USD/CAD Weekly Forecast: The commodity complex starts to look shaky

- USD/CAD falls on Wednesday after 6.7% Canadian CPI.

- Fed Chair Powell stokes rate speculation on Thursday, USD/CAD reverses.

- US 10-year Treasury yield adds 5 basis points to 2.875%.

- Canada 10-year note rises 10 points to 2.871%.

- FXStreet Forecast Poll predicts upside technical failure.

The Bank of Canada and the Federal Reserve added another verse to their policy roundelay this week as inflation drove speculation that half-point hikes are the next order of business for both banks.

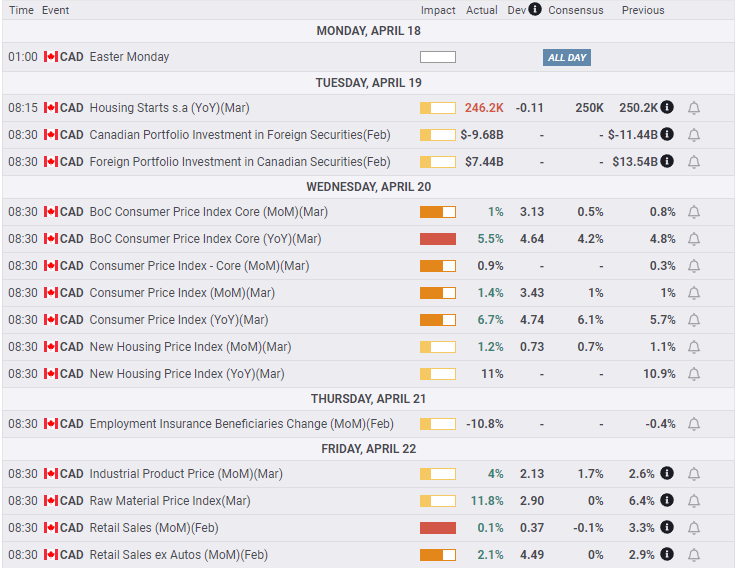

Canadian consumer inflation soared to 6.7% in March (YoY), far more than the 6.1% forecast, from 5.7% in February. The 1.4% monthly gain brought the Consumer Price Index (CPI) to its highest annual rate since February 1991. Core inflation measured by the Bank of Canada (BoC) rose 1% on the month, double the expectation, bringing the yearly rate to 5.5% from 4.8%. The consensus prediction was for a drop to 4.2%.

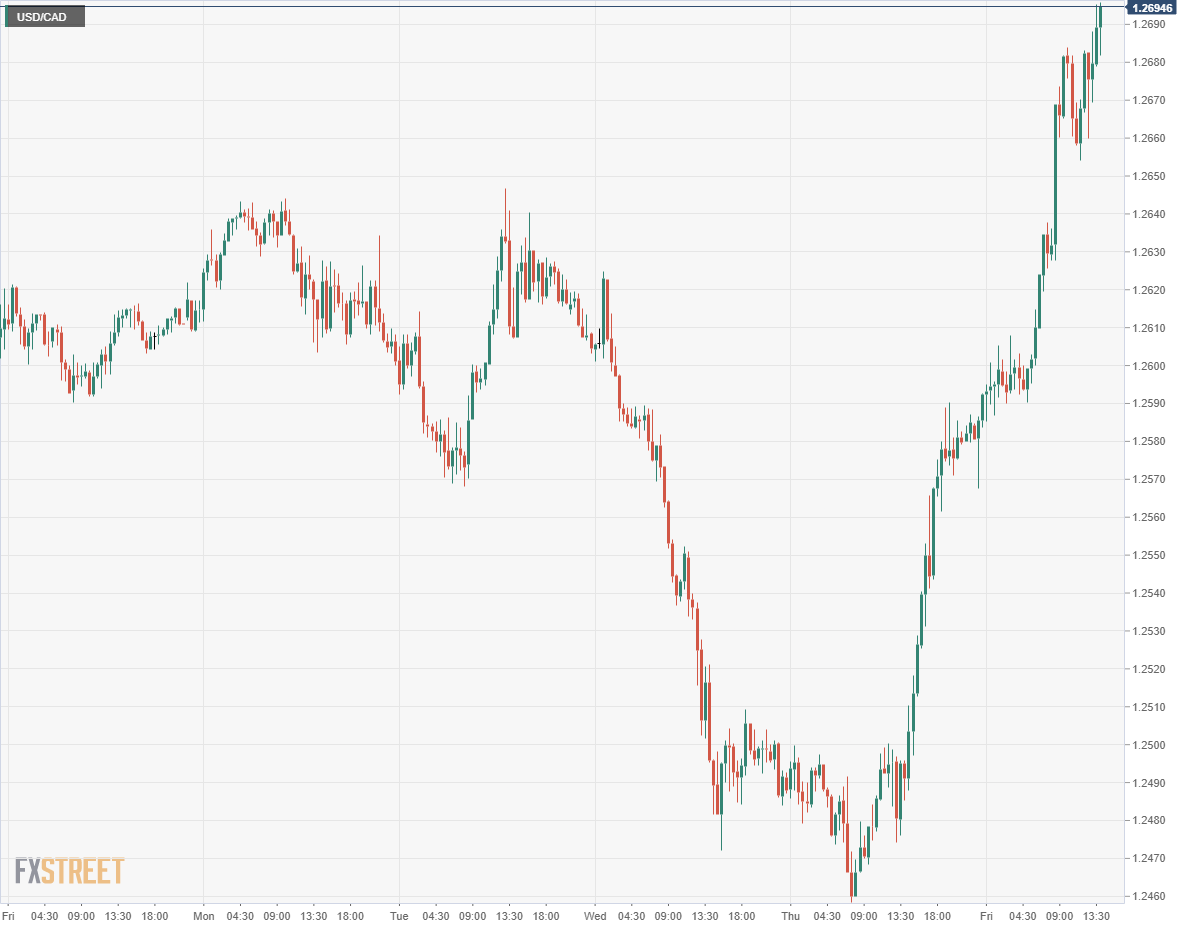

The USD/CAD cascade began on Wednesday when the 8:30 am release sent the pair through support at 1.2570. Selling continued for the rest of the US market with the close of 1.2496 just points above the low at 1.2482. Dollar Canada remained below 1.2500 for the Asian session and in Europe on Thursday until Federal Reserve Chair Jerome Powell suggested the bank might opt for half-point increases at the next two meetings.

“I would say that 50 basis points will be on the table for the May meeting,” observed Mr Powell at an IMF panel he shared with ECB President Christine Lagarde among others. The Fed chief also cemented expectations for a second hike in June. “There’s something in the idea of front-end loading, so that points in the direction of 50 basis points being on the table," said Mr. Powell.

The USD/CAD responded by rising almost a figure closing at 1.2582 on Thursday and continued to power-up on Friday trading as high at 1.2721, its best since March 16.

The BoC raised the overnight rate 0.5% last Wednesday to 1.0%, in the first 50 point jump in 22 years. Governor Tiff Macklem said the bank will begin to reduce its C$350 billion ($275 billion) portfolio acquired during the pandemic this month by not reinvesting the proceeds of maturing securities. Over the next year about one-quarter of the BoC’s holdings could be discharged.

The next policy meeting is June 1 and overnight swaps have fully priced in a half-point increase in the overnight rate to 1.5%.

If the Fed hikes 0.5% to 1.0% on May 4 and adds another 0.5% on June 15, the policy rates of the two banks would be identical at 1.5%. These alternating and well-telegraphed rate increases, accompanied by complementary and nearly matching increases in each countries' bond yields have obviated any currency impact.

The US 10-year Treasury yield rose 8 basis points for the week to 2.904%, Canada’s version added 10 points to 2.873%.

West Texas Intermediate (WTI) and the Bloomberg Commodity Index (BCOM) fell 4.9% and 4.4% respectively on the week, keeping pressure on the resource backed Canadian dollar. Sharply rising commodity prices over the past year have been one of the loonie’s main supports, helping to thwart the general rise in the US dollar.

Consumer inflation in Canada was the most influential release but two producer gauges, Industrial Product Prices and the Raw Material Price Index promise more inflation pain ahead. Industrial product prices, which track costs for major commodities sold by Canadian manufacturers, rose 4% in March, more than double the 1.7% forecast and up from 2.6% in February. The raw material index, which records commodity prices paid by manufacturers, soared 11.8% in March following 6.4% and 6.5% jumps in February and January.

Retail Sales were stronger than predicted in February rising 0.1% for the month and 2.1% over the year on estimates of -0.1% and flat but provoked no USD/CAD reaction. January’s sales were revised higher.

In the US, Mr. Powell’s comments were the chief market news. Existing Home Sales dropped a bit more than expected in March, reflecting the sharp rise in mortgage rates. Building Permits and Housing Starts remained at or near their highest levels since the bubble of over a decade ago. Initial Jobless Claims were 184,000 in the April 15 week. The 4-week moving average came in at 177,250, its third lowest result on record, after the totals of the two previous weeks.

Fed Chair Powell noted in his Thursday IMF appearance that the demand for workers is “too hot, you know it is unsustainably hot.”

USD/CAD outlook

Jerome Powell may have broken the immediate USD/CAD longjam but it is a long way to the effective 1.2900 top of the range of the last 10 months and a new trend.

Speculative positioning in the USD/CAD had not looked far beyond the May 4 Fed meeting. Mr. Powell’s deliberate reference to a 50 basis point hike in June has put policy into a much more aggressive stance. The Fed may have stolen a rhetorical march on the BoC but even if the FOMC carries through, it will leave the banks with identical base rates in June. Bond yields in both countries have moved higher in unison.

The Ukrainian war has stalemated. Kyiv seems secure from defeat but far from victory. Russia continues to attack in the east leaving a negotiated settlement forlorn. Sanctions on Russia will stay and that has kept commodity and oil prices from descending to pre-invasion levels. The rising inflationary drag on consumption coupled with rapid central bank tightening has brought second and third quarter recession fears to the fore. Any indication that the US consumer is pulling back on spending could cut the floor from commodity prices.

An economic slowdown or recession is the greatest risk for the Canadian dollar as it would undercut the loonie’s main support. As that possibility rises the USD/CAD prospects improve. The balance has not yet shifted to a full-fledged USD/CAD rally but the indications are pointing in that direction.

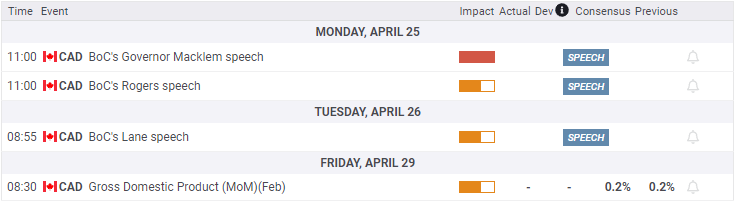

Canadian information is sparse in the week ahead with only February GDP on tap. Speeches from several BoC officials, including Governor Macklem may provide comments on policy.

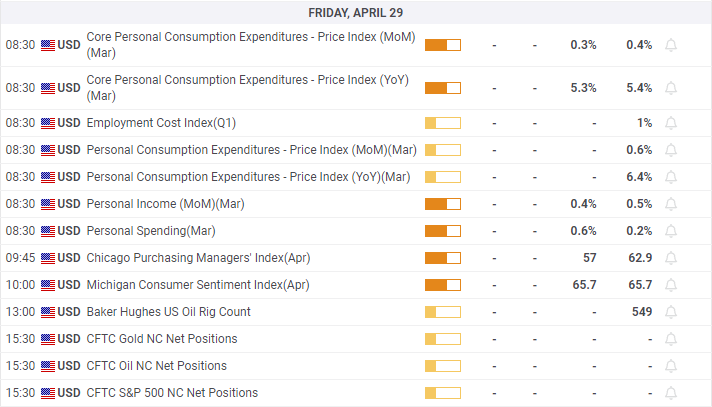

In the US, first quarter GDP on Thursday is of great importance. Economic growth is expected to drop to 1.0% from 6.9% in the fourth quarter. The Atlanta Fed estimate is 1.3%. Any deviation from the forecast, especially if the number is near or below zero will undermine the Fed’s rate plans and by extension Treasury rates and the US dollar. Durable Goods Orders for March should reflect the strong Retail Sales figures. Friday’s March Personal Consumption Price Index, the Fed’s preferred gauge, will add nothing new to the inflation picture nor will the Personal Income and Spending numbers.

The USD/CAD outlook is higher.

Canada statistics April 18–April 22

FXStreet

US statistics April 18–April 22

FXStreet

Canada statistics April 25–April 29

FXStreet

US statistics April 25–April 29

FXStreet

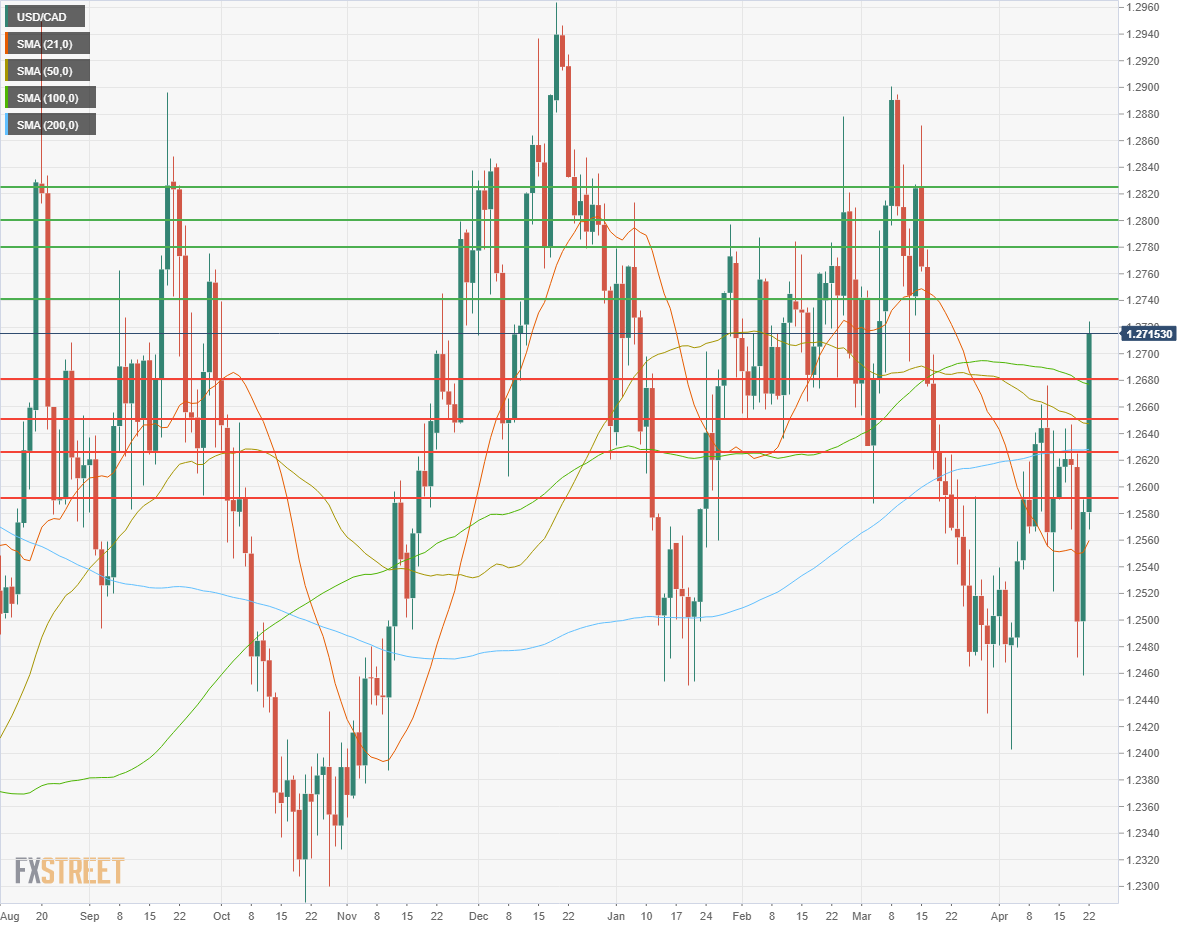

USD/CAD technical outlook

Friday's near figure-and-a-half run higher rang all the technical bells for substantial change in market attitude for the USD/CAD. Taken from Thursday's open at 1.2499 the USD/CAD gained 1.8% in two sessions, its steepest jump since August 2021. The Friday surge crossed the 200-day moving average (MA) at 1.2628, the 50-day MA at 1.2648 and the 100-day at 1.2677, in quick succession. The 21-day MA at 1.2560 was crossed on Thursday. The three longer averages represent the USD/CAD's range-bound trading of the past five months and their abrupt dismissal is emblematic of a change in outlook.

The MACD (Moving Average Convergence Divergence) moved into positive territory with the late week rise, as did the Relative Strength Index (RSI) and both are buy signals. Volatility in Average True Range (ATR) rose to its highest level in three weeks with the Wednesday plunge and following recovery.

Immediate support is centered on the 100-day, 50-day and 200-day moving averages.

Resistance: 1.2740, 1.2780, 1.2800, 1.2825

Support: 1.2680, 1.2650, 1.2625, 1.2590

Moving averages: 21-1.2560, 50-1.2648, 100-1.2677, 200-1.2628

FXStreet Forecast Poll

The late week rise in USD/CAD has reversed the one-week bullish prediction in the FXStreet Forecast Poll. All three terms are now bearish, an outlook belied by the fundamental outlook.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.