USD/JPY Forecast: Fed dovishness and the global slowdown prove toxic, trade and the ISM awaited

- USD/JPY dropped mostly due to the Fed's dovish decision.

- The services sector survey stands out in the first full week of February.

- The technical picture is becoming mixed for the pair. Experts see falls in the short term but gains afterward.

This was the week: Dovish Fed dominates

The Federal Reserve made a significant dovish twist. They no longer foresee a gradual increase in interest rates but pledge patience amid a global slowdown and uncertainty due to the government shutdown. The central bank took one step further and announced it might change the balance sheet reduction program.

The result was a rise in stocks and a weaker US Dollar across the board, also against the Japanese yen. There were a few additional dovish things. See: 5 Dollar downers in the Fed decision, and why the sell-off may continue

End-of-month flows mitigated part of the greenback's descent.

The Non-Farm Payrolls report was mixed: while the economy gained 304K jobs, it came on top of a significant downward revision and wage data was mixed with only 0.1% MoM. Year over year, salaries rose by 3.2%.

Trade talks between China and the US continued in Washington. While President Donald Trump and Chinese officials expressed optimism, some trade hawks in the Administration still see a long way to go. Trump and his Chinese counterpart Xi Jinping may meet later in February.

China's Caixin Manufacturing PMI extended its falls, adding to worries about a slowing Chinese economy. Germany officially slashed growth forecasts, and Italy entered a recession. The UK Parliament instructed the government to renegotiate Brexit, and this was met with immediate rejection by the European Union. All in all, the safe-haven yen had reasons to rise.

In Japan, the Bank of Japan's meeting minutes did not stray from the extremely loose monetary policy.

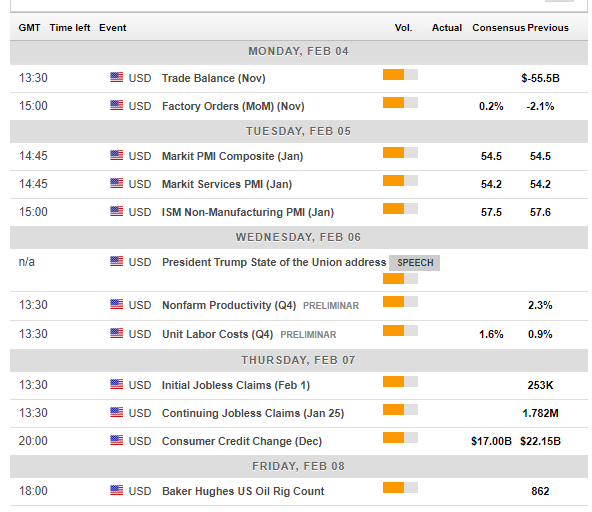

US events: ISM data and more releases to come

The US government shutdown ended, but not all data points have been released or rescheduled. The calendar may be updated with further events. The most important figure that is missing is the first estimate of Q4 2018 GDP.

Trade balance kicks off the week and will serve as input to the trade talks between the US and China. Factory orders will be of interest.

The ISM Non-Manufacturing PMI for January stands out amid concerns about the slowdown and the shutdown that was in place during most of the month. The forward-looking gauge fell from the high levels and may continue falling.

Trump will deliver his State of the Union address on Wednesday. It was postponed due to the shutdown. Markets will be looking for any new economic plans such as infrastructure spending and a new tax bill in the wide-ranging speech. Willingness to work with Democrats would also help as the government is currently open only until February 15th. A long-term solution is still awaited.

Weekly jobless claims will be watched more closely after they leaped to 253K last time. Markets will want to verify it is only a one-off and not a change in the dynamics of the US labor market.

All in all, the week is somewhat quieter regarding macroeconomic events, but a rescheduling of delayed data and political events may provide surprises.

Here are the top US events as they appear on the forex calendar:

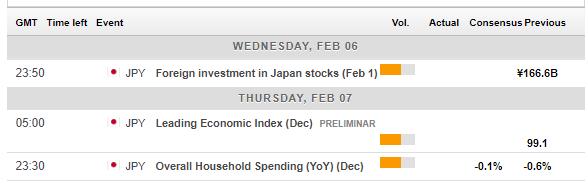

Japan: Trade talks have growing importance

While top-level trade talks have ended in Washington, they continue at lower levels. Headlines related to the negotiations can move the safe-haven yen. Progress will likely diminish demand for the currency while reports that talks are stuck can send it higher.

Confirmation of a Trump-Xi Summit may help. Trump finds it hard to confront leaders face to face. He may be charmed to give up some demands in a meeting, something he would not do from afar and something his trade hawks would never do.

In Japan, foreign investment may be of interest, and also the preliminary leading economic index might have an impact. However, the yen mostly moves on market sentiment. The Chinese New Year holiday means no new disappointing data from the world's third-largest economy.

Here are the events lined up in Japan:

USD/JPY Technical Analysis

USD/JPY seems to have ended its recovery and began falling once again. The 50-day Simple Moving Average crossed the 200-day one, a pattern known as the "death cross." On the other hand, Momentum has turned positive. The Relative Strength Index is stable. All in all, the pair is looking for a new direction.

Support awaits at 108.50 which was the low point this week. The next line to watch is 108.20 that was a stepping stone on the way up in mid-January. 107.75 had the same role. It is closely followed by 107.50 which is where the pair stabilized after the flash crash. 106.50 dates back to early 2018 while 104.87 is the flash crash low.

109.15 provided support when the pair attempted to break above 110. That round number of 110 capped USD/JPY in recent weeks. Further up, 110.40 was a support line in August. It is followed by 111.40 that limited a recovery early in the new year.

-636846089687344276.png)

USD/JPY Sentiment

The Fed's dovishness weighs on the USD and the global slowdown boosts the safe-haven yen. There is further room to the downside.

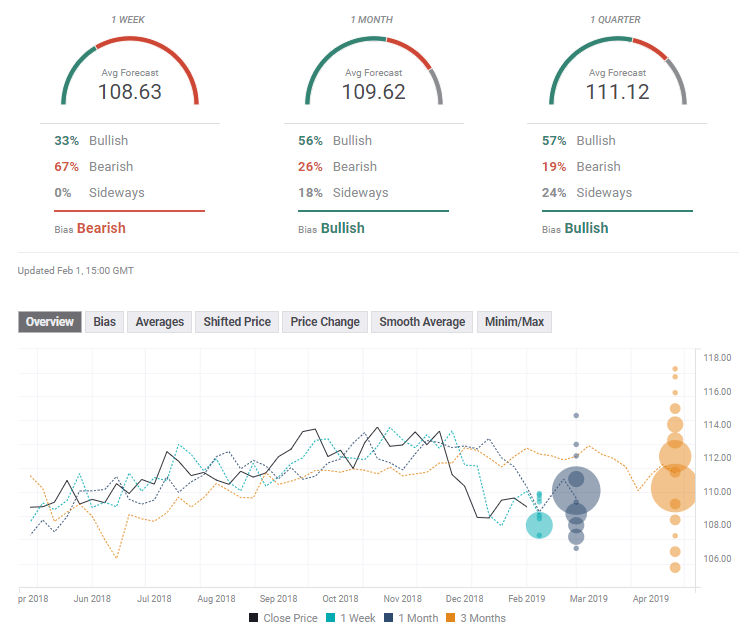

The FXStreet forex poll of experts shows a bearish tendency in the short term but a bullish one afterward, with an ambitious long-term target. Forecasts have been upgraded for the short and long terms and downgraded for the medium term.

Related Forecasts

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.