US Second Quarter Final GDP Revision Preview: The consumer is cued

- Annualized GDP is the second quarter predicted to be unchanged at 2.0%

- Consumer spending driving US growth

- Business investment curtailed by trade concerns

The Bureau of Economic Analysis, a division of the Commerce Department will issue its final revision of annualized second quarter gross domestic product (GDP) on Wednesday, September 26th 12:30 GMT, at 8:30 EDT.

Forecast

Annualized economic growth in the second quarter is expected to be unchanged at 2.0%. The initial release was at 2.1%. First quarter growth was 3.1%.

US GDP

The US economy has slowed from its 3.1% annualized pace of growth in the first quarter. The decline to 2.0% in the second quarter and the likely continuation of that in the third is largely due to the pull back in business investment. The Atlanta Fed GDPNow model is currently tracking at 1.9%.

The almost two-year old trade confrontation with China that once seemed headed for agreement has inhibited business planning and spending and raised the threat of recession if the tariff competition escalates. Given the uncertainty this brings to planning business executives have decided to wait for an outcome before committing resources.

Business sentiment and investment

Business sentiment has been fading for a year. The 14 year high in the manufacturing purchasing managers’ index of 60.8 in August 2018 had tumbled to 54.3 by that December dragged down by the partial government shutdown at the end of the year. The rebound to 56.6 in January was solitary and by August the index has slipped to 49.1. It was the first reading below the 50 demarcation between expansion and contraction since August 2016.

Reuters

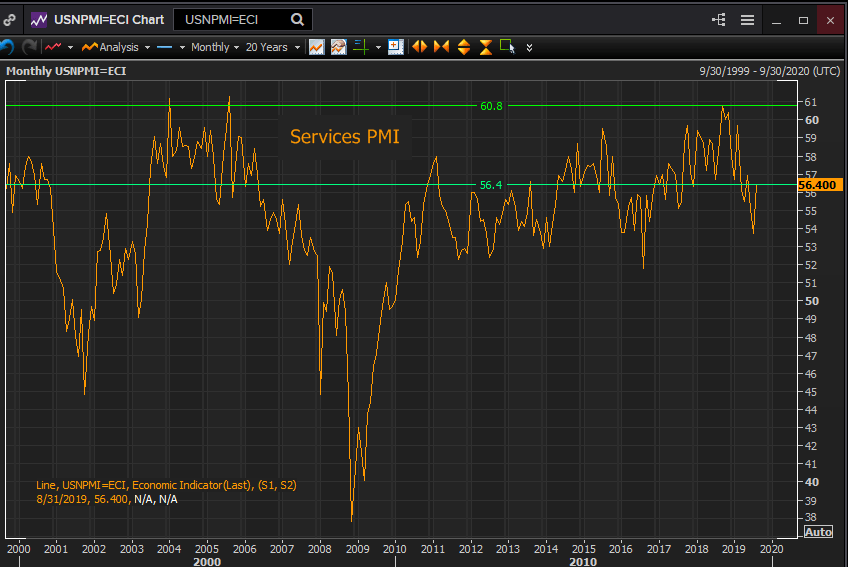

Optimism in the far larger service sector has fallen also though not as far and not into contraction.

The 13 year top of 60.8 in September 2018 had dropped to 56.7 by January. It recovered to 59.7 in February, was down to 53.7 in July but then came back to 56.4 in August.

Reuters

The September numbers for manufacturing and services will be released on October 1st and 3rd respectively.

The durable goods category of non-defense capital goods ex-aircraft is commonly used as an approximation for business investment. Shipments of these goods are included in the Bureau of Economic Analysis’ GDP calculation as business equipment outlays.

In July shipments dropped by 0.7% the most since October 2016. June’s shipments were revised to flat from 0.3%. Over the year these deliveries are 1.5% higher.

Business investment contracted in the second quarter for the first time since January, February and March of 2016.

Consumer spending

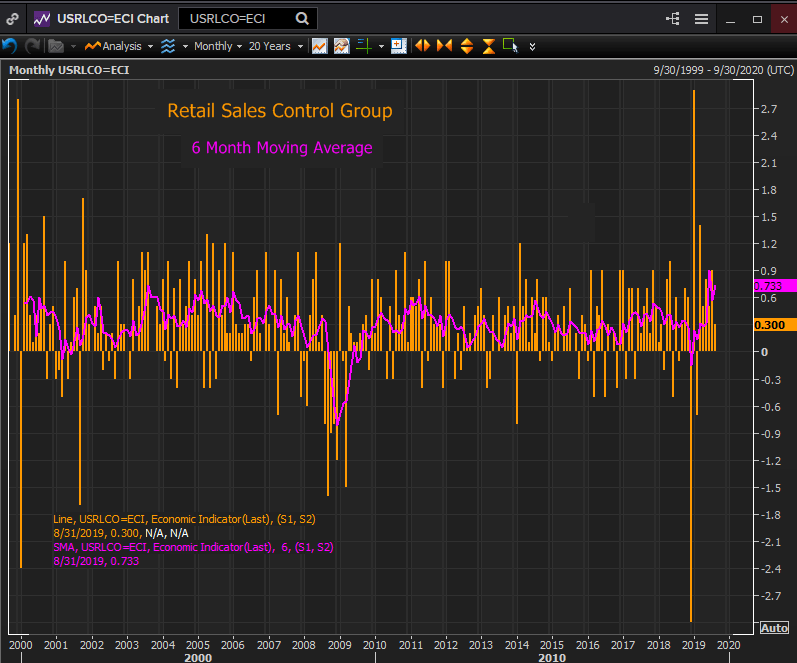

Consumption or consumer spending the economic activity that underpins approximately 70% of US GDP has been supported by the robust labor market. Excellent job creation, rising wages and historic levels of employment have given many Americans the best gains in disposable income in a decade

These wages have translated into a strong six months in retail sales. From March through August the control group classification, which is included in the BEA’s estimate of GDP, rose an average 0.733% per month. Leaving out June’s 0.9% average which was skewed by the reporting problems around the government shutdown in January, that is the best six month run in 16 years.

Reuters

Conclusion

As long as the consumer continues to spend the benefits of a buoyant labor market the US economy will muddle through. The current rate of consumption is equal to between 2.0% and 2.5% in GDP. Stronger growth will have to wait until business sees an improvement in the US China trade picture and global economic growth.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.