US PCE Price Index Preview: It’s not deflation you know

- Inflation in May to remain tame

- Core rate predicted to be unchanged

- PCE trending lower for five months

The Bureau of Economic Analysis (BEA) a division of the Commerce Department will release the May calculation of the Personal Consumption Expenditure (PCE) price index on Friday June 28th at 8:30 am EDT, 12:30 GMT.

Forecast

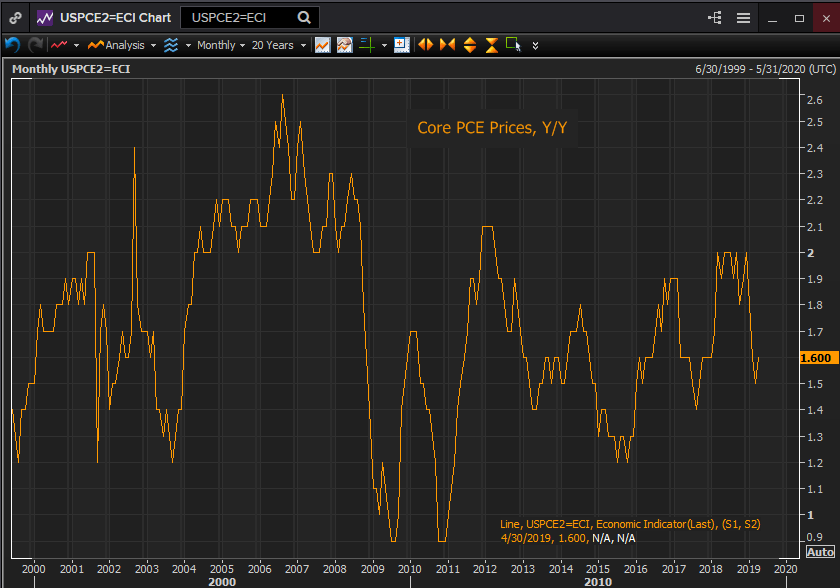

The overall PCE price increase is expected to fall to 0.1% in May from 0.3% in April. Annual inflation is predicted to be stable at 1.5%. The core PCE monthly rate is forecast to be unchanged at 0.2% as is the yearly rate at 1.6%.

The Fed and inflation targeting

The FOMC’s official shift to an easing bias at the June 19th meeting came after the decline of its preferred inflation gauge the core PCE price index from 2% last December to 1.5% in March and 1.6% in April.

The six non-consecutive months in 2018 from March through December when the index had registered 2% were the first time prices had been at the Fed target in six years. In late 2011 and early 2012 inflation also reached its goal with 2.1% from December through March and 2% in April.

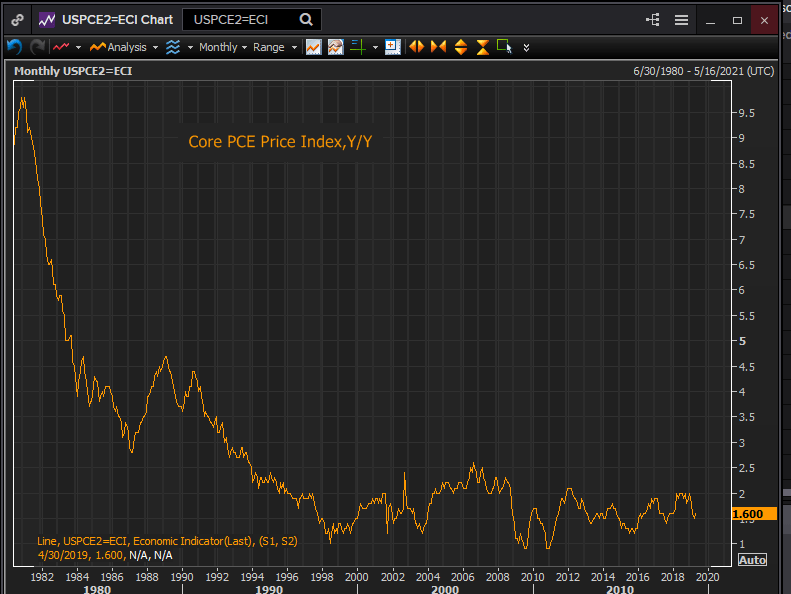

Those scattered 11 months over the decade since the financial crash and recession, 120 odd months, are the only inflation achievement of the Fed’s prolonged experiment with quantitative easing and the quadrupling of its balance sheet.

Reuters

The Fed and former Chairman Bernanke would point to the threat of deflation in the immediate aftermath of the financial crisis as reason enough for the exceptional policies.

Over the years the Fed has seemed curiously blasé about the almost perennially underperformance of inflation.

Chairman Powell’s response to a question about low inflation after the May 1st FOMC meeting could stand for any number of Fed comments about inflation over the past ten years. “The weak inflation performance in the 1st quarter was not expected...some of it appears to be transitory or idiosyncratic.”

As could the phrase from the June 19th FOMC statement “… [The Fed] will act as appropriate to sustain the expansion, with a strong labor market and inflation near its symmetric 2 percent objective.”

PCE, growth and Fed policy

The Fed’s current policy bias has not been driven by a response to declining inflation. The logic and concern exhibited by governors and the Chairman over the past six months is due to a modest deterioration in the US macro-environment and to large concerns about where the world economy might be headed if the US-China trade dispute and Brexit are not settled on amicable terms.

The recent slowdown in the global economy could become substantially worse, with businesses and consumers holding back on spending and further retarding weak growth in Europe and China which would in turn impact the entire world including the United States.

Interest rates in the United States began to fall in November, two months before the Fed’s last rate hike to 2.5%. Global rates have accompanied US rates lower. The judgment of the credit markets has been consistent that the expansion would not tolerate higher interest costs or maybe, and more cynically, that the Fed would quail at the first sign of trouble.

With almost all of the central banks of the industrialized nations cutting rates or thinking publically about doing so, the Fed’s inflation target is an additional excuse to do what the governors want to do.

If PCE is weaker than predicted, the Fed will quote it as partial justification. If it stronger than expected, even at 2%, perhaps someone will note that this too is transitory.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.