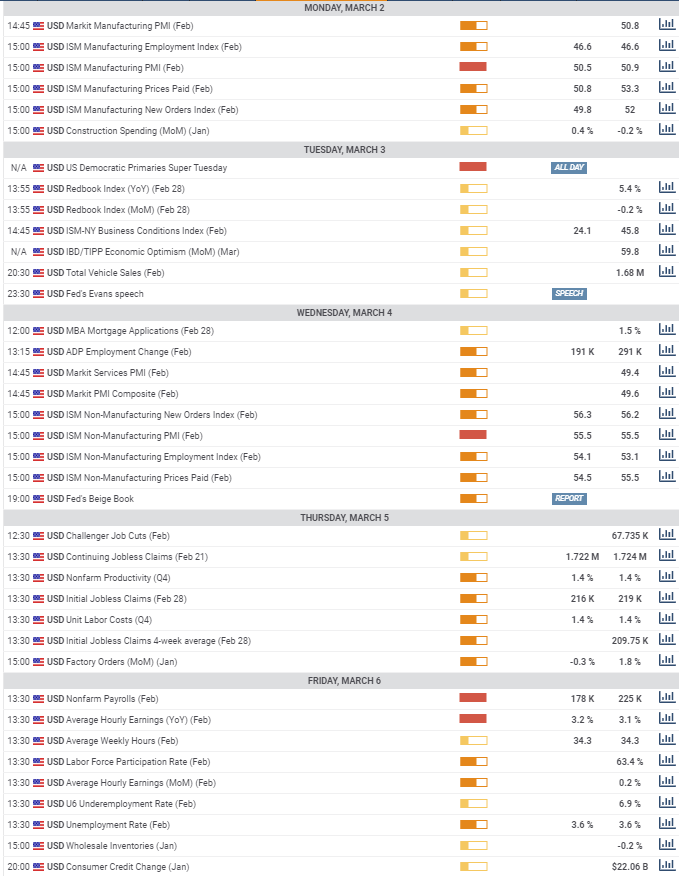

Japanese statistics March 2-6

Tuesday

Consumer confidence in February is expected to rise to 40.6 from 39.1 and though it has recovered somewhat form last year’s October slough at 35.6, every score from February 2015 to May 2019.

The Jibun Bank Services PMI for February is forecast to drop to 46.7 in February from 51 in January.

Thursday

Overall household spending in January is projected to decline 4% on the year after December’s 4.8% decrease for the third annual decline in a row.

Friday

The preliminary coincident index for January is forecast to add 0.1 point to 94.2.

The preliminary leading economic index for January is expected to rise to 91.9 from 91.6 in December.

Japanese statistics conclusion March 2-6

The modest gains expected in some of the economic criteria in January, if accurate, may provide a brief hiatus before the feared hit to the economy from the China health crisis. As such they are unlikely to provide an accurate reading on the future of the Japanese economy.

US statistics March 2-6

A busy week lies ahead in the United States.

Monday brings the February manufacturing purchasing mangers’ index (PMI) from the Institute for Supply Management. It is expected to maintain its hold on expansion at 50.5, down from January’s surprise jump to 50.9 from 47.8 in December. It was the first month above the 50 demarcation between expansion and contraction since August. New orders are forecast to fall back to 49.8 from 52 in January with the employment index stable at 46.6. This the first major manufacturing indicator that may register the impact of the China health crisis and will be closely watched.

The Democratic presidential primaries on Tuesday will occupy most of the news flow but with an inconclusive result for the nomination anticipated, they are unlikely to have much market impact.

Wednesday is the ADP precursor to the Employment Situation Report for February on Friday. Private payrolls are forecast to have added 191,000 workers in February following the January bonanza of 291,000.

Services PMI for February is projected to be unchanged at 55.5. New orders are forecast to rise 0.1 to 56.3 while employment should gain 54.1 from 53.1. As with the manufacturing figures traders will be looking for any signs of weakness related to the China virus slowdown.

The Organization of Petroleum Exporting Countries (OPEC) begins its meeting on Thursday and while their sway over oil prices is very weak the recent sharp drop in crude is sure to bring rhetorical flourishes from the members.

The US employment report on for February Friday is forecast to bring 178,000 new jobs after January’s unexpectedly strong 225,000. Unemployment will be unchanged at 3.6%, near its five decade low and annual wages will rise 3.2% up from 3.1% in January.

Statistics conclusion

Statistics conclusion

Statistics conclusion

Economic statistics in both nations this week will be viewed through the single narrow lens of the Coronavirus and its impact on global growth and financial security. The Japanese yen has revived its Asian safety ascendancy, expect that market opinion to continue.

USD/JPY technical outlook

The revival of the yen safety trade burned through all the support lines that had gathered for the last five months, reference is now to the period from August to early October 2019.

The 21-day average has ticked lower on the week's move but there is no trend while the 100-day and 200-day trends have paused awaiting development.

Weak support is at 107.50 with stronger lines at 106.85, 106.00 and 105.65.

First resistance is 108.50 followed 109.00, 109.70, 110.00 and 110.25 and 111.00. At long range we have 111.60 and 112.15.

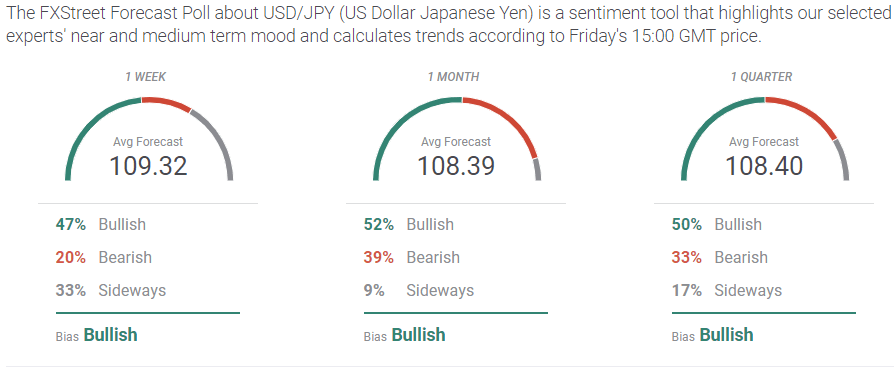

USD/JPY sentiment poll

Sentiment this week has completely reversed from its bearish stance seven days ago.

The one week view is 47% bullish vs 27%, bearish is down to 20% from 40% and neutral is the same at 33%. The forecast is two figures lower at 109.32 from 111.31, but it is almost two figures above the Friday close at 107.88.

The one month view is far more bullish at 52% vs 15%, far less bearish 39% vs 82% and slightly higher for neutral at 9% vs 3%. The forecast at 108.39 is mid-way between last week's 109.19 and the close at 107.88.

The one quarter outlook is also far more bullish, 50% vs 17%, half as bearish 33% vs 76% and more unsure at 17% vs 7%. The forecast is not different than the one month at 108.40.

This week's sentiment is a classic of mean reversion. The bearish view of last week was enacted and the response reverts to the mid-point in the range.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.