US July Services PMI Preview: The US is not enough

- Service sector sentiment predicted to rise in July

- Index has been stable since March

- Service sentiment weakening but less affected by US china trade war

The Institute for Supply Management will release its non-manufacturing Purchasing Managers’ Index for June on Monday August 5th at 10:00 EDT, 14:00 GMT.

Forecast

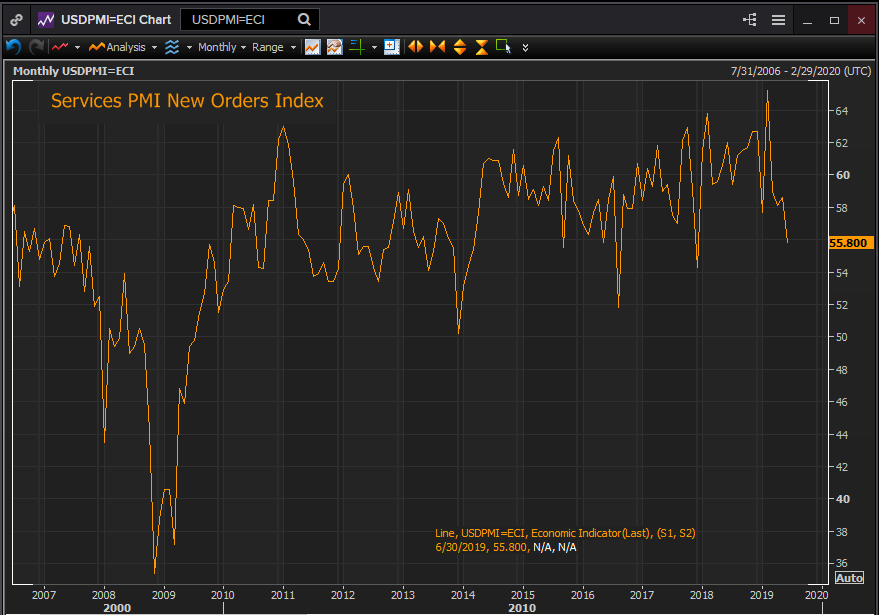

The headline Purchasing Manager’s Index is expected to increase to 55.5 in July from 55.1 in Jun. The business activity index will edge up to 58.3 from 58.2. The new orders index was 55.8 in June and 58.6 in May. The employment index was 55.0 in June and 58.1 in May.

Services Business sentiment and the US economy

The US trade dispute with China has been, since its inception more of a concern to business executives that to the general public. Businesses have to worry about supply chains and distribution networks, many of which pass through China, about the portion of their sales that come from a slowing global economy and where this all leads in six months or a year.

Sentiment in the services sector reached 61.6 in September, the highest post-recession score, fell to 56.7 in February this year in the aftermath of the partial government shutdown and has been slipping since.

FXStreet

The new orders index was 55.8 in June its lowest level since December 2017.

FXStreet

The US background in contrast has been strong. The economy expanded at a 3.1% pace in the first quarter and 2.1% in the second. The labor market remains exceptionally healthy. In any other era a 3.7% unemployment rate, 165,000 new jobs each month and 3.2% average wage growth with a 1.5% overall inflation rate would be celebrated.

Federal Reserve

The central bank’s angst over international economic growth and the impact of the China dispute that led to the first fed funds rate cut in over a decade match those of business. The opportunity cost of having the world’s two largest economies mired in a tariff laden trade war is high. The global economy is deprived of the full services of its two most dynamic growth engines. With the European Union in apparent denial about the economic cost of the British exit, the three largest economic entities are not only underperforming in the present but face a darkening future.

Consumer and business sentiment and GDP

American consumer attitudes have held up despite the gloomy international picture. The Michigan Consumer Sentiment Survey registered 98.4 in July, in the middle of its robust post-2016 election range.

Propelled by the best labor economy in a generation, with jobs plentiful and remuneration rising at the best pace in ten years, households are a strong base for the US economy.

Consumption is by far the largest segment of GDP at 70%. At its current rate of activity consumer spending is capable of fueling about a 2.0% rate of growth in the US. To go beyond that level business investment and overseas trade are required and those are the areas most inhibited by the international situation.

Executives are not being unduly pessimistic when their depressed attitudes are so at odds with the home front economy. By necessity they must look farther than the United States for direction.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.