US Non-Farm Payrolls November Preview: Labor market continues to defy concerns

- Payrolls expected to rise 180,000 as GM strikers return.

- ADP jobs of 67,000 were less than half the 140,000 forecast.

- Employment PMI in manufacturing and services declines in November.

The Bureau of Labor Statistics (BLS) a division of the US Department of Labor will release its Employment Situation Report for November on Friday, December 5th 13:30 GMT, 8:30 EDT

Forecast

Non-farm payrolls are predicted to rise 180,000 in November following October’s 128,000 increase. The unemployment rate is expected to be unchanged at 3.6%. Hourly earnings will gain 0.3% in November after October’s 0.2% increase and annual earnings will be stable at 3.0%. The labor force participation rate will stay at 63.3%. Average weekly hours will remain at 34.4.

The Employment Situation Report

The Labor Department’s Employment Situation Report, normally referred to as non-farm payrolls or NFP for short, is the most complete write-up of the US labor market produced by the federal government. Its jobs and unemployment figures are the most widely followed and traded US statistics.

The report’s data is solicited by two surveys. The establishment survey contacts a sampling of non-farm businesses and queries various employment related details of the firms. This questionnaire produces the payroll numbers, wages, weekly hours, labor force participation rate and other statistics.

The separate household survey polls a statistical representation of US households and asks if the non-military working age members are employed and if not when they last sought a job. This information produces the several BLS unemployment rates.

The unemployment rate commonly quoted by the media and analysts is the U-3 rate. This measure is limited to unemployed individuals who had looked for work in the month prior to the survey. Any individual who is not working but had not searched for a job in the previous month is not counted as being in the labor force and thus not unemployed.

A second jobless rate, the U-6 or underemployment rate has a broader definition. Here the BLS considers unemployed anyone who is not working and had looked for a job in the prior year. It is considered by many analysts to be a more accurate measure of joblessness and is normally several points higher than the U-3 rate.

The non-farm payrolls number also includes an estimate for the number of jobs created each month by new businesses.. Because most of these new concerns have not interacted with Federal government agencies the BLS uses a statistical program, the so-called birth–death model, to predict the number of new hires each month based on historical labor market performance.

By the end of the year when payrolls have been reported to the IRS the estimated figures are revised against actual tax rolls in the annual baseline revision. Adjustments have been 500,000 a year or more.

Payroll data is one of the most timely economic statistics as its data is one month old.

Payrolls and economic growth

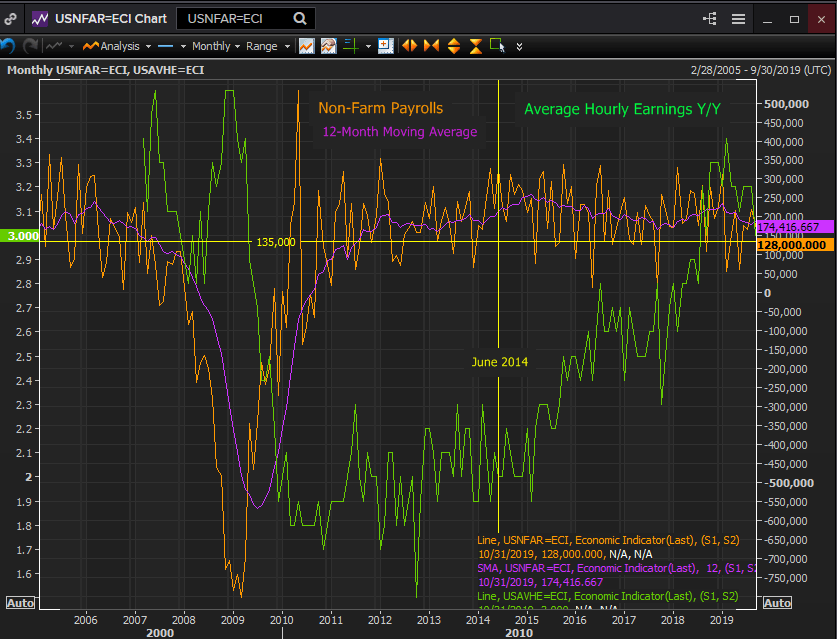

Job creation has tracked US GDP lower through three quarters. Economic growth has subsided from 3.1% annualized in the first three months of the year to 2.0% in the second quarter and 2.1% in the third. Non-farm payrolls have dropped from a 12-month moving average of 245,000 in January to 171,000 in October. The three-month average has fallen from 236,000 to 159,000.

Annual wage gains however have remained strong, posting 3% or above for 15 months in the best performance since the recession ended a decade ago.

Wages and the recession

According to the Bureau of Labor Statistics (BLS) the US economy lost 8.7 million jobs in the financial crisis and aftermath. It took the US economy until June 2014 five years after the end of recession to recover those positions.

The US economy needs to create about 135,000 new jobs each month to keep pace with population and labor force expansion. From February 2008 when payrolls shrank by 82,000 jobs until March 2010 when job growth resumed in earnest the employment shortfall was 135,000 greater each month than the recorded payroll losses. Just those 25 months alone added another 3.4 million missing jobs and places on the unemployment rolls.

This shortage of employment extending for years beyond the end of the recession as the economy struggled to create over 12 million jobs and the huge surplus of unemployed workers was the main reason wage increases stayed below their historical average for a decade after the recession despite the historically healthy job numbers for most of the post-crisis period.

It was only in August of 2018 nine years after the downturn ended and four years after the BLS said that the job losses of the financial crisis had been made good the that annual wage gains broke above 3%.

Reuters

It was the 10.6 million jobs created from July 2014 to August 2018 that ended the unemployment backlog from the recession and enabled the next year’s job market to finally pressure wages above 3%.

American households are seeing the best income gains and labor market flexibility in a decade. When combined with low inflation, real income and disposable income have increased notably. Those gains have maintained consumer spending and economic growth.

ADP and NFP

Job creation in both series has fallen substantially this year though from a high base..

The trend correlation between the two payroll series is high. Since January ADP’s 12-month moving average has dropped 24%, NFP 30%.

The three-month average for ADP has fallen from 253,000 in February to 125,000 in October. The 12-month average has dropped from 220,000 to 168,000. Non-farm payrolls are down from 245,000 for the 12-month average in January to 171,000 in October, and the three-month is off from 236,000 to 159,000 in October.

Over the past year ADP has dipped below 100,000 three times, November, September and May. Only once, in May did NFP have a correspondingly weak month at 72,000.

Purchasing managers’ indexes

Overall measures from the Institute for Supply Management have declined this year with the manufacturing PMI now in contraction for four months to November. Though the fading business optimism has not as yet affected hiring the weaker than forecast November results particularly in the dominant service sector have elicited concern. At some point, a point that seems to be approaching, the increasing pessimism in the business sector must impact hiring.

Employment, business and consumer spending

Consumption has been the engine that has kept the US economy humming. Retail sales in the control group classification that informs the GDP calculation have averaged a 0.433% monthly gain over the past half year.

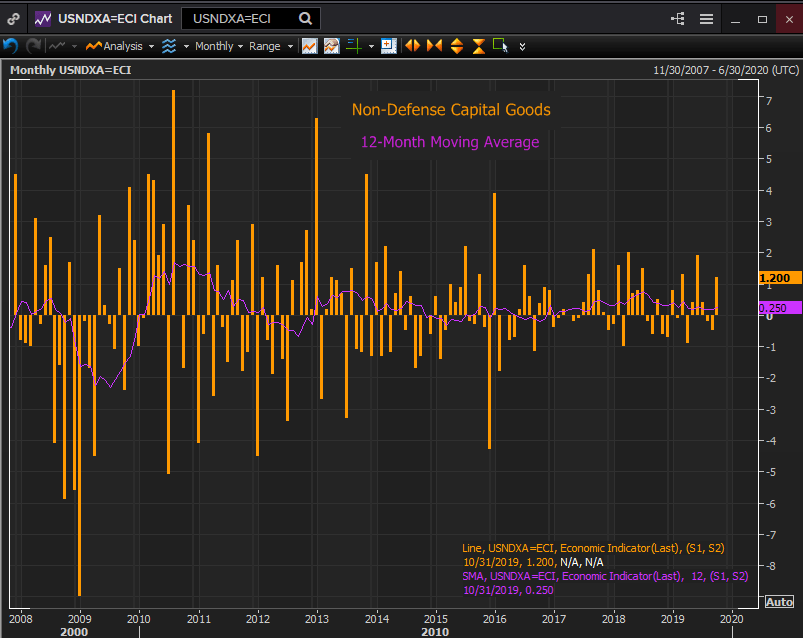

Though business investment in the durable goods non-defense capital goods category was negative in August and September, October’s unexpected 1.2% jump may indicate that the year- long decline in business spending is ending.

Reuters

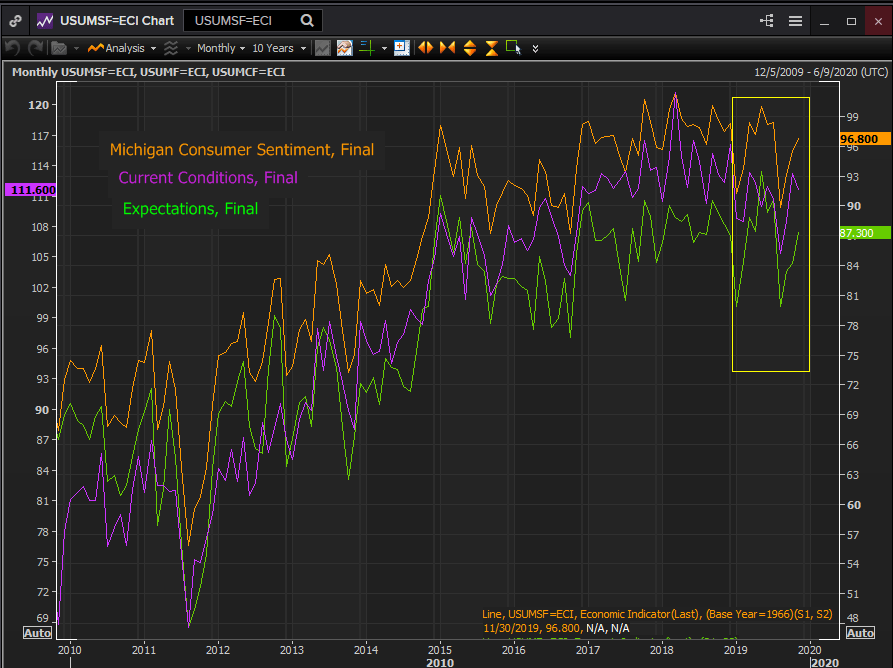

Consumer sentiment has stayed buoyant reflective of the strong labor market and rising wages.

Reuters

Coincident labor statistics

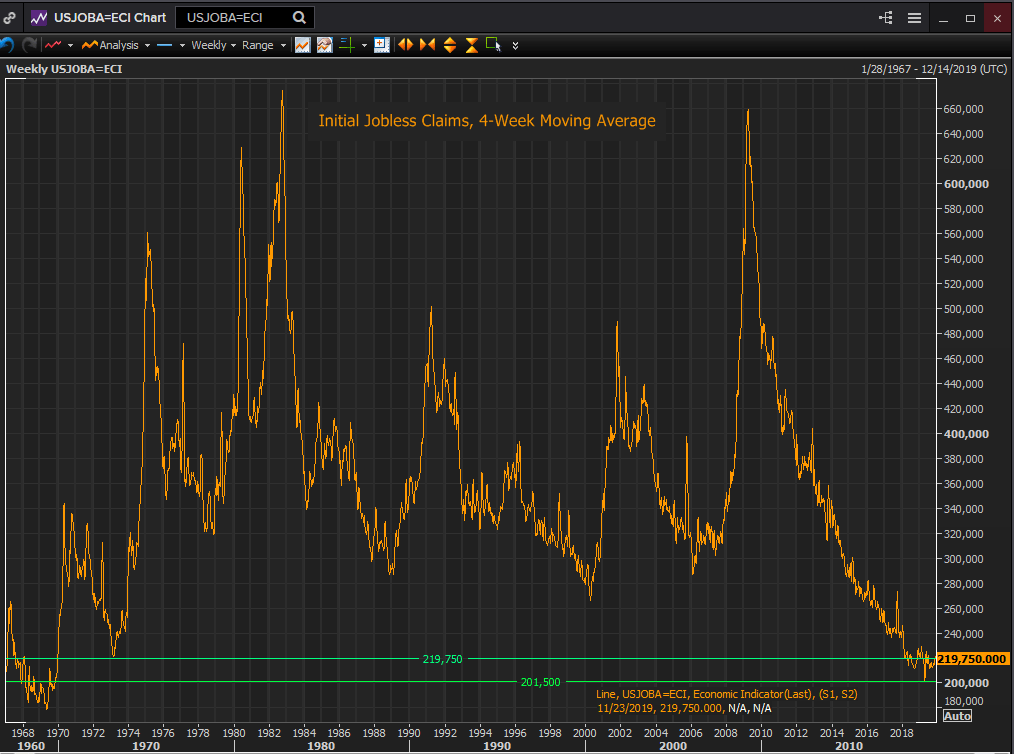

Neither the unemployment rate at 3.6% nor the initial jobless claims 4-week moving average at 219,750, both near five decade lows, harbor any hints of labor market trouble.

Reuters

Conclusion and the dollar

Payrolls have remained resilient despite the decline in US economic growth. When measured by historical standards and by the number of new jobs needed each month to maintain full employment the labor market is operating at capacity.

The year-long decline in manufacturing sentiment and employment, largely a product of the China trade war, has not spilled over into the service sector which has continued to produce a steady stream of new jobs. Consumers remain confident and spending expansive.

The weak ADP November result is unlikely to be matched by NFP. Month to month correlation is low and the 40,000 to 60,000 GM and allied industries workers who struck and were subtracted from October payrolls will return in November.

The dollar has be on the defensive recently dragged lower by poor US data, primarily the two ISM indexes. If the NFP misses the 180,000 forecast by more than a modest amount it will add to dollar weakness even if it is not a dire sign for the US economy. A better than projected result will blunt the dollar’s decline but it will not restore advantage until it is seconded by other improved data

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.