USD/CAD is on a downswing

Outlook:

We get the ISM manufactur ing index this mor ning, for ecast at the flash 53.2, the highest since July 2015. It was 51.5 in Sept and a lousy 49.4 in August. A modest recovery shows resilience in the face of contraction in the oil patch. We also get auto sales, with investors.com reporting "overall U.S. sales are expected to match the highest level of the year, coming in at a 17.8 million-unit annual rate, though that would be another year-over-year decline."

And not to be missed is Aug GDP from Canada, likely 0.2% m/m and 1.3% y/y. Given the lack of coherence from the BoC, we don't know if this is good or bad. The USD/CAD is on a downswing, so expectations must be for a good report.

We are seeing some talk about a recovery in commodities as having a big influence on perception of upcoming inflation, emerging market currency effects and other matters. Below is the Reuters-Jeffries CRB index from Bloomberg. After a double bottom in Aug and Sept, the index is struggling to matchand- surpass the previous high from early June. Bottom line—some commodities are up (industrial metals) and some are down, like oil, and to project big outcomes off this chart looks unwise.

Probably the biggest effect of commodities is on inflation, which some persist in seeing lurking under every bush. The WSJ keeps insisting inflation is already here. "The rise in inflation expectations is clear. The average U.S. inflation rate over the next 10 years priced into bond markets is at its highest level this year, having risen from 1.55% at the start of January to 1.74%. The rate for the five years starting in five years' time, designed to strip out short-term moves such as oil-price swings, is also at a new high for the year of 1.84%, after dipping to 1.4% in both February and June."

Worse, TIPS started the year "offering 0.72% above inflation for 10 years, TIPS now offer just 0.12%" Golly, doesn't this mean inflation expectations have fallen? The point of the WSJ article is that slower growth coupled with rising inflation expectations, as shown by the commodity price bounce, means both equities and bonds offer no return to speak of.

"This breakdown in the dollar's usual relationships has helped to shield emerging markets from the turmoil often associated with a stronger greenback in the past. Indeed, this year several emerging com-modity exporters have had stunning gains in their currencies, with the Brazilian real up 25%, Russian ruble up 15% and South African rand up 14%. Weakness in China's yuan means the dollar is up a little on a trade-weighted basis against emerging currencies this year, but it's at the same level as in June."

We are deeply unhappy about this slant on things. It's the tail wagging the dog. Commodity prices go up on supply constraints or higher demand. If it's higher demand, as in the case of industrial metals, you can't also complain about slow growth. Demand for industrial metals almost by definition means higher growth. So, either the demand estimate is wrong or the low growth thesis is wrong. It would be very odd to have rising inflation due to rising demand for commodities and rising commodity prices and slow growth at the same time. Besides, to name Brazil and Russia, never mind China, as having currencies linked solely to commodity prices is downright silly. We don't follow emerging market cur-rencies much anymore, but political risk is surely of equal importance. We have one word—Rousseff. The rand, also, tanked on a political event (arresting the finance minister) and then jumped when the event was reversed (although S. Africa quit the International Criminal Court and the fallout from that is yet to be determined).

Bottom line: reporters desperate to find linkages between asset classes are stretching the bounds of cre-dulity. Granted, asset classes are related, if sometimes by only the most tenuous of links, but creating correlations out of thin air can lead to seriously flawed deductions. Yes, we could get commodity infla-tion and slow growth at the same time. But what is the relationship to low-but-rising bond yields? We might better look to demand (and supply) of bonds themselves. Just saying.

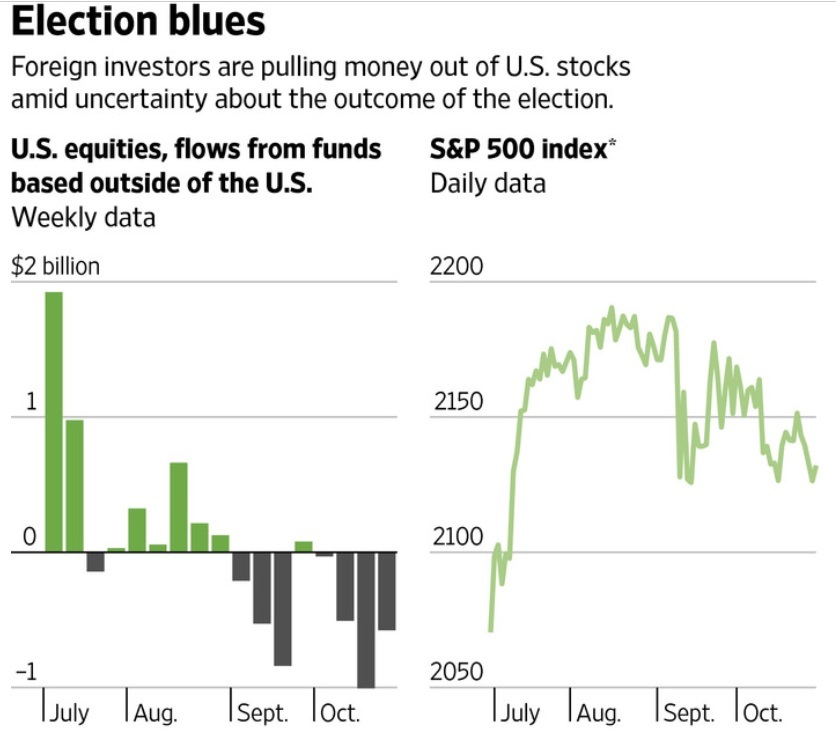

Political Tidbits: The WSJ reports foreign equity managers are pulling money out of the US in case Trump wins the election, a net $577 million in the week ending Wednesday. They have retreated in 7 of past 8 weeks. The managers think Clinton will win, but then, they thought Brexit would get voted down, too. The managers agree the S&P will rally if Clinton wins, overvalued or not. See the chart.

New reports from the Washington Post show Trump has not given any money to charity since 2009, belying his boasts about being a generous donor. No wonder he won't release his tax returns. Newsweek reports Trump has cheated subcontractors and vendors for over 30 years as a standard busi-ness practice. Newsweek and the NYT report Trump destroyed emails and other documents being sought under court order and not just once but numerous times. The NYT says "... Trump avoided re-porting hundreds of millions of dollars in taxable income by using a tax avoidance maneuver so legally dubious his own lawyers advised him that the IRS would most likely declare it improper if he were au-dited." This one trick was later outlawed by Congress.

It's not Hillary who is crooked. It's Donald. Hillary just picks bad managers.

The WSJ also reports a sad story: China's top climate negotiator Xie called on Trump to honor the car-bon deal that goes into effect this Friday. It calls for the US to cut net greenhouse gas emissions by 26%-28% below 2005 levels by 2025. China's equivalent promise has until 2030. Trump says he will cancel the deal. Xie said "I'm convinced, if it's a wise leader—especially a political leader—he ought to know that all his policies should conform to the trends of global development."

| Currency | Spot | Position | Strength | Date | Rate | Gain/Loss |

| USD/JPY | 104.99 | LONG USD | WEAK | 10/06/16 | 103.50 | 1.44% |

| GBP/USD | 1.2247 | SHORT GBP | WEAK | 09/10/16 | 1.3041 | 6.09% |

| EUR/USD | 1.0996 | SHORT EUR | WEAK | 09/19/16 | 1.1168 | 1.54% |

| EUR/JPY | 115.44 | SHORT EURO | WEAK | 10/21/16 | 113.15 | -2.02% |

| EUR/GBP | 0.8978 | LONG EURO | WEAK | 09/19/16 | 0.8564 | 4.83% |

| USD/CHF | 0.9857 | LONG USD | WEAK | 09/19/16 | 0.9804 | 0.54% |

| USD/CAD | 1.3399 | LONG USD | STRONG | 09/15/16 | 1.3203 | 1.48% |

| NZD/USD | 0.7174 | SHORT NZD | WEAK | 09/19/16 | 0.7305 | 1.79% |

| AUD/USD | 0.7670 | SHORT AUD | WEAK | 09/24/16 | 0.7618 | -0.68% |

| AUD/JPY | 80.52 | LONG AUD | STRONG | 10/06/16 | 78.48 | 2.60% |

| USD/MXN | 18.8716 | LONG USD | WEAK | 10/31/16 | 18.9054 | -0.18% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat