USD/CAD Forecast: Lighthizer, not light, at the end of the dark CAD tunnel

- The stability of the Canadian Dollar was broken by a double-data-disappointment.

- A light Canadian calendar leaves the focus on the FED and NAFTA

- The technical picture is balanced, and the pair still seeks a new direction

Double-disappointment, US yields, and NAFTA

We will begin from the end: Canadian data disappointed once again, preventing a positive close to the week for the loonie. Canadian CPI came out at 0.3% MoM in April, below 0.4% expected. Core CPI missed with 0.1% MoM against 0.2% predicted. Similar misses were seen in YoY numbers. The forecasts for a pick up in Q2 are not realized, at least not now. Retail Sales for March were more nuanced, but leaning lower as well. While headline sales rose by 0.6%, above forecasts, core sales dropped by 0.2%, far worse than a rise of 0.5% expected.

The disappointing sent the USD/CAD shooting higher, but it came on top of an adverse twist in NAFTA negotiations. Top US negotiator Robert Lighthizer said that there is still a lot of work and that the sides are "nowhere close" to an agreement. The headlines contrasted optimism voiced by Canadian Prime Minister Justin Trudeau and Finance Minister Bill Morneau. The C$ is sensitive to all comments.

In the US, bond yields remained in the driver's seat. The 10-year benchmark rose to 3.13%, yet another peak, the highest since 2011. Other maturities followed suit. Markets seized on small upward revisions to US Retail Sales figures to extend the gains. Other data points were mostly OK, but the roots for higher yields are deeper. They stem from the Fed's hiking intentions, the growing funding needs of the US government and also some fear about emerging markets.

Oil prices remained high amid shrinking inventories and production problems in Venezuela and other oil-exporting countries. Crude was a small positive for CAD.

Canadian events: Light calendar but one Lighthizer

The sole event on the Canadian economic calendar is the release of Wholesale Sales on Tuesday. A bounce is expected in March after a drop in February.

Much more importantly, NAFTA headlines are set to have a growing impact on the Canadian Dollar, as we have seen their influence recently. While the parties have vowed to continue working as long as necessary, the Mexican Presidential Elections still loom and put pressure to conclude the talks sooner than later. Positive comments from the US will likely have more impact than those from Canada. The US is seen as the tougher side in the negotiations. Likewise, negative comments from Canada could have a bigger adverse impact on the loonie in comparison to those coming from the US.

A deal is now slightly less priced in than earlier. So, an announcement about a done deal could undoubtedly give the loonie a boost.

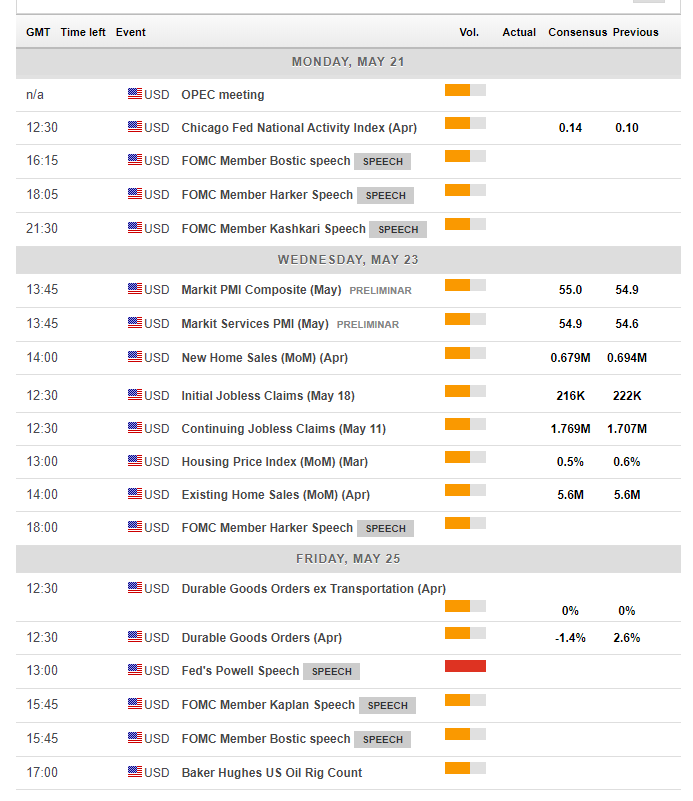

Here is the Canadian calendar for this week.

US events: Fed minutes, speeches and also some data

The Federal Reserve dominates the upcoming week. Fed members will be speaking throughout the week, culminating with a public appearance by Fed Chair Jerome Powell on Friday. Bostic and Kashkari are doves, Harker is a hawk, and Dudley and Kaplan are somewhere in the middle. Upbeat comments from doves may boost the US Dollar while cautious remarks from hawks could send it lower.

The Fed will also have its say with the release of the FOMC Meeting Minutes on Wednesday. The document may unveil more about the "symmetric" inflation target. Will the Fed tolerate higher inflation after an extended period of weakness? More importantly, the publication will likely confirm a rate hike in June, which is priced in by the markets. A sign of hesitance could weigh on the greenback.

Existing and new home sales are expected to remain at elevated levels while Durable Goods Orders on Friday stand out on Friday. They will provide insights into Q2 GDP growth and may shape expectations for the next Fed moves.

As in previous weeks, the 10-year Treasury yield will likely yield the most significant movements for the US Dollar. As we have seen, the greenback and the yields are not in full tandem, but the correlation is clear.

Here are the critical American events from the forex calendar:

USD/CAD Technical Analysis - Bulls are giving it a try

The late move on Friday tipped the trend in favor of the bulls, with an uptick in the RSI and a minor step up in Momentum. The has breached a short-term downtrend resistance line, a thin black line on the chart. The pair also topped the 50-day Simple Moving Average, but the pair is not going anywhere fast.

The broader picture remains mixed, with the thick black lines showing a narrowing wedge. Current trading levels are not far from those seen in previous weeks. The pair has yet to pick a direction.

1.2930 capped the pair on May 15th and is a line of resistance. It is followed by the round 1.3000 level that the pair failed to breach on May 8th. Further above, we note levels last seen in March: 1.3050 and 1.3130, when the pair traded on the much higher ground.

On the downside, 1.2870 capped the pair in late April and switches to support. The round number of 1.28 served as support in early May. 1.2750 and 1.2730 were swing lows in May as well.

-636622486731098145.png)

Where next for USD/CAD?

The recent signs of weakness in the Canadian economy, rising US yields and the fact that the pair's rally is not extended all support further gains. On the other hand, the high oil prices and more importantly a decisive turn in NAFTA negotiations could turn the tables. Assuming no NAFTA surprise, the pair could move higher.

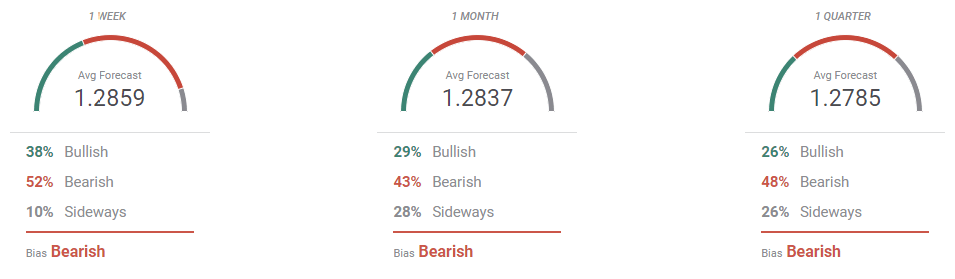

The FXStreet Forecast Poll shows a bearish bias in the short, medium, and long terms. Are they optimistic about NAFTA?

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.