USD higher despite lacklustre economic data

Market Brief

The US dollar was better bid yesterday in spite of lacklustre economic data from the world’s largest economy. The September durable goods orders report did not give much room for excess optimism. The headline gauge printed below expectations, contracting 0.1%m/m versus 0.0% expected after an upwardly expansion of 0.3% in August. However, ex-transportation orders matched expectations and printed at 0.2%, after rising 0.1% in the previous month. Nevertheless, when excluding non-defense capital goods and aircraft, orders fell 1.2%, suggesting that the factory sector industry is still under pressure. Even though the US election could be a significant drag on investment, the strength of the dollar and sluggish global growth offer little grounds for optimism. After hitting 1.0942 in the European session yesterday, EUR/USD slid towards 1.0883 before stabilising at around 1.09. The strong support at 1.00822 (low from October 3rd) is still untouched, while on the upside the 1.12-1.13 area will act as resistance.

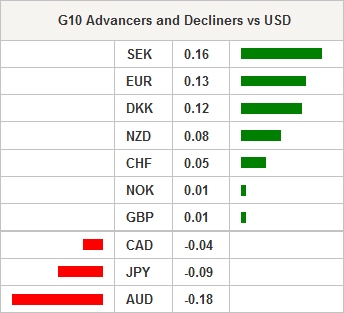

On Friday, the Australian dollar was the worst performer among the G10 complex. AUD/USD moved back below the top line of its long-term declining channel, currently trading at around 0.7574. The boost provided by the better-than-expected CPI report on Wednesday was short-lived as the Aussie completely erased those gains. The Reserve Bank of Australia will deliver its interest rate decision next Monday and will likely stay on hold for now.

The Japanese yen continued to lose ground against the US dollar. The last CPI report from Japan showed that inflationary pressures remained subdued in September. Headline CPI gauge fell 0.5%y/y in September, while the BoJ’s favourite gauge of inflation, which excludes fresh food was off 0.5% as well, while the gauge excluding energy and fresh food printed flat. All in all, it seems as though the multiple easing measures implemented by the Bank of Japan have had little effect in terms of boosting inflation and the market is growing steadily impatient. For now, the market is exclusively focused on pricing in the upcoming interest rate hike in the US. However, this distraction will soon dissipate and investors will start looking again towards the BoJ and will challenge Kuroda by pushing the JPY higher. USD/JPY tested 105.42 in Asia, up more than 1.50% since the beginning of the week.

Today traders will be watching the CPI report from Spain, France, Germany and Brazil; consumer confidence from the euro zone; personal consumption, core PCE and GDP from the US; interest rate decision from Russia.

| Global Indexes | Current Level | % Change |

|---|---|---|

| Nikkei 225 Index | 17446.41 | 0.63 |

| Hang Seng Index | 22877.16 | -1.1 |

| Shanghai Index | 3104.271 | -0.26 |

| FTSE futures | 6910.5 | -0.66 |

| DAX futures | 10588.5 | -1.14 |

| SMI Futures | 7850 | -0.86 |

| S&P future | 2117.2 | -0.29 |

| Global Indexes | Current Level | % Change |

|---|---|---|

| Gold | 1267.2 | -0.09 |

| Silver | 17.63 | 0.01 |

| VIX | 15.36 | 7.87 |

| Crude wti | 49.51 | -0.42 |

| USD Index | 98.8 | -0.09 |

| Today's Calendar | Estimates | Previous | Country/GMT |

|---|---|---|---|

| SZ Oct KOF Leading Indicator | 101,8 | 101,3 | CHF/07:00 |

| SP Oct P CPI EU Harmonised MoM | 0,60% | 0,70% | EUR/07:00 |

| SP Oct P CPI EU Harmonised YoY | 0,30% | 0,00% | EUR/07:00 |

| SP Oct P CPI MoM | 0,80% | 0,00% | EUR/07:00 |

| SP Oct P CPI YoY | 0,30% | 0,20% | EUR/07:00 |

| SP 3Q P GDP QoQ | 0,70% | 0,80% | EUR/07:00 |

| SP 3Q P GDP YoY | 3,10% | 3,20% | EUR/07:00 |

| SW Sep Retail Sales MoM | 0,30% | 0,60% | SEK/07:30 |

| SW Sep Retail Sales NSA YoY | 2,70% | 2,80% | SEK/07:30 |

| EC ECB's Benoit Coeure Speaks in Frankfurt | - | - | EUR/07:30 |

| RU oct..21 Money Supply Narrow Def | - | 8.71t | RUB/08:00 |

| NO Oct Unemployment Rate | 2,80% | 2,80% | NOK/08:00 |

| EC ECB Governing Council Member Lane Speaks in London | - | - | EUR/08:00 |

| SW Riksbank I/L Bond Purchase Results | - | - | SEK/08:10 |

| EC Oct Economic Confidence | 104,9 | 104,9 | EUR/09:00 |

| EC Oct Business Climate Indicator | 0,46 | 0,45 | EUR/09:00 |

| EC Oct Industrial Confidence | -1,6 | -1,7 | EUR/09:00 |

| EC Oct Services Confidence | 10 | 10 | EUR/09:00 |

| EC Oct F Consumer Confidence | -8 | -8 | EUR/09:00 |

| BZ Oct FGV Inflation IGPM MoM | 0,20% | 0,20% | BRL/10:00 |

| BZ Oct FGV Inflation IGPM YoY | 8,84% | 10,66% | BRL/10:00 |

| RU oct..28 Key Rate | 10,00% | 10,00% | RUB/10:30 |

| SA Sep South Africa Budget | - | -16.68b | ZAR/12:00 |

| GE Oct P CPI MoM | 0,20% | 0,10% | EUR/12:00 |

| GE Oct P CPI YoY | 0,80% | 0,70% | EUR/12:00 |

| GE Oct P CPI EU Harmonized MoM | 0,10% | 0,00% | EUR/12:00 |

| GE Oct P CPI EU Harmonized YoY | 0,70% | 0,50% | EUR/12:00 |

| US 3Q Employment Cost Index | 0,60% | 0,60% | USD/12:30 |

| US 3Q A GDP Annualized QoQ | 2,60% | 1,40% | USD/12:30 |

| US 3Q A Personal Consumption | 2,60% | 4,30% | USD/12:30 |

| US 3Q A GDP Price Index | 1,40% | 2,30% | USD/12:30 |

| US 3Q A Core PCE QoQ | 1,60% | 1,80% | USD/12:30 |

| US Oct F U. of Mich. Sentiment | 88,2 | 87,9 | USD/14:00 |

| US Oct F U. of Mich. Current Conditions | - | 105,5 | USD/14:00 |

| US Oct F U. of Mich. Expectations | - | 76,6 | USD/14:00 |

| US Oct F U. of Mich. 1 Yr Inflation | - | 2,40% | USD/14:00 |

| US Oct F U. of Mich. 5-10 Yr Inflation | - | 2,40% | USD/14:00 |

Currency Tech

EURUSD

R 2: 1.1352

R 1: 1.1058

CURRENT: 1.0923

S 1: 1.0822

S 2: 1.0711

GBPUSD

R 2: 1.2857

R 1: 1.2477

CURRENT: 1.2177

S 1: 1.2090

S 2: 1.1841

USDJPY

R 2: 111.45

R 1: 107.49

CURRENT: 105.30

S 1: 102.80

S 2: 100.09

USDCHF

R 2: 1.0328

R 1: 1.0093

CURRENT: 0.9927

S 1: 0.9632

S 2: 0.9522

- S: Strong, M: Minor, T: Trendline, K: Keylevel, P: Pivot

Author

Arnaud Masset

Swissquote Bank Ltd

Arnaud Masset is a Market Analyst at Swissquote Bank. He has a strong technical background and also works in the development of quantitative trading strategies.